Kevin Warsh takes over as Chairman of the US Federal Reserve. He replaces Jerome Powell , who can look back on an eventful tenure at the helm of the Federal Reserve (Fed).

This time, the handover is more delicate than usual. This is because US President Donald Trump, who nominated Warsh, has been exerting strong pressure for lower key interest rates for some time. The US Senate’s vote in favor of Warsh was also close, with 54 votes to 45 confirming him as the future head of the world’s most important central bank. What events shaped Powell’s eight-year term of office and in which direction could US monetary policy develop under Warsh’s leadership?

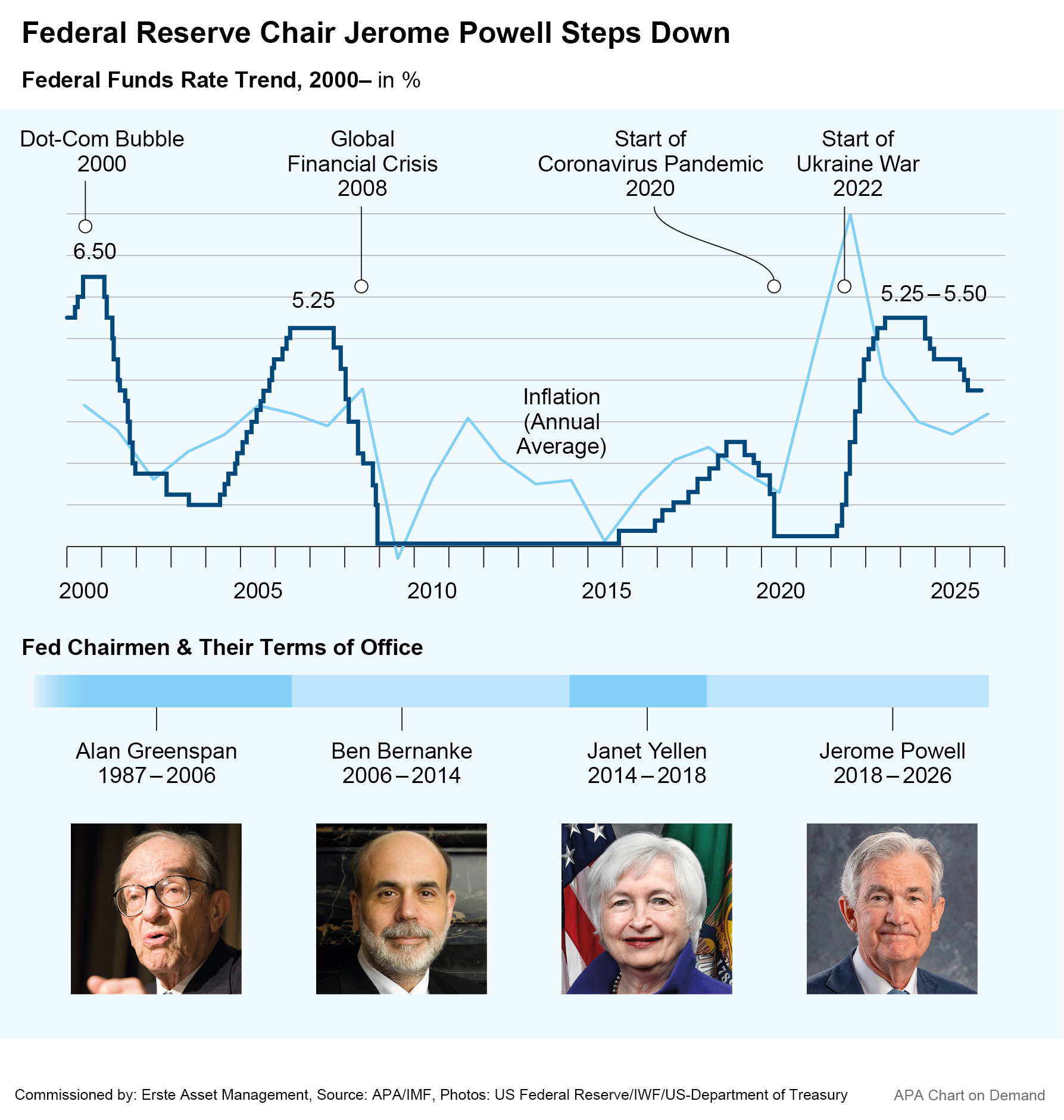

Powell’s turbulent time at the helm of the Fed

Powell led the central bank back to normality after the zero interest rate phase of the financial crisis, supported the economy with drastic interest rate cuts at the start of the pandemic and responded to the high inflation resulting from the lockdowns and the war in Ukraine with a cycle of interest rate hikes.

However, the central banker is likely to be remembered above all as a fierce opponent of US President Donald Trump. Trump has repeatedly criticized the Fed’s monetary policy under Powell. He has spoken out in favor of a key interest rate of one percent or less. During both of Trump’s terms in office, Powell defied the president’s attempts at intervention and insisted on the central bank’s independence.

Trump himself had appointed Powell to head the Fed. He succeeded Janet Yellen, who was also criticized by Turmp. In 2018, Powell initially continued his predecessor’s course of moderate interest rate hikes and was harshly criticized by Trump even then: “I think the Fed has gone crazy,” said Trump at an election campaign event.

