It would appear that Donald Trump – who, until recently, liked to portray himself as the “peace president” – has taken a liking to war. Back in January, he caused an international stir by ousting Nicolás Maduro in Venezuela, and one somehow cannot help the impression that Venezuela served as a blueprint for the “Epic Fury” mission in Iran. Six weeks later, we now know that the mission is proceeding anything but according to plan and is more akin to an “epic failure”.

The regime change in Iran has not succeeded, and even though the US-Israeli alliance has caused massive damage to the military infrastructure, hundreds of Iranian drones and missiles were still flying towards Israel and the neighbouring Gulf states on a daily basis right up until the very end.

After all, the Iranian regime has been preparing for this contingency for decades, and as the current course of the conflict shows, the plan appears to be working. In particular, the spread of the escalation across the entire region and the closure of the Strait of Hormuz are exerting maximum pressure and causing the greatest possible economic damage. In contrast, the USA appears increasingly haphazard from week to week, and Donald Trump’s latest remarks seem to be paving the way for a face-saving US withdrawal, even without any real success. A protracted and, above all, costly war is unpopular in the United States and would further diminish Trump’s chances in the mid-term elections this autumn. The ceasefire announced at the start of the week is, in any case, a step in the right direction, even though the negotiations have not yet yielded any real progress.

Energy prices are becoming a burden

Regardless of how the conflict unfolds or how long it actually lasts, it is clear that higher energy prices will weigh on the global economy. The key question in this context, however, is the duration and scale of the energy price shock. Last week, the OECD became the first multilateral organisation to issue an assessment of the impact of the current energy price shock and sees global growth, at 2.9%, remaining on a resilient growth trajectory.

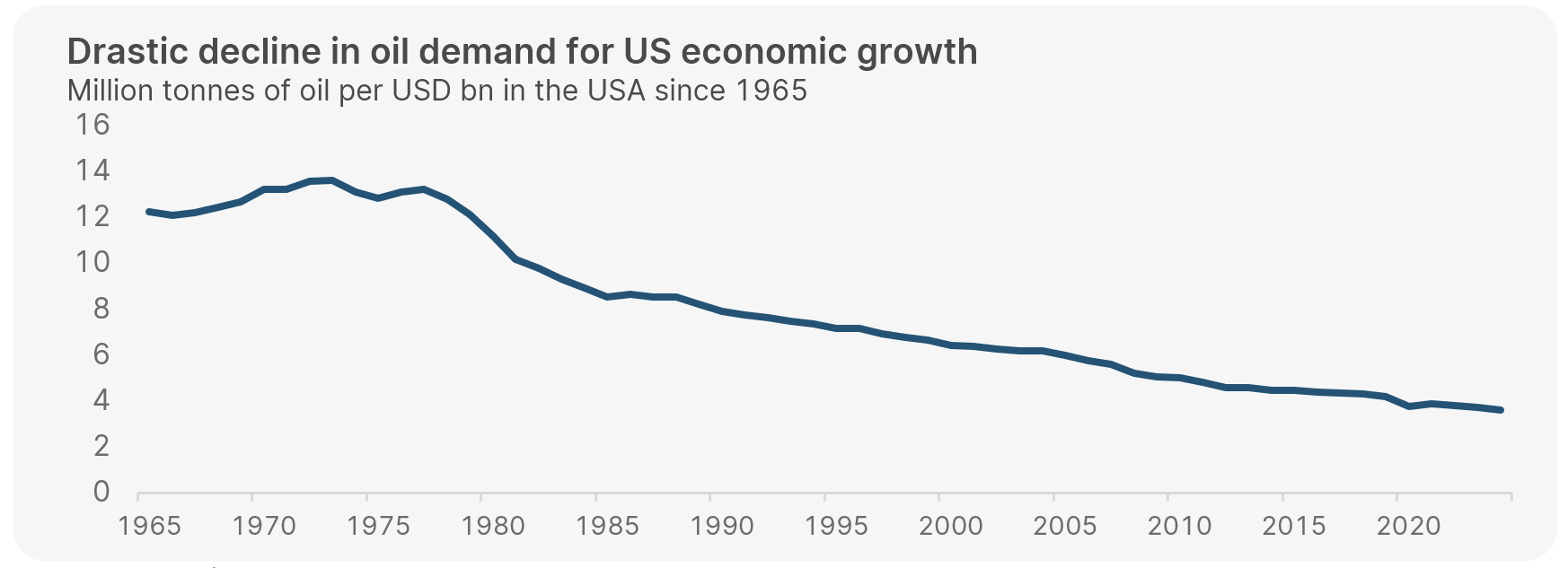

For the time being, the effect is therefore dampening but by no means recessionary – the comparisons often drawn with the oil crises of the 1970s seem in any case to fall short, for as the chart below illustrates using the example of the United States, the dependence of economic growth on crude oil has fallen dramatically over the past 50 years.

