Who wouldn’t be happy about that? A new cosy jumper in the new autumn/winter trend colour 2023, “butter yellow”! The new trendy garment is quickly pulled from the shelf and after thoughtlessly inserting the ATM card at the checkout, you are the official owner of a new jumper.

Shortly after leaving the air-conditioned shop, you are shocked for a moment that it is still 27 degrees outside at the beginning of October and you can’t help but think of climate change. Immediately, you are plagued by thoughts like “Do I really need this jumper?”. As we all know, the most sustainable piece of clothing is the one that was never made…

The environmental impact of the textile industry

On the one hand, the textile industry depends on numerous natural resources; on the other hand, it is precisely these dependencies that result in various impacts on the environment. In addition to water (N.B. an average of 2,700 litres of water is used to produce one cotton T-shirt), land is also needed to grow cotton. The dyeing and finishing of textile products with chemicals alone are estimated to be responsible for about 20% of global wastewater.

In addition, the fashion industry produces about 10% of global CO2 emissions. At around 4-5 billion tonnes of CO2 emissions, this is about tantamount to what all international flights and global shipping combined generate. These figures push the textile sector to near the top of the list of major drivers of global water pollution and land consumption (N.B. in 2020, the textile sector was the third largest source of water pollution and land consumption). [1]

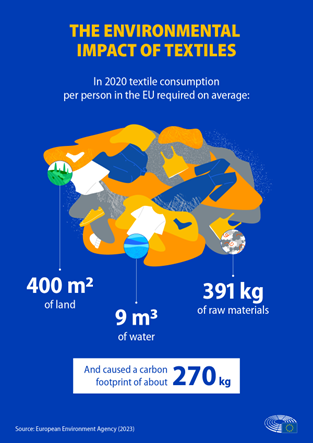

In 2020, an average of 400 m2 of land, 9 m3 of water, and 391 kg of raw materials were needed to meet the textile needs of one EU citizen. This corresponds to a carbon footprint of approximately 270 kg. [2]

Source: European Environment Agency

What is climate risk actually?

Even the booming fashion industry is confronted with a wide variety of challenges due to climate change that could make the entire industry rethink its ways. These “new”, extensive risks that are only becoming apparent as part of the climate crisis are called climate risks and include all uncertainties that can arise in connection with climate change.

Mark Carney, former Governor of the Bank of England and co-founder of the Task Force on Climate-Related Financial Disclosure (TCFD), said in a speech more than eight years ago: “Climate change is the tragedy of the horizon”. [3] The famous sentence, as well as the entire speech, was seen by many as a turning point in the global discussion on the challenges of climate change in the financial industry.

The TCFD was originally created to provide investors, lenders, and other financial market participants with better climate-related information. [4] The idea was that this would facilitate more informed decisions regarding climate-related risks (and also opportunities!). In its recommendation report, the TCFD divides climate change and carbon-transition risk factors into two categories: physical risks and transition risks. [5]

The frequency of heat waves and extreme weather events has increased compared to pre-industrial times. The costs associated with these actual, tangible, physical impacts of climate change are referred to as physical risks. Physical risks can be divided into acute and chronic risks. Extreme weather events (e.g. floods) are examples of acute physical risks. Longer-term changes in climate patterns that could lead to a warmer environment or rising sea levels, on the other hand, are chronic physical risks. [6]

The risks associated with the transition to a low-carbon economy are referred to as transition risks. These risks can be divided into four sub-categories:

- Reputational risk: e.g. the increasing stigmatisation of CO2-intensive economic sectors.

- Market risk: e.g. the change in customer behaviour, rising prices for raw materials

- Technology risk: e.g. the development of new technologies with lower CO2 emissions or the substitution of current technologies.

- Legal and political risk: e.g. increased pricing of GHG emissions, increased reporting of GHG emissions, increased vulnerability to litigation.

