“SELL IN MAY AND GO AWAY (BUT REMEMBER TO COME BACK IN SEPTEMBER)”

Who has not heard of the old stock exchange rule “Sell in May and go away” – sometimes complemented by “but remember to come back in September”. We had a closer look at this adage and have analysed the performance on the global stock exchanges over the past 48 years. To this end, we looked at an index that measures exactly that: the company MSCI launched its MSCI World index on 1 January 1970, This is also the start date of our analysis.

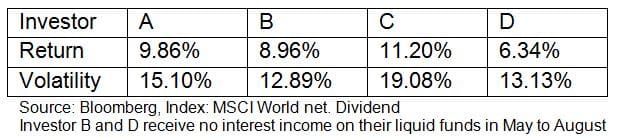

Given that the rule about realising one’s gains in May and returning in September was created in the USA, we are going to look at the performance from the perspective of a US investor as well as from that of a euro investor. These are our premises:

Investor A: fully invested at all times, referential currency USD

Investor B: fully invested with the exception of the months of May to (and including) August, referential currency USD

Investor C: fully invested at all times like A, but referential currency EUR

Investor D: investment pattern like B, but referential currency EUR

The four investors have achieved the following results since 1970:

Investor B is only invested for eight out of twelve months.

However, his/her return falls only slightly short of the performance of investor A. Statistically speaking, the return of B should be two thirds of that of A (equal distribution of monthly returns), i.e. 6.6%. At 9.0%, the return is significantly higher than that.

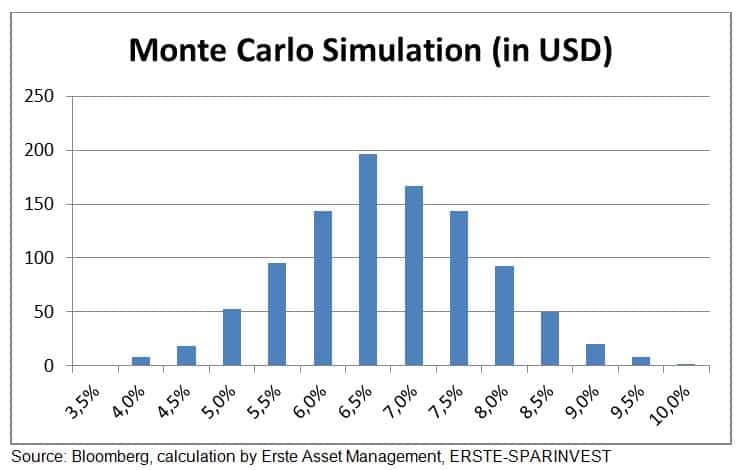

In order to analyse this performance in more detail, we resort to a so-called Monte Carlo simulation, a statistical method that in our case works as follows: we randomly select eight months and calculate the performance on the basis of realised monthly returns. This means that we want to find out whether the deliberate selection of four (non-invested) months deviates from a method that hinges on a random selection of four months. Taking this process through 1,000 iterations, this is the result we get:

The simulation confirms our earlier hypothesis, i.e. that a performance of 6.5% is the most frequent one. While a performance of 9% is not impossible, it is not very likely. More specifically, a performance of 9% or above occurs with a probability of 3%. In other words, the probability of error is 5% that the performance of investor B is significantly higher than expected.

This suggests that the stock exchange rule is justified. While the performance of 9.0% is less than 9.9% (for the case of permanent investment), it still beats the expected value of 6.6% by a significant degree.

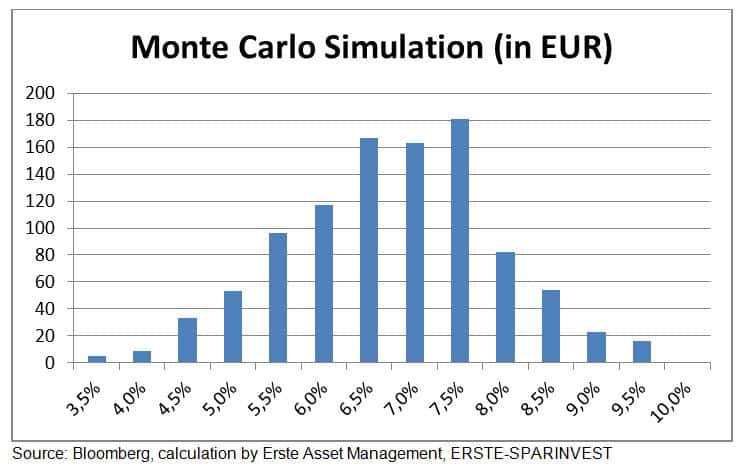

We now repeat the procedure for the euro investor. The performance of a buy-and-hold strategy is 11.2%. An investor implementing the stock exchange rule would achieve only 6.3%. The expected value for investor D is 7.5%, which means that the investor did not even match the expected value, let alone the result of investor C. The probability of the result being equal to or above 6.3% is 48%. This means that investor D achieved a result within the realm of expectation. Therefore, the stock exchange rule yielded a result within expectations for the euro investor (and nothing beyond that).

