In mid-August, a dip in the New York stock exchanges caused a fair stir.

Both the Dow Jones Industrial Index and the Nasdaq Composite Index dropped by more than 3 per cent each on 14 August, resulting in massive index losses on stock markets worldwide. Even though signals of an easing in the trading dispute between the USA and China had actually created an excellent mood among investors in the days just prior to the event.

Nor had US President Trump not made a conspicuous statement. So what had caused the sudden slump in the stock markets?

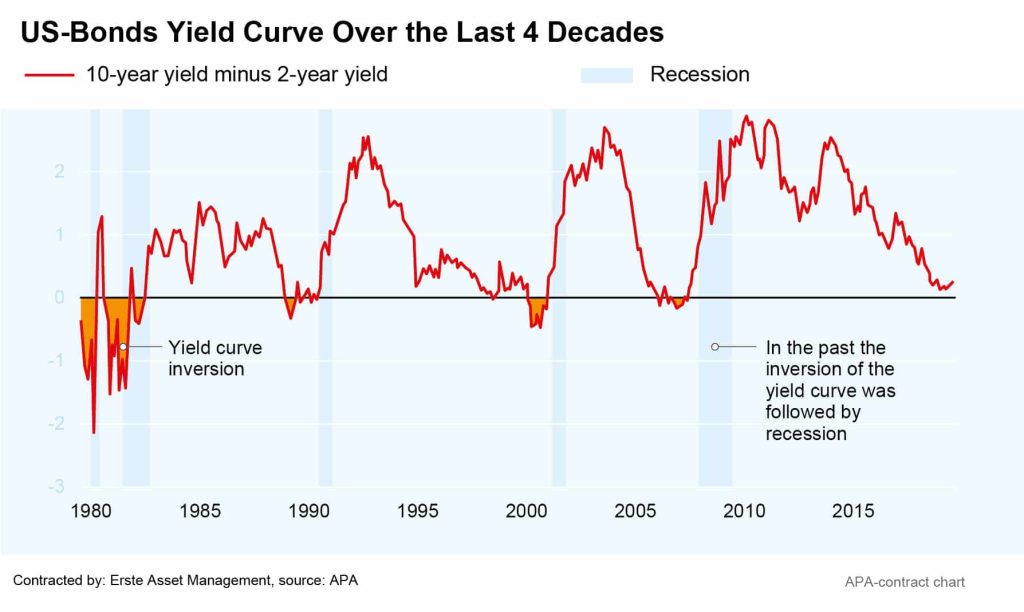

What the yield curve reveals about growth expectations

In the US bond market, the yield on two-year government bonds had risen above the yield on ten-year bonds, creating the rare situation of an inverse yield curve. This was last the case in 2007.

All recessions in the US economy over the past five decades were preceded by an inverted yield curve; it is therefore regarded as a reliable harbinger of a recession.

The reason for this is that, when investors lend money to the state, they are usually satisfied with a lower yield on short-term bonds than on bonds that run for ten or more years.

The logic behind this is simple: the shorter the term, the more manageable the risk of the investment and thus the lower the required interest rate.

But why does the inverse yield curve play such a major role?

An inverse yield curve indicates that the investors’ assessment has reversed. They then consider the short-term risk to be higher than that for longer-term investments.

In other words, they think it is possible that economic growth will slow down to such an extent that it will be more difficult for the state to repay its debts.

At the same time, they expect lower interest rates in the long run because they assume that the central banks will have to help the economy with cheaper money.

In this environment, it is also more costly for companies and consumers to borrow money in the short term. They therefore postpone investments and purchase decisions because they assume that interest rates will drop again at another point in time.

This reduces investments and consumption, which make up a large part of economic activities, and thus actually reduces economic growth.

Why the yield curve has inverted

The yield on short-term bonds depends strongly on the interest rate policy of the respective central bank, because key interest rates have a decisive influence on the attractiveness of other financial products.

Long-term government bonds are more likely to be influenced by inflation expectations, as investors pay particular attention to value stability during long maturities.

In recent years, the Federal Reserve (Fed) has gradually raised interest rates, driving yields on two-year bonds. When it surprisingly announced in March that it was loosening the monetary policy again, the yield curve normalised.

However, when the Fed finally lowered key rates in July for the first time since 2008, the yield curve flattened further and finally inverted.

The reason for this is increasing concern that the weak global growth will continue to spread, driven by trade conflicts, and that a looser monetary policy alone will no longer be sufficient to compensate for that.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Shift in risks

Both the markets and central banks are pointing to a shift in economic risks from inflation towards growth. The focus is currently on the US labor market.

Eastern Europe: Economies expected to outperform Euro Area

Weakening growth in the eurozone has been an issue on the markets for some time now. In the Central and Eastern European countries, however, this is largely a non-issue. According to forecasts, the region is also likely to grow faster than the eurozone this year. Private consumption in particular has recently proved to be a growth driver. However, the tense situation in German industry is causing concern.