After the pandemic years and the massive rise in inflation, a fall in inflation made it possible to cut interest rates again in 2024. However, Powell took a cautious approach and did not cut interest rates as quickly as Donald Trump, who has since been re-elected president after Joe Biden’s interregnum, would have liked. Trump publicly criticized Powell several times in harsh terms and expressed his desire for faster interest rate cuts.

In return, Powell insisted on the independence of the central bank. In 2025, Trump’s criticism of Powell escalated and grew into threats of dismissal. Trump’s attempts to intervene in connection with the upcoming change at the head of the US Federal Reserve fueled speculation that the Fed could no longer only pursue the goals of low inflation and full employment in future. What government wouldn’t want low interest rates on government debt and low lending rates for private households and companies?

US Federal Reserve already on the “dovish” side

As mentioned, the main task of monetary policy is to pursue two objectives: Full employment and price stability – i.e. low inflation. This already reveals an important area of friction. This involves the old question of whether a central bank should act in a more inflation-fighting (hawkish) manner and thus in favor of creditors or bond investors, or in a more business-friendly manner and thus in favor of debtors or equity investors (dovish).

A look at the key indicators of inflation, the unemployment rate and economic growth suggests that the Fed is now acting rather dovishly. At 3.8%, inflation is well above the target value, while inflation-adjusted growth of 3.3% is clearly above the potential value. The Fed’s forward guidance, i.e. the outlook for interest rate policy communicated by the central bank, also fits into this picture.

Status as at May 2026

Two forces are currently shaping the economy and the financial markets. On the one hand, the Iran conflict is pushing up energy prices. Part of this will be passed on to other inflation components. On the other hand, the AI boom is primarily an investment boom that is boosting inflation. Only in the medium to long term could the use of AI increase productivity and thus reduce inflation (higher labor productivity, more efficient processes, lower production costs, higher potential growth rate).

Numerous central banks, including the European Central Bank, have reacted to the inflationary developments by signaling interest rate cuts. In contrast, the Fed is still officially inclined to cut interest rates. However, this stance is shared by fewer and fewer Fed members, which is why the market is already pricing in a tenth of a percentage point higher key interest rate by the end of the year.

What will change under Kevin Warsh?

In this context, it is interesting that the new Fed Chairman Kevin Warsh is in favor of changing the Fed’s communication strategy. The Fed could withdraw its forward guidance, i.e. its outlook on interest rate policy. This would increase the central bank’s flexibility, but at the same time increase market volatility. Interest rate expectations would then depend more on new data (inflation, employment) and less on a previously communicated path.

Warsh recently argued in favor of lower interest rates, pointing to AI-induced productivity gains, among other things. This may have opened up a contradiction: should greater emphasis be placed on data dependency in the future or should forecasts be taken into account?

In fact, there is even more at stake. The US national debt is high and, according to OECD data, recently stood at 125% of GDP – as were the interest payments on the national debt, which amounted to 4.1% of GDP. It is not only in the USA that there is a risk that the central bank will no longer be able to focus its monetary policy primarily on price stability, as higher interest rates could jeopardize the sustainability of public finances. In technical terms, this is known as fiscal dominance over monetary policy. Normally, a central bank should raise interest rates or keep them high if inflation is too high. This becomes more difficult in the case of fiscal dominance because higher interest rates increase the interest burden on the state, increase the budget deficit and can therefore raise doubts about debt sustainability.

So what will change under Kevin Warsh? De jure, the Fed Chairman is not the sole decision-maker on monetary policy: he only has one vote on the Federal Open Market Committee (FOMC) and requires majorities for interest rate and balance sheet decisions. De facto, however, his role is considerably greater. He sets the agenda, organizes the FOMC consensus, shapes communication, influences the perceived reaction function and can change the Fed’s institutional direction. In Warsh’s case, the relevance therefore lies less in the question of whether he alone can push through interest rate cuts, but whether he will shift the Fed regime via communication, balance sheet policy, regulatory priorities and the relationship with the Treasury.

Conclusion

To summarize: The Fed’s previous policy can already be described as rather dovish. This will not change under the new Fed Chairman, because Kevin Warsh is already arguing for interest rate cuts . However, he cannot cut interest rates on his own. All in all, ceteris paribus, this still speaks more in favor of equities than bonds (assuming that inflation remains above the central bank target of 2%).

At the same time, Fed policy could become less predictable if forward guidance is weakened. This would probably result in higher market fluctuations if economic data develops unexpectedly. The higher uncertainty implies, at least in theory, a higher risk premium, i.e. a higher difference between long-term and short-term bond yields.

One of Kevin Warsh’s possible projects as Fed Chairman is to reduce the central bank’s balance sheet by selling government bonds. However, this would be a major project that would require a lot of preparation. Speculatively, one possible consequence could be that bond sales would tighten the financial environment to such an extent that key interest rates would have to be cut. However, just like the fears that monetary policy could become subordinate to fiscal policy, this is just speculation at the moment.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Discretionary Portfolio Management Update: Spring awakening

Despite geopolitical tensions and rising inflation, the capital markets are proving resilient. Good US corporate earnings are supporting this trend. In this Discretionary Portfolio Management update, Gerald Stadlbauer explains why a balanced, risk-conscious investment strategy remains important.

Trade conflict & Ukraine war: How structural change could affect the markets

In the global world order, much seems to be in a state of upheaval. The changes brought about by the new US administration are a structural change that is also affecting the financial markets. In our view, this scenario is currently the most likely 👉