The market participants are still focused on the implications of Donald Trump’s victory at the US presidential elections. In simple terms, “Trumponomics” are a combination of expansive fiscal policies and restrictive trade policy. An increased budget deficit is supposed to support economic growth, while the curbing of free trade aims at job protection.

Heterogeneous growth

While real global economic growth is below average, it is also remarkably constant at +2.5%. Trumponomics will make economic growth more heterogeneous and probably also more volatile (i.e. higher fluctuations). The trade-off is between an outlook of higher economic growth in the USA and possible, so-called positive externalities (NB higher US growth could be beneficial for the rest of the world) on the one hand, and a restrictive trade policy and higher US interest rates on the other hand.

Falling deflation pressure

The decline in commodity prices over the past years has caused inflation to fall sharply to excessively low levels. The global deflation pressure is subsiding on the back of the stabilisation of commodity prices that we have seen this year. In the USA, economic stimulus is provided against a backdrop of economic resources (i.e. labour, capital) already tending towards full capacity utilisation. The so-called negative output gap has probably already been closed. In the USA, the overheating of the economy and an increase in inflation have become more likely.

The end of austerity

The budget balance adjusted for the effects of the economic cycle, i.e. the so-called structural balance, was at -2.5% of GDP in 2015 in the developed economies. For 2016, the consensus expects an increase of the budget deficit to 2.8%. The general austerity pressure exerted by governments has already subsided even prior to the expected expansion of the budget deficit in the USA. The assessment according to which the central bank policies are “the only game in town” has lost its validity.

No additional impulse from monetary policy

The market does not expect additional expansive measures from any of the important central banks. Their policies are already in extreme territory. Key-lending rates are low, some of them even negative. Also, the central banks are buying large volumes of bonds in order to keep yields low and generate liquidity. Since deflation pressure is falling, so is the need for additional measures. In the USA, economic growth and inflation expectations are on the rise due to the outlook on tax cuts and ramped-up spending. Therefore, the expectations regarding rate hikes by the US Fed are also rising.

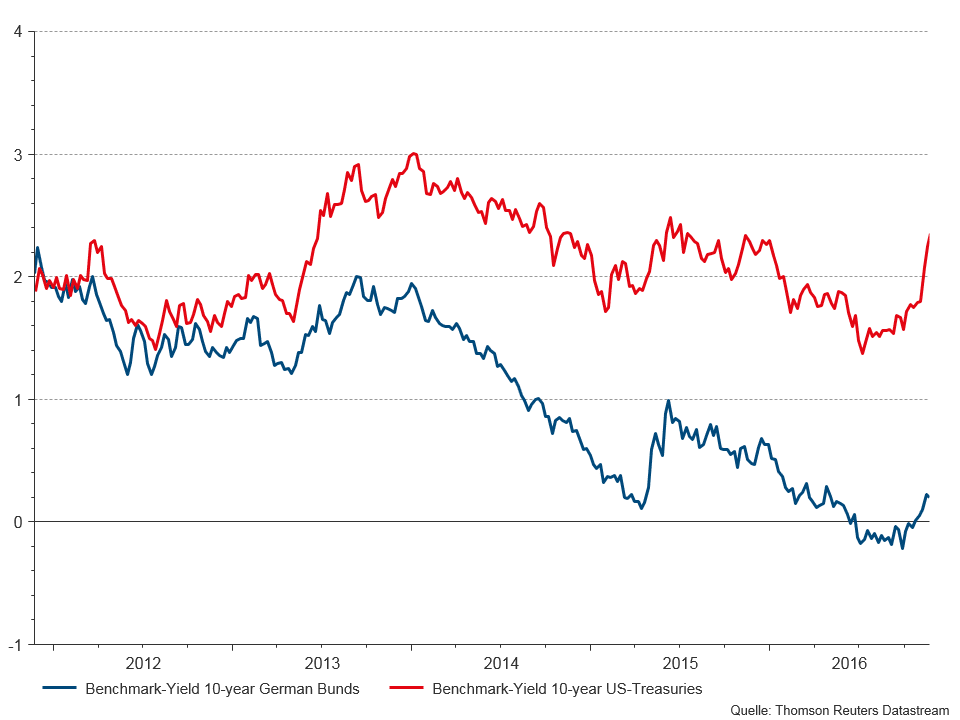

Yield comparison 10-year Government Bonds Germany vs. USA (11/2011-11/2016)

Source: Thomson Reuters; Data per 24.11.2016

Stalling globalisation

The process of globalisation has stalled, with global trade currently only growing at low rates anymore. Donald Trump has confirmed that he wants to withdraw from the Trans-Pacific Partnership Agreement (TPP). The risk associated with this situation is that of actionist measures being replaced by a trade war. This would cause world trade to contract. In contrast, the Chinese President Xi Jinping announced at the 21st Asia-Pacific Economic Cooperation Summit in Peru that China wanted to play a bigger role in globalisation (free trade, free flow of capital). This would strengthen the trend towards a multi-polar world.

Climate agreement

There is ultimately also the hope that some of Trump’s delicate statement during the campaign will not be implemented. After all, this week he said he was “open” about the previously announced withdrawal from the climate agreement.

Adjustment and consolidation

The market prices have adjusted to the outlook of higher economic growth and higher inflation in the USA (i.e. higher bond yields), a heterogeneous environment (i.e. appreciation of the US dollar against other currencies), possible positive spill-over effects to the rest of the world (i.e. higher yields in the Eurozone), and possible negative consequences (i.e. falling prices of equities, bonds, and currencies in the emerging markets).

Will this development continue? We might see a phase of consolidation, because there is still little specific information on the kind, extent, and speed of the possible measures to be taken by Trump’s cabinet, and it will take a few quarters before we can notice the effect in the real economy.

Postscript: This also goes for US equity indices, which have set new highs this week. The economy already suffers from the strong US dollar, whereas possible measures supportive to the economy would only become effective several quarters down the road.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Central banks are becoming more cautious: these are the implications for the bond market

The investment package in Germany and the associated ‘abandonment of the debt brake’ has caused a lot of movement in the eurozone bond market. Meanwhile, central banks have to manage the balancing act between slowing economic growth and rising inflation. Dániel Bebesy, Fixed Income Portfolio Manager at Erste Asset Management Hungary, talks in an interview about the recent central bank meetings and their impact on the bond market.