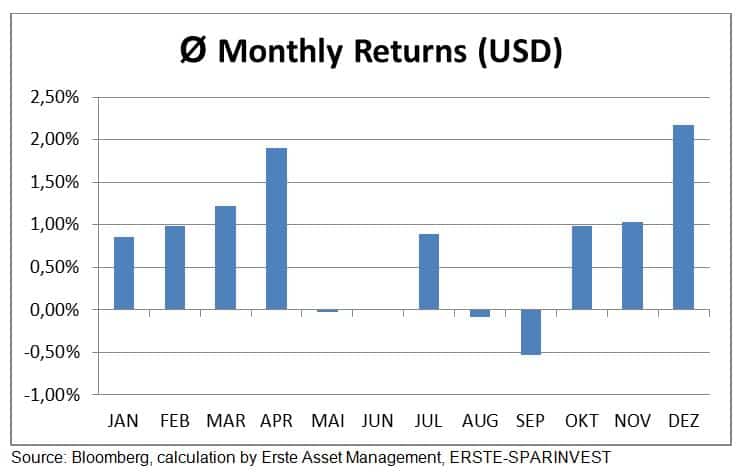

What catches our eye when we are looking at the average performance figures for the US investor across the individual months for the period of 1970 to today is the fact that the performance from October to May is far superior to the performance of May to September (with the exception of July). The chart therefore supports the stock exchange rule according to which being invested from May to September is not really essential.

The analysis supports another stock exchange rule, which says that winter performance beats summer performance.

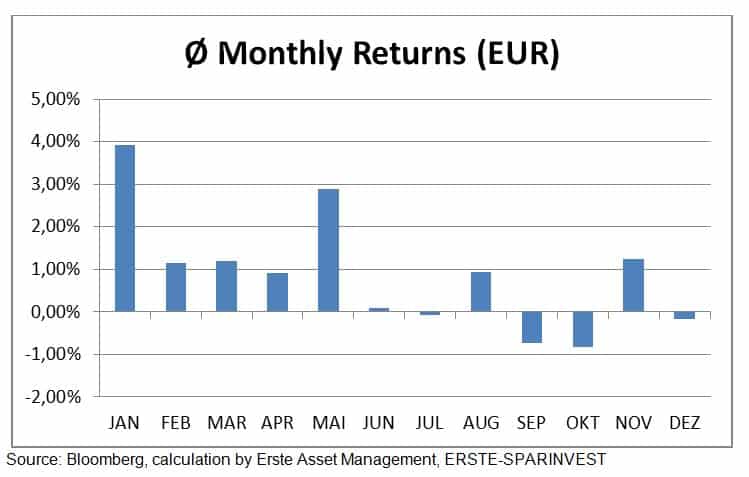

However, the performance for a euro investor looks significantly different. A US investor would realise the best result in December, whereas a euro investor would come out best in January. Whereas a US investor on average would not achieve a positive return in May, this month turns out to be the second-best one for a euro investor.

US dollar has a massive influence on the investment result

Our analysis reveals that the development of the currency strongly influences the result for a euro investor. Overall, the euro investor achieved a slightly better performance (11.2%) than the US investor (9.9%) due to currency gains. January to (and including) May are the best months for a euro investor.

In summary, the stock exchange rule “Sell in May …” is justified for a US investor. While he/she would not achieve a better result than with a permanently invested strategy, the performance is significantly better when taking into account that he/she is invested only for eight out of twelve months. For a euro investor, on the other hand, the rule has no justification, unless the US dollar is hedged against the euro.

But before we dismiss the rule for a euro investor altogether, let us introduce two additional investors E and F, who invest only in European companies (no currency risk).

Investor E: fully invested at all times, but Euro Stoxx companies (i.e. referential currency euro)

Investor F: fully invested in Euro Stoxx companies with the exception of the months of May to (and including) September

The result is striking: while pulling out for the months of May to September, investor F achieved the same return as investor E who was permanently invested. As a reminder: if I am not invested for four months (i.e. I am invested for 66.67% of the possible months), my return should reflect this shorter term of exposure, i.e. 9.64% x 2/3 = 6.43%.