Source: Energy Institute, World Bank, Data as of 3.3.2026

Adjusted for inflation, the price of oil would need to rise significantly further to reach levels comparable to those seen during past energy crises. That being said, in the long term, higher energy prices will certainly increase the risk of a significant slowdown in growth, which could subsequently lead to stagflation or, in extreme cases, even a recession. A quick glance at the petrol pumps here suggests that it is only a matter of time before consumer confidence faces further headwinds.

In addition to the immediate price rises in the energy sector, the knock-on effects must also be closely monitored. Commodity prices have already risen across the board, and the conflict will also have a negative impact on food prices. The fertiliser industry, in particular, is affected in two ways – on the one hand, production is heavily dependent on natural gas, and on the other, a third of global fertiliser exports pass through the Strait of Hormuz.

Initial figures are already showing the immediate impact on inflation in March – for instance, the consumer price index in Germany recently rose to 2.8% from 2.0% in February.

Central bank again between a rock and a hard place

The current rise in inflation is already bringing back memories of 2022. Back then, too, the war in Ukraine had triggered a shock in energy prices and inflation, to which central banks were forced to react far too late with massive interest rate hikes. This comparison is somewhat flawed, however, because unlike today, the inflation momentum four years ago were heavily influenced by pandemic-related measures. Furthermore, central banks were starting from a completely different interest rate level.

