The current period, although not entirely perfect, could be from multiple perspectives called a golden age.

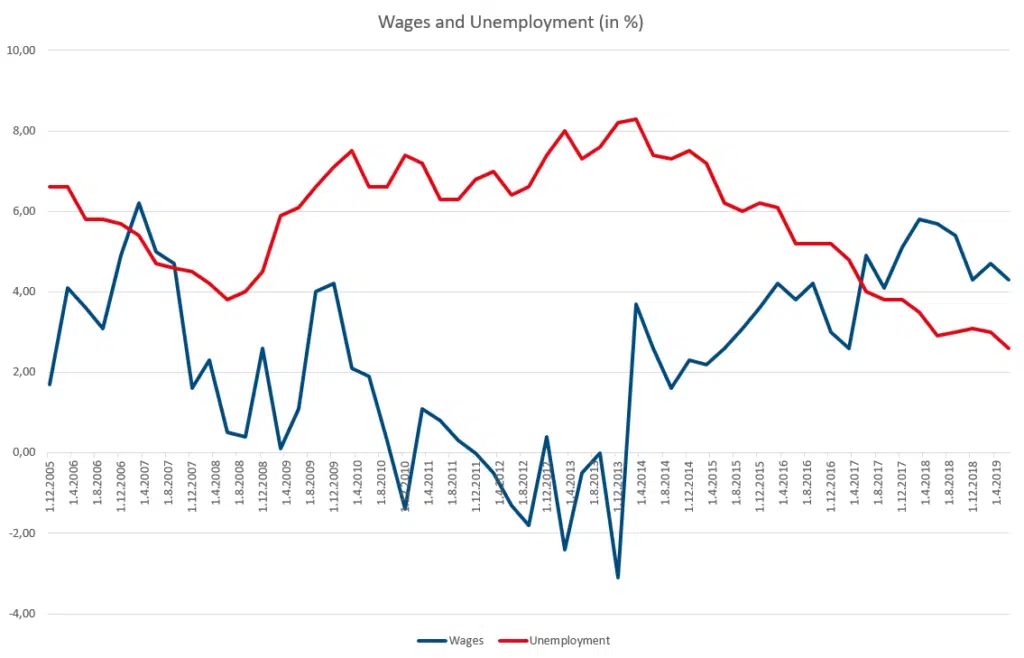

The unemployment is at record lows and a number of companies just lack employees, wages grow at probably the best pace since the global financial crisis, social policies gained speed.

Consumers buy a lot of other than necessary goods and are willing to pay up for quality. Apart from that, they purchase real estate and the prices have been driven to record levels.

But just how golden is the current period indeed?

