Anton Hauser, senior fund manager at Erste Asset Management and expert for Central and East European (CEE) government bonds

Anton Hauser has been senior fund manager of ERSTE BOND DANUBIA for numerous years. The expert for Central and East European (CEE) government bonds has received several national and international awards. In this interview, he talks about the difficult first half of 2018 and illustrates possible future scenarios.

The CEE bond markets have come under significant pressure in recent months. What have been the crucial factors for this development?

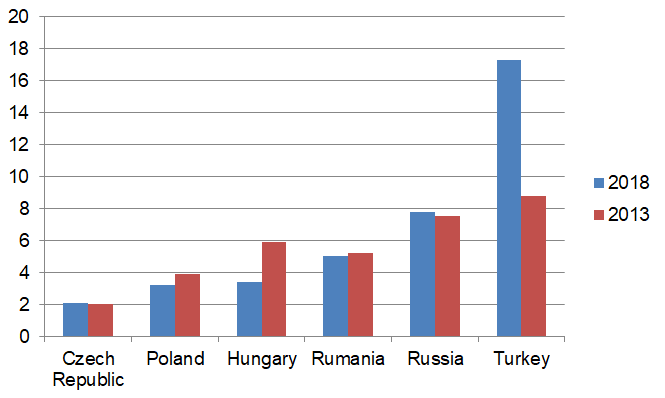

The increase in bond yields (see table below) and the currency depreciation experienced by Central and Eastern Europe vis-à-vis the euro have been triggered by country-specific as well as geopolitical factors (e.g. rising commodity prices). The tighter monetary policy of the US central bank and the approaching end of the bond purchase programme of the European Central Bank has led to capital outflows from the emerging markets (and emerging markets funds). As a result, the pressure on CEE investments has increased. Also, a possible cut of transfer payments in the new EU budget has had a negative impact.

10Y yield of government bonds by comparison

(in %)

Source: Bloomberg, 20 July 2018

Note: Past performance is not indicative of future development.

How big is the risk of inflation becoming excessive in those countries?

The CEE countries are currently not running any significant macroeconomic imbalances. The increase in inflation – with the one in Turkey standing out at 15% (source: Bloomberg, 20 July 2018) – has been caused mainly by the rising oil price despite the substantial wage increases that we have seen. We do not expect core inflation to accelerate significantly in the region. Therefore, we only expect moderate interest rate increases and regard the most recent sell-off in the region as excessive.

You invest in the new EU member states as well as in bonds from Turkey and Russia. What sort of weighting do you keep, and how do you assess the foreseeable future of those countries?

Russian bonds in the fund are currently weighted at 13%, Turkish bonds at 14% (as of July 2018; source: Erste AM Fund Management).

The situation in Russia is largely stable. While debt levels are low, the high oil price supports economic growth. Due to the sanctions, the number of new issues is also very limited. Bonds falling due are reinvested in existing bonds. Given this scenario, the Russian economy should be developing relatively well in the coming months.

The situation in Turkey on the other hand is difficult. A massive current account deficit, high short-term liabilities, an overly loose monetary policy in connection with high political risk have caused a crisis of trust and put pressure on Turkish bonds and the currency. At the moment, there are hardly any signals to suggest what the economic policy might look like under the new presidential system. The most recent decision by the central bank, to refrain from hiking interest rates despite the high rate of inflation, came as a surprise and left many questions unanswered. The uncertainty on the Turkish capital market is accordingly high. That being said, as fund manager one cannot disregard the high yields of a currency that has already depreciated substantially. And lastly, I should like to point out that Turkey is experienced in handling high inflation and is well known for its unconventional monetary and fiscal policy.

Over the years, CEE bonds have repeatedly gone through phases of falling prices. Should the recent corrections be used to increase positions?

Falling prices lead to rising expected yields. Historically speaking, expected yields would be reflected quite well in actual yields. We believe that the situation this time will not be much different than previous ones.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Is the AI Rally Nearing its End?

Following this week’s interest rate cut by the US Federal Reserve, shares related to artificial intelligence (AI) applications are once again in the spotlight. Investors are hoping that AI will have a positive impact on the business figures of the key players. With the ERSTE STOCK TECHNO fund, you can invest in the most important companies in future technologies.