Imagine a fairy that grants you three wishes. What would you wish for? The answer would be very easy for me. I would just like to know if the economy is caught up in a recession of has embarked on an expansionary phase a year from now. And whether the central bank will be pursuing an expansive or restrictive policy. If I got these two wishes granted, I would even forego the third one. Or, as a good fund manager, I might engage in risk management and save up for bad times. Growth and monetary policy are of significant relevance to the return of almost all asset classes.

US central bank increases Fed funds rate: was that it, or is there more to come?

The World’s most important central bank, the US Federal Reserve, increased its most important key-lending rate, the Fed Funds rate, by 25bps to a target band of 1% to 1.25% on 14 June. This prompts the question of whether this was it, or if there is more to come. I personally am convinced that the US central bank will tighten its monetary policy further in the coming months. There are several reasons for this. I would like to discuss one of them in the following.

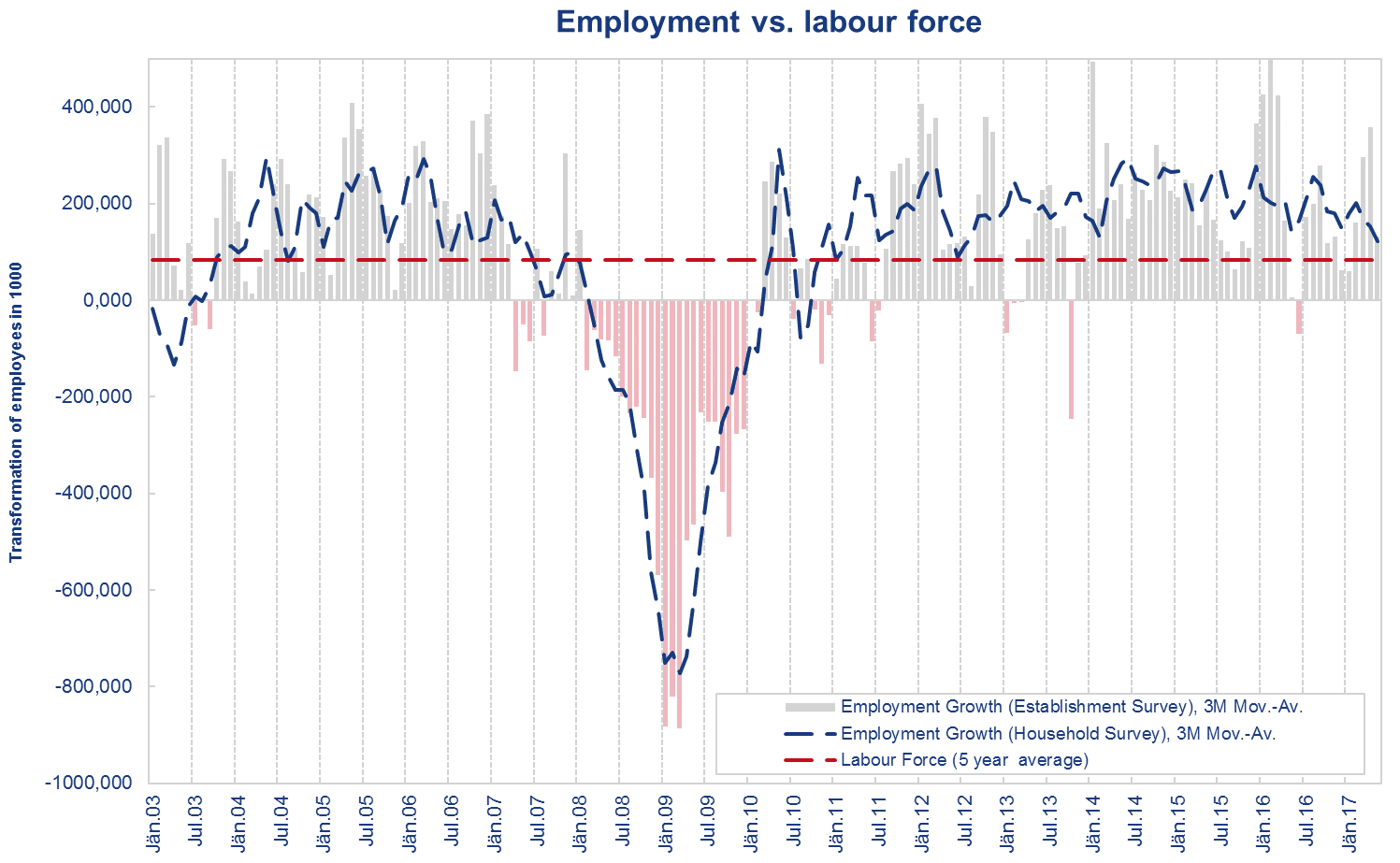

The chart above juxtaposes supply and demand in the US job market. The supply of labour force hinges on two factors: the change in the number of people at an employable age and the percentage of people thereof who are looking for work (participation rate). In the chart, the red line illustrates how many people on average have entered the labour force in the past five years. At the moment, the number averages 80,000. This means that every month an average of 80,000 have entered the job market.

Job growth in the USA