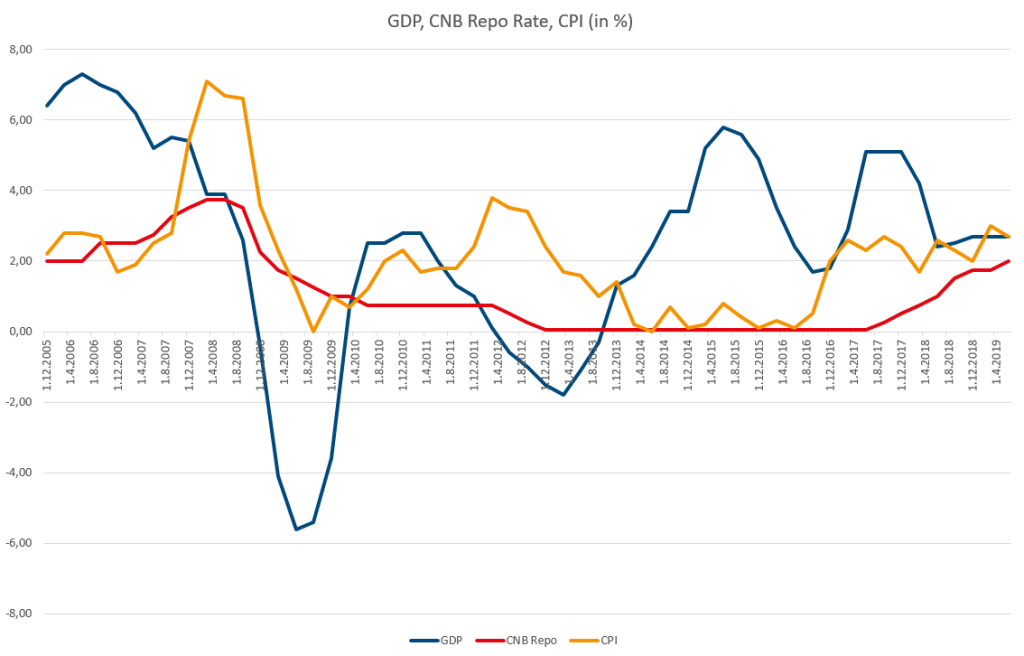

After the global financial crisis of 2008-2009 the Czech economy, thanks to the relatively quick fiscal and monetary policy response, recovered, but not for very long. Throughout 2011-2013, GDP growth was back on the declining trend and the already relatively high unemployment began to rise.

Inflation was heading downward and fears of a deflationary spiral emerged. The Czech National Bank (CNB), in its efforts to support the economy, got interest rates down to the so-called “technical zero” (0.05%).

After the interest rate arsenal had been depleted, the CNB decided to embark on FX interventions and devalued the domestic currency in November 2013. By supporting the export-oriented manufacturing sector (among others), it thus managed to uphold the economic activity.

Over time, the unemployment consistently declined, GDP growth picked up and gained pace and so did wage growth, fuelling inflation pressures. Domestic demand was, apart from the foreign demand, one of the drivers of economic growth. On the supply side, manufacturing fared pretty well.

Not only domestic fiscal and monetary policy, but also favourable developments at main foreign partners were among the factors that helped create an environment of certain prosperity.

Source: Bloomberg/Czech Statistical Office

Developments after foreign exchange intervention

After more than three years, in April 2017, the CNB discontinued its FX intervention policy. This was not without snags though. It is perhaps easier to initiate FX interventions than to exit from such a regime. Because of the solid economic fundamentals among others, there was a widespread view that the fundamentally justified CZK exchange rate should be substantially stronger than the one artificially sustained by FX interventions.

A lot of speculative capital rushed into the economy in anticipation of an abrupt and pronounced strengthening of the Czech crown.

Shortly before the estimated exit from the FX intervention regime, the speculative inflows intensified so much that, at one point, the market players realised that the currency was overbought, which could definitely prevent them from realising any immediate gains.

They subsequently rebuilt their strategies so as to be able to profit from them in a longer term. In the end, the exit from the intervention regime indeed did not cause the crown to strengthen as much as had initially been expected.

The accelerating economy, coupled with the still rather weak crown, led the CNB to begin a monetary tightening cycle, which has by now comprised eight interest rate hikes.

Stricter regulations in the banking sector

Together with the more stringent guidelines for the banking sector, elaborated in an attempt to stem the potentially developing housing bubble, and the already elevated real estate prices, these rate increases have managed to significantly cool down the mortgage market.

On the other hand, the limited housing availability, so often mentioned in the media these days, is not a great advantage for the economy.

Source: Bloomberg/Czech Statistical Office, Czech National Bank

In an environment of low expected returns on savings, partly caused by global conditions, as well as the speculative inflows, and due in part to the less strict amended bond market regulations, bonds issued by smaller companies found their place in a number of retail investors’ portfolios, not infrequently without proper assessment of investment suitability.

Such bonds tend to have higher yields than broadly accessible standard investment products. To the public that had not yet forgotten the convenient saving via bank accounts bearing adequate interest (in earlier times) these bonds looked attractive.

Are there any greater risks these days?

Escalating global trade conflicts and the struggling German economy (among others), to which the Czech one is closely tied, were able, together with the monetary tightening that was already being conducted, to moderate the economic growth.

It cannot be ruled out that these factors will eventually pass and the Czech economy will avoid further slowdown in the near term. However, it is also possible that the external factors have not yet manifested themselves to the fullest extent and that a more marked slowdown lies ahead.

For now GDP growth is, despite some deceleration, solid, the labour market is still strong and inflation remains quite robust. There is thus little (if any) reason to loosen monetary policy. Due to the global uncertainties and the already moderating inflation pressures, monetary tightening probably does not seem to be an option either. At the September 25th meeting, the CNB did refrain from changing its policy rates.