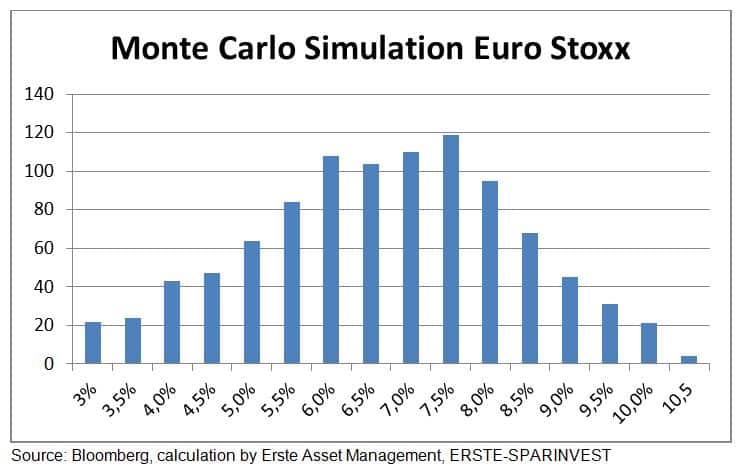

The Monte Carlo simulation (investments in eight randomly selected months on the basis of realised monthly returns) suggests a performance of 9.7% to be rather unlikely. The expected value is 6.4%. The probability of a result of >9.5% is 2.5%. This means that at an error probability of 5%, a performance of 9.7% is significantly higher than the expected value, which then re-introduces the rule “Sell in May and go away” as justified after all.

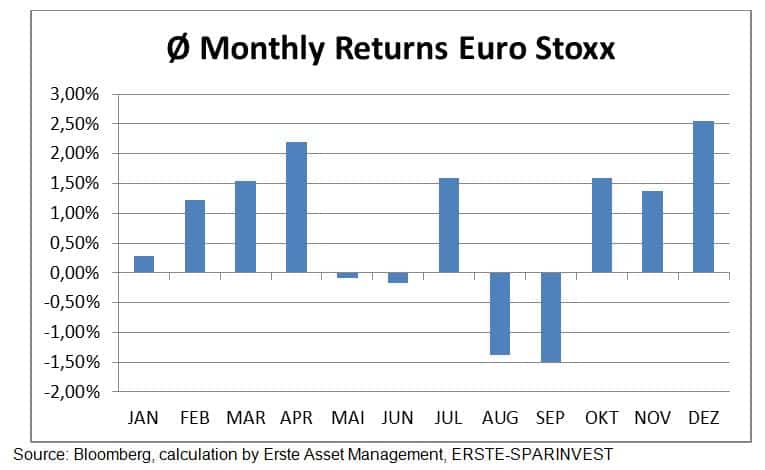

The average monthly returns of the Euro Stoxx index paints a similar picture as the MSCI World index in USD does. The months of May and June are weak. Here, too, July is the exception. Also, it seems there is no hurry when it comes to returning from your summer holidays. Re-investing in October suffices seeing as September would frequently produce negative returns. In fact, the month of September has been the weakest month for the Euro Stoxx index, historically speaking.

Our analysis shows that the stock exchange rule “Sell in May …” is valid also for a euro investor if he/she only invests in euro-denominated equities.

While this strategy does not necessarily generate a surplus yield, the investor hardly misses out by closing his/her positions for the summer months. In other words, the performance in the months of September to April is significantly higher than in the months of May to August. But this stock exchange rule has not worked in every decade. In the 1980s, an investor following this strategy would have clearly fallen short of the benchmark performance. The following table illustrates the average return for the periods of May to August and September to April by decade.

These considerations are interesting for euro investors. Currency fluctuations dilute the performance significantly for internationally diversified portfolios and do not produce the desired improvement in risk-adjusted performance. By investing only in Euro Stoxx companies, one creates a different scenario. The stock exchange rule is valid again.

As a side note, we did not include transaction costs or taxes in our calculations. The purpose of our analysis was of a statistical nature.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Trump and green stocks – Interview with fund manager Alexander Weiss

Environmental stocks have corrected sharply in some cases as a result of the US election. We discuss with Alexander Weiss, fund manager of the ERSTE GREEN INVEST, how our fund management is positioned and what opportunities are arising for renewable equities.