The fact that there is also a blue line and bars in the chart that represent the newly created jobs per month is based on the statistical approach taken in the USA. Here, two statistical models are used to establish these numbers. On the one hand, a so-called household survey is made among private households. On the other hand, a survey establishes what employment status companies report (establishment survey). Both numbers may differ significantly from month to month, which is why for a short-term market assessment it is important to look at both. In the long run (as also manifests in the chart above), they paint the same picture: on a 3M average, the US economy has created 120,000 (Household Survey) or 130,000 (Establishment Survey) jobs, respectively, per month. The chart also illustrates the fact that the US economy has constantly created more jobs than would have been necessary to accommodate the additional labour force. This, in turn, results in a decline of the unemployment rate, which at this point is already extremely low, also from a historic perspective.

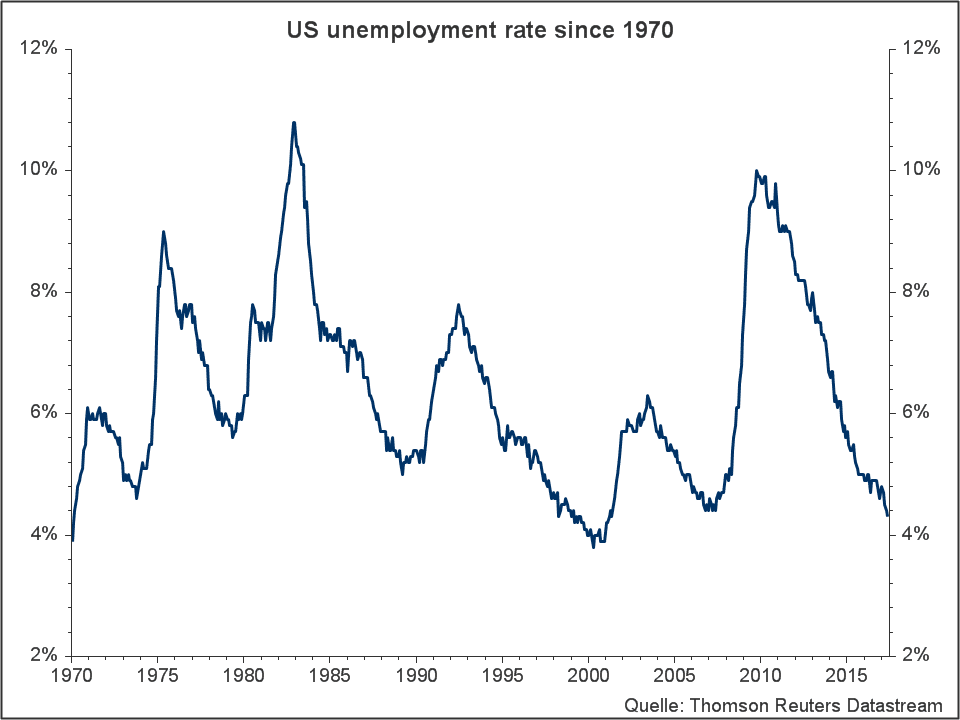

Given that about 80,000 people enter the job market per month and about 125,000 jobs are created per month, the demand for labour force exceeds supply. As a result, the unemployment rate is falling and is currently at a very low 4.3%.

In view of this situation, I have no doubt that the US central bank will continue to tighten its monetary policy. How it will be doing this (interest rate hikes, reduction of the government bond holdings, change in forward guidance (i.e. guidance of market expectations through statements made by the central bank)) I do not want to discuss at this point. Generally, the idea holds: “After the interest rate hike is before the (next) interest rate hike”.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.