The massive volumes of speculative capital (according to some estimates, total FX intervention volumes surpassed as much as 43% of GDP) create an imaginary resistance level for the Czech crown. It can be assumed that a large part of that capital still remains in the economy. Although the share of government debt held by non-residents has been declining (with alternating success), the pre-intervention levels have by far not been reached. (This share amounted to 36.99% in July 2019, 41.43% in March 2017, and only 10.75% in October 2013.)[i]

So far, the behaviour of non-resident investors remained more or less stable. Sometimes though, warnings can be heard that their eventual exit en masse could cause turbulence in the FX market.

What is the pattern of investor behavior?

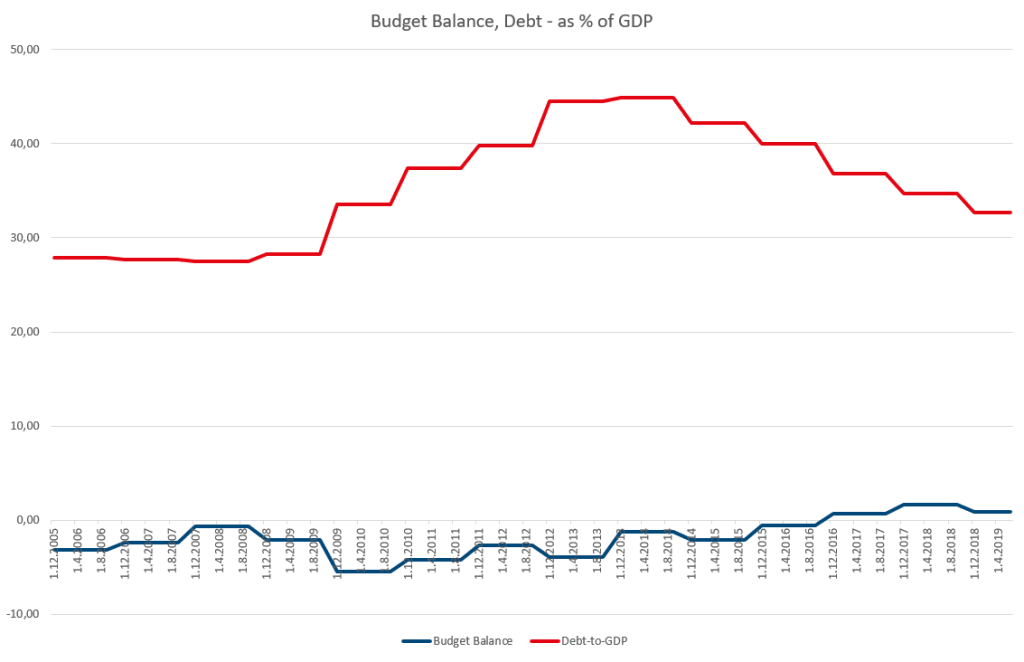

Although not everything is perfect, the financial situation of many social classes is getting better nowadays. Criticism nonetheless intensifies that a budget cushion is not being built during good times, and that the decelerating economy, for instance, can take its toll on that. The Czech Fiscal Council warns against the apparently unsustainable public finances in the long run.

Among the recommendations that the European Commission gave the Czech Republic there are those regarding needed improvements in the long-term sustainability of the pension and healthcare system. Up until now, the fiscal situation has been rather healthy, however, should the current developments continue for a long time, the public finances might no longer look so in international comparison, which could draw attention in the markets at some point in the future.

Source: Bloomberg/Eurostat

Should we worry or should we be carefree?

For now, it appears that overly strong pessimism would probably be misplaced. The domestic economy looks quite resilient to the foreign developments, the consumer is still strong, the CNB’s interest rate cushion for the eventual (so far not very probable though) threat of recession is, in international comparison, sizeable and the fiscal position is, in historical, as well as international, perspective, solid.

A number of already mentioned risks could have an impact on each of these elements. Whether these risks materialise, would not depend on domestic factors only.

A further escalation of global trade conflicts, a more pronounced deceleration in China or in Germany (eventually in other countries) and the subsequent impact on the Czech economy, deteriorating sentiment towards markets such as the Czech Republic, or a whole range of other factors could prompt the situation to take quite a different turn.

To us, a partial deceleration of growth, not a recession, still remains the most probable scenario.

[1] https://www.mfcr.cz/en/themes/state-debt/debt-statistic/by-type-of-holder

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Nationalist forces strengthened in the EU: what could be the consequences?

In the EU parliamentary elections, right-wing parties made significant gains in some major countries. In France, early elections are now on the cards following President Macron’s defeat. What possible effects could a shift to the right have in the EU?