After getting off to a good start at the outset of the year, economic recovery in China has recently stalled again. Following the lifting of stringent measures to contain the pandemic, the path out of the crisis is proving slower than expected. The weak global economy and flagging domestic demand, as well as the ailing real estate sector, have recently put a damper on the world’s second-largest economy.

China’s gross domestic product grew by only 0.8 per cent quarter-on-quarter in Q2, down from 2.2 per cent at the start of the year. Some recently reported economic indicators were also worse than expected; in addition, economists are also concerned about record youth unemployment and deflation. The Chinese government and central bank have already announced countermeasures. In view of the great importance of China as a major trading partner for a large number of nations, the situation in the country is also being keenly observed on the financial markets.

Note: Past performance is not a reliable indicator for future performance. Prognoses are not a reliable indicator for future performance.

Industry and Retail Presented Disappointing Figures

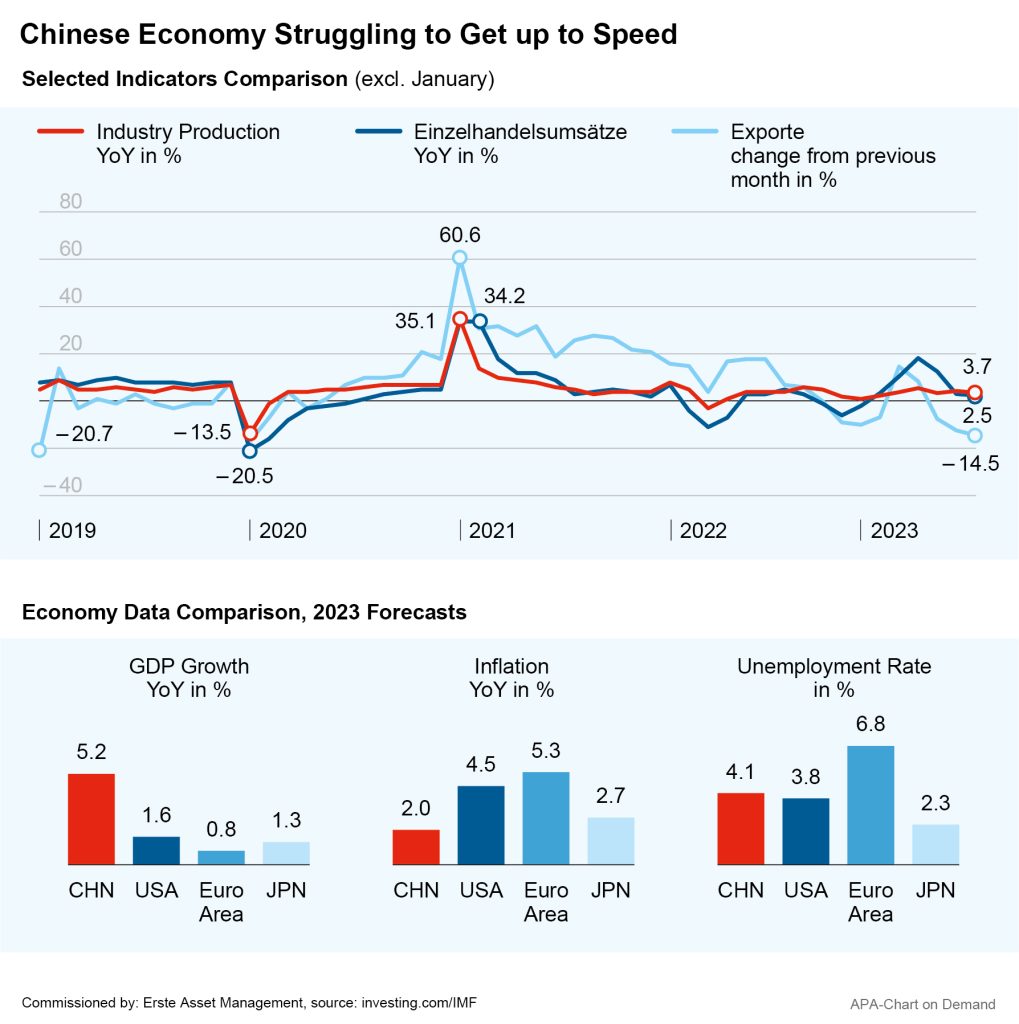

Industrial production and retail sales figures for July reported in the previous week fell short of analysts’ expectations and fueled economic concerns in the markets. Industrial production in China increased 3.7 per cent YoY, marking a decline from the 4.4-per-cent increase in June.

Retail sales, a key indicator of consumption, rose by 2.5 per cent, down from a 3.1-per-cent gain in June and the slowest growth since December 2022. In the financial markets, the figures gave rise to doubts that China will meet its already low 5-per-cent growth target this year. Earlier, officials also reported the lowest export figures since 2020 for July.

Add to that record youth unemployment and the threat of deflation. Consumer prices fell 0.3 per cent YoY in July, the first decline since February 2021, while producer prices have been on a downward trajectory for ten months – most recently falling by 4.4 per cent. Meanwhile, official labor market data show the youth unemployment rate at a record 21.3 per cent. Unofficial estimates see this figure as much higher in some cases. According to Zhang Dandan, economics professor at Peking University, the rate may have been as high as 50 per cent in March.