Climate risks in the textile industry

As pointed out above, all kinds of raw materials and natural resources are needed to produce new garments. Besides cotton, leather and wood are among the most important commodities in the textile world. From this, some risks can be derived that could be of great relevance to the industry in the future. Once certain risks for the textile industry have been evaluated, it is also necessary to assess how exposed one is to the identified risks and how these risks can best be managed.

Biodiversity, land use, und water use:

The cultivation of cotton goes hand in hand with enormous land use and dwindling biodiversity in the growing areas. On the one hand, heat waves, droughts (and at the opposite end, cold spells), and floods can have an impact on the cotton crop. With a constant change in climate, the current cultivation areas may no longer be able to meet the cultivation needs of the crop in the future. These are classically physical risks, as the textile sector is directly impacted by extreme weather phenomena and long-term climate change. On the other hand, regulatory risks related to land use and biodiversity also play a role. In addition, production sites in areas with less water could be increasingly confronted with reputational risks in the future.

The textile industry is therefore highly dependent on various natural resources, which is why the loss of biodiversity and sufficient water is one of the main risks. Some of the approaches used by companies in the textile industry to address water scarcity include water optimisation programmes (frequently in cooperation with local communities), water reduction programmes together with agricultural suppliers, and the measuring of water efficiency.

Carbon footprint of the product:

The textile, apparel, and luxury goods industries face regulatory risks regarding the carbon footprint and environmental labelling of products. Higher and more volatile energy prices upstream along the value chain (affecting raw materials, input, and distribution costs) could lead to higher costs. Companies are more vulnerable the higher the CO2 intensity is of the business unit whose operations are located in countries where regulations are becoming more stringent. To better manage the risks, the carbon footprint could be measured through a product life cycle analysis. Furthermore, the emissions of the suppliers (across the entire value chain) should be collected and reduction targets should be defined.

Raw material procurement:

Companies depend on raw materials such as cotton, leather and wood. The production of these raw materials can have serious environmental effects, such as deforestation, water and pesticide use, and the release of hazardous chemicals. Cotton fields are often monocultures, which is why the use of pesticides is on a continuous rise. However, as the use of certain pesticides is not entirely safe for both humans and the environment, new regulations in this area may be introduced in the future. Poor impact management could also lead to reputational and brand damage.

Risk management in the supply chain of fashion companies includes, for example, the procurement of raw materials (cotton, leather, …) that are environmentally certified by third parties. In addition, the handling of controversial raw materials should be evaluated and, if necessary, guidelines should be developed. It should also be noted that cooperation with suppliers in the procurement of raw materials is becoming increasingly important.

Conclusion

Exactly what additional challenges and risks climate change will bring remains uncertain. What is certain, however, is that the relationship between the environment and businesses in the fashion and textiles industry is characterised by significant interdependencies. Just as the industry has a serious impact on the environment and the climate, climate change also has significant implications for businesses in the industry, particularly when they are affected by natural disasters caused or exacerbated by climate change. Extreme weather conditions can also affect supply chains and operational processes.

To better evaluate the risk situation, the development of resilience plans and the implementation of environmentally friendly practices is part of reducing the impact on the environment. It is also important that companies reduce their dependence on fossil fuels and use renewable energy to reduce their emissions and minimise their carbon footprint.

Read more articles from the ESGenius Letter on the topic of “Climate Risks” here!

[1] The impact of textile production and waste on the environment (infographics) | News | European Parliament (europa.eu)

[2] 20230613PHT98335_original.png (1200×1700) (europa.eu)

[3] Breaking the tragedy of the horizon – climate change and financial stability – speech by Mark Carney | Bank of England

[4] Climate change task force – press release (bbhub.io)

[5] FINAL-2017-TCFD-Report.pdf (bbhub.io)

[6] FINAL-2017-TCFD-Report.pdf (bbhub.io)

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

{kind=link}

Biodiversity: Engagement for our nature

Around 8.7 million different species live on Earth – and they all provide important “ecosystem services”. This is precisely why the protection of biodiversity is essential. In the area of engagement, this year we are focusing on the chemical and pharmaceutical industry and are making contact with one of the world’s largest corporations in this sector.