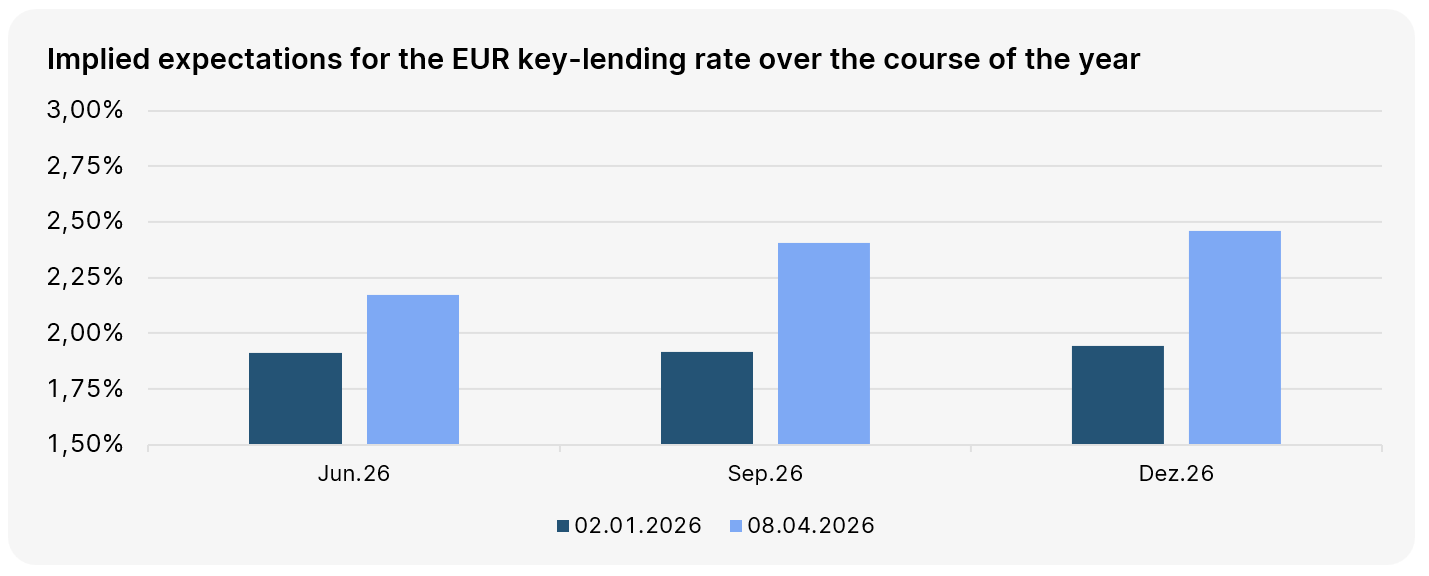

Nevertheless, the current situation is anything but pleasant for central banks and, by extension, for the capital markets. The path of monetary easing that was clearly signalled at the start of the year – with key-lending rates expected to remain flat or even fall – has been rapidly priced out of the markets. The chart below compares current market expectations regarding key-lending rate trends with those prior to the Iran war. Instead of the originally expected sideways movement in Europe, the markets now anticipate at least two interest rate hikes by the end of the year – a situation similar to that in the United States, where two expected rate cuts were recently priced out of the market.

Source: LSEG Datastream, Data as of 8.4.2026

Central bankers are thus once again faced with the dilemma that combating inflation through higher interest rates simultaneously weighs on the economy. Even though the market expects central banks to prioritise the fight against inflation, it is hardly surprising that both the Fed in the USA and the ECB are, for the time being, “playing for time”. Ultimately, the duration of the conflict will play a key role here too, and a data-dependent approach leaves little scope for a hasty 180-degree U-turn in monetary policy.

Is private credit turning into a problem?

Naturally, the Middle East conflict has been the focus of media coverage in recent weeks. Away from the spotlight, however, another issue has emerged in parallel that could also pose a significant risk to the financial markets – private credit.

This refers to a credit market now worth USD 2 trillion, which has developed in recent years outside the traditional and generally heavily regulated financial system. In the past, these companies and funds have increasingly financed technology and software firms whose business models have recently come under growing scrutiny due to disruption caused by AI. Out of concern over potentially non-performing loans in their portfolios, numerous well-known providers were therefore confronted in the last quarter with high redemption requests from clients, which cannot be met, or only to a limited extent, due to restricted liquidity. Through so-called “gating”, i.e. the limitation of payouts, providers generally have good options for maintaining the stability of the fund.

Still, concerns remain about a broader risk of contagion, including within the traditional banking sector. Given the limited transparency and regulation, it is reasonable to assume that the segment will remain under pressure, although the existing risks do not appear to be systemic due to the long-term capital structures.

Mad world

Although external shocks have become a common occurrence in the capital markets in recent times, investors’ nerves are currently being put to the test once again. Particularly when the president of the United States conducts diplomatic negotiations via social media and causes fresh irritation almost every hour, market volatility is inevitable. Trump’s threat of genocide represents an absolute moral low point and also demonstrates that the world’s most dangerous president is currently not sitting in Moscow, Beijing, or Tehran, but in Washington. As so often in the past, it was perhaps just another bizarre negotiating tactic which, in hindsight, worked once again. The ceasefire and, above all, the immediate reopening of the Strait of Hormuz triggered a veritable surge in share prices and is also fuelling hopes of an imminent end to the war.

Positioning in Discretionary Portfolio Management

In view of the continuing uncertainty surrounding the course of the war, we remain defensively positioned for the time being. Even if the oil tankers are able to sail again, the energy markets are likely to take a few more months to normalize. It can also be assumed that the upcoming negotiations could prove to be quite bumpy, meaning that volatility on the markets is likely to remain high in the short term.

We are therefore sticking to the underweight position in equities we took at the beginning of the war and are trying to be as broadly diversified as possible in terms of regions and styles. A similar approach was taken in the bond segment, where we reduced risk slightly by taking profits on emerging market bonds. As part of the reallocations, we have also included a broad commodities basket in the investment alongside a significant increase in money market investments.

The coming weeks are crucial: the latest energy price-driven impetus is currently not enough to overturn the basic scenario of inflationary growth. If the conflict is resolved quickly, market setbacks could represent long-term buying opportunities, while a further escalation is likely to trigger significantly stronger market reactions. At the same time, it has been shown that markets and companies are now more resilient to external shocks than in the past, meaning that the economy has also become more resilient.

Please note: investing in securities involves risks as well as opportunities.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Emerging markets bonds and sustainability: How do these two go together?

Lower interest rates in the USA mean that investments in emerging markets are becoming more attractive. The ERSTE RESPONSIBLE BOND EM LOCAL fund, which received the Austrian Ecolabel in August, could also benefit from this.