Real Estate Crisis Still Making Headlines

In addition, China’s important real estate sector has been in a severe crisis for some time. In addition to expensive bad investments by individual real estate developers, the introduction of new tough rules to reduce the debt of industry enterprises is considered the main trigger. In the meantime, Beijing has relaxed the regulations somewhat and signaled help for the industry. However, the crisis is now threatening to spread to the entire financial sector and is also affecting other areas of the economy, as the real estate sector in China has always been an important pillar of growth.

China Evergrande, the heavily indebted Chinese real estate developer, most recently filed for Chapter 15 creditor protection in the US. Evergrande is considered the most indebted real estate company in the world. The group had accumulated debts of over USD 300bn, growing unable to make interest payments on time. Most recently, however, the imminent bankruptcy of the project developer Country Garden also made headlines. Concerns about the industry were also fueled by recent data showing a decline in the prices of newly built homes.

The real estate developer Evergrande is more than 300 billion US dollars in debt. (c) HECTOR RETAMAL / AFP / picturedesk.com

Growth target likely to be missed

In view of the latest figures, the growth target of 5% for 2023 will probably not be reached, comments Erste AM chief economist Gerhard Winzer. With falling construction activity, a major growth driver for the Chinese economy has disappeared. At the same time, the structural risk is increasing with the falling real estate prices and the falling prices of goods and services. This is because both companies and consumers are under pressure to reduce debt and increase the savings rate, i.e. to consume and invest less.

Risk of liquidity trap

The risk of a so-called liquidity trap has thus increased. In this case, falling interest rates no longer support growth. Fears of such a development have existed for a long time, but recent economic data have made them more realistic. According to the textbook, stock prices, government bond yields and the currency are falling in China. However, the poor quality of data makes it difficult to assess the situation. After the significant increase in youth unemployment, the publication of data was stopped last week.

There are several scenarios to choose from for the future development, as Gerhard Winzer explains:

- a) Economic support measures are sufficient to stay on a growth path for GDP per capita.

- b) A slow adjustment similar to Japan after 1990, in which case prices stagnate and debt is slowly reduced.

- c) A quick adjustment via a recession.

The effects on the world economy are thus not yet clear. However, an important pillar of growth for the world economy would probably fall away. Economic policy in China is likely to have a significant influence on the likelihood of these scenarios.

Central Bank Lowered Key Interest Rates After Weak Data

The People’s Bank of China, China’s central bank, is looking to respond to the ongoing turmoil in the real estate market, planning to adjust and optimize its real estate policy soon. The central bank announced this last Thursday, after already having reacted to the weak economic data published in the previous week. Only one hour after the publication, it surprisingly lowered the key interest rates, making it the second rate cut within three months to counteract the rapid weakening of economic recovery.

The country’s securities regulator also wants to revive stock market trading and boost investor confidence with a whole series of measures. According to insiders and media reports, China’s major state-owned banks recently sold dollars on the foreign exchange markets in order to support the yuan, which is under a fair amount of pressure.

Government Plans to Support Recovery With Economic Stimulus Measures

However, experts also see China’s government obliged to support the recovery with stronger measures than have been taken thus far. The government already initiated taken a series of stimulus measures last month – from driving consumption of cars and household appliances to easing some real estate restrictions and supporting the private sector. In addition, local governments are to be protected in the event of debt problems. According to economists, high local government debt is a major risk to the financial stability of the world’s second-largest economy.

In any case, China’s government is bracing itself for a prolonged period of economic recovery, which will be a “bumpy and arduous process with difficulties and problems,” a Chinese Foreign Ministry spokesman said.

Conclusion by Chief Economist Gerhard Winzer

The combination of rising real yields and rising risks for China has led to higher risk aversion on the capital markets and thus falling share prices since the beginning of August. However, the rise in yields can be explained to a large extent by increased confidence in a “soft” landing in the US, i.e. a sustained fall in inflation without recession.

However, China remains a known unknown (“known unknown” according to Donald Rumsfeld). Similar to the central banks in the developed economies, economic policy in China will probably also be data-dependent, i.e. with little view into the future. Whether the measures taken by the central bank and the government in China are sufficient to reduce the downside risks and to increase consumer and business confidence, however, is something that not even China’s politicians are in a position to assess well.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

The Sahm Rule: What is behind the recession indicator?

The Sahm Rule, an important recession indicator in the US, was triggered at the beginning of August – causing uncertainty on the markets. We explain what is behind the indicator and why everything could be different this time.

International Monetary Fund/World Bank Group Spring Meetings 2024

At this year’s spring meeting of the International Monetary Fund and the World Bank, the focus was on the increasingly unlikely recession in the USA as well as the future monetary policy and the political situation. Fund manager Tolgahan Memİşoğlu reports on his impressions.

Trump on fire!

Donald Trump is getting serious and imposing temporary tariffs on his major trading partners. He is also escalating the war in Ukraine and increasing the pressure on Europe, which will hopefully soon be galvanized into unity with a new German Bundestag.