The global economy continues to face the aftermath of the two-stage inflation shock, first pandemic, then energy. Monetary policy has since corrected the ultra-expansionary monetary stance. However, the immediate dominant macroeconomic issue remains the excessively high inflation trend.

No “No Landing”

Hopes that inflation would fall as quickly as it rose (Immaculate Disinflation) were dampened. The “No Landing” scenario was just flawless (Goldilocks). The somewhat more realistic assessment, according to which weak demand (“soft landing” including stagnation or even mild recession) could reduce inflation, has also become less likely. In both scenarios, key rate cuts were conceivable from the second half of the year, which would have supported the markets.

High inflation rates

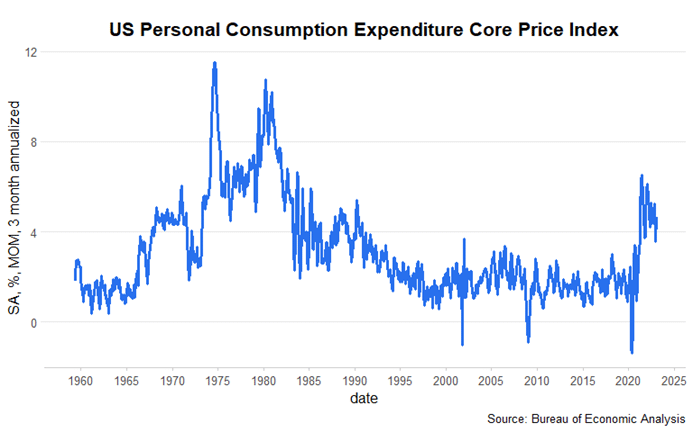

Inflation rates were too high in some countries in January, many important economic indicators rose and unemployment rates remained very low. In the US, the deflator (the inflation rate) for personal consumption expenditures was above expectations in January (0.6% month-on-month). Excluding the normally volatile components of food and energy, the price increase was also 0.6%. If this figure is extrapolated for the year (0.6% times 12 months), the annualized value is around 7.2%.

This value is far from a development with which the central bank can be satisfied. At the end of the week, the focus in the euro zone will be on the flash estimate for consumer price inflation for the month of February. The consensus estimate expects an unchanged high value for the core rate (5.3% yoy).

Note: Past performance is not a reliable indicator for future performance. Representation of an index no direct investment possible.

Rising economic indicators

The aggregate flash estimate of purchasing managers’ indices (PMI) for major developed economies showed an increase for the second consecutive month in February. The PMI for the manufacturing sector indicates a bottoming out or slight growth. Global manufacturing contracted in the fourth quarter. The services PMI rose more than the manufacturing PMI. With a value of 51.5, the indicator is now back above the theoretical threshold of 50 that separates expansion from contraction.

With regard to the subcomponents, the increases in new orders and sentiment are worth highlighting. The employment sub-indicator has also improved. However, due to the tight labor market (low unemployment rate), there are risks of secondary round effects (excessively high wage growth). At the same time, it is worrying that the indicator for sales prices in the service sector did not continue the downward trend with a slight increase. This development provides an indication that companies have pricing power.

Inflation persistence

The assessment that the disinflation process will be slower than hoped for and bumpy is becoming increasingly accepted as the baseline scenario. The risk of inflation persistence becoming too high or of a renewed acceleration of inflation has even increased.

Too loose monetary policy – increased recession risks

Central banks were unable to do much about the supply-side shocks (high energy prices, supply bottlenecks). However, the underlying monetary policy stance was (much) too loose in hindsight. This environment has facilitated pass-through and secondary round effects. Currently, the combination of too high inflation rates (a too-slow disinflation) and rising economic indicators is worrying central banks. The risk of anchoring inflation expectations at a level above the central bank target (of 2%) has increased.

However, central banks can affect demand (economic growth) with a restrictive monetary policy. The probability of additional key rate hikes has increased. In the USA, further interest rate hikes of almost one percentage point are included in the market prices until July (upper band for the effective key interest rate currently: 4.75%). In the euro zone, too, a key interest rate increase of around one percentage point is priced in by July (deposit facility currently: 2.5%). However, this has also increased the risk of a recession triggered by the central banks.

High fluctuations

Central banks and probably also some market participants now have little confidence in their own forecasts of inflation and economic growth. Consequently, they are acting even more than before on published indicators. However, these are prone to fluctuation. Since the beginning of February, expectations for future key interest rates have risen, putting bond and equity prices under pressure. Higher interest rates reduce the present value (current value) of future cash flows (dividends, coupons). In addition, the increased probability of recession in the medium term reduces expected profits. However, one or the other unexpectedly rapid fall in inflation would once again support share prices.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Trump’s tariff plans: a game with no winners?

On 20 January, the world will once again look to Washington with anticipation as Donald Trump is sworn in as US President for the second time in front of the Capitol. In any case, his statements and plans are already the focus of attention on the financial markets.

Trump is planning high import tariffs for goods, for example from Mexico and China. The possible consequences range from the threat of a trade war to a comeback of inflation. In the end, will no one benefit from the planned tariff measures?

Autumn on the stock markets will be anything but boring

Election campaign, interest rate turnaround, sluggish growth in Europe – there should be no sign of autumn fatigue on the stock markets. What will the coming (and certainly exciting) weeks bring for the markets and how can investors prepare for them?