It comes as a surprise that despite the crucial nature of the issue only a few reliable studies have been produced for this field of social medicine so far. To facilitate a better understanding of the subject, we have gone through relevant recent (2006 to 2019) papers in order for us to consolidate our assessment of the effects of pandemics, especially on global economic performance.

The specific studies analyse and compare the effects of epidemics (i.e. a significant regional increase of new infections in one region) to those of pandemics (cross-border and cross-continental spreading of an infectious disease) on the basis of:

- Historical case studies

- Macroeconomic models and simulation of shocks

- Simulations (e.g. actuarial models) of possible courses and effects of the disease

Most studies rely on historical case studies so as to calibrate the parameters of the respective models. Whereas macroeconomic models are primarily aimed at quantifying the effects of rapidly spreading infectious diseases, actuarial mathematics links the expected effects to probabilities. The idea is to forecast the probability of pandemics and their socio-economic costs.

What do the aforementioned studies suggest will happen?

The various studies and their models forecast relatively limited economic effects. On average, experts envisage a decline of global economic output (as measured by GDP) of 0.6% or USD 500bn. At the same time, the consensus expects a V-shaped recovery of the economy in the coming three to twelve months. That being said, significant regional differences are likely, especially in terms of the effects on the GDP of the first world vs. developing economies.

The most negative estimate of a study with regard to an assumed outbreak of Ebola in Sierra Leone suggested a slump in GDP of 16% in this economy. This was due to the, relatively to industrialised states, deficient healthcare, the generally worse supply situation within the population, and the high population density in conjunction with a lack of hygiene (e.g. insufficient access to clean drinking water).

In a 2013 model, the World Bank set the probability of a global pandemic at 1% to 3%. This is very low, but in the event of a high rate of infection (like for the Spanish flu), the costs for the global economy could amount to as much as USD 3,000bn.

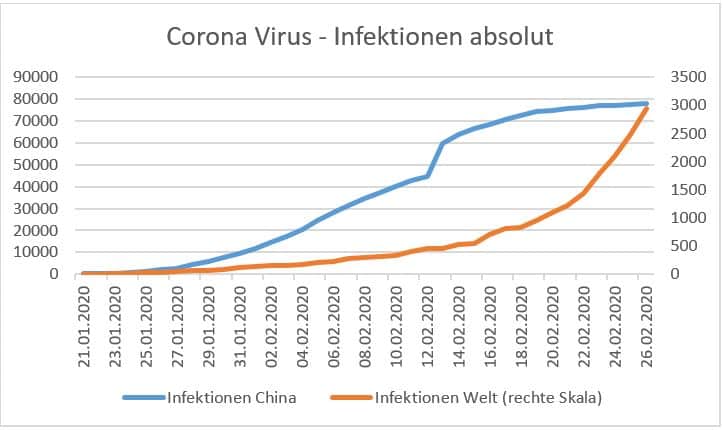

Coronavirus – Infections

Source: WHO, edited by Erste AM; Infections China (blue), Infections Worldwide (orange); 26.02.2020

The calculations of the world bank

In view of this volume, the World Bank warns that the community of states has set insufficient preventive measures. According to its model, USD 3.7bn would have to be invested annually in preventive measures (especially in developing countries) for the cost caused by infectious diseases to fall by USD 37bn.

Generally speaking, the economic cost is biggest in those sectors where personal client contact takes place and where consumption cannot be suspended. This includes numerous segments of the service sector, especially tourism and the leisure industry. Companies with complex and global supply chains that would be disrupted by the fight against a pandemic would also be particularly hard hit.

Costs of an epidemic/pandemic

In terms of countries, those economies would be worst affected that strongly depended on the input factor labour. This means that developing countries would feel the costs of an epidemic or pandemic more severely than developed countries, given that their economy is less significantly automatised and digitised.

The degree of interconnectedness of regions is another important influencing factor for the spreading of an infectious disease and costs associated with it.

For example, a virus will spread faster in open economies such as Europe than, say, in the Middle East, where the individual countries are more isolated from each other.

An important element with regard to the costs generated by pandemics is human behaviour. Fear of contagion can be both detrimental to containment and produce immediate negative economic effects. This starts at the sociology of a quarantine situation, which people will try to escape in order to avoid possible contagion and thus carry the virus with them.

The sociology of quarantine

The literature also suggests that many people resort to self-quarantine so as to avoid contracting a virus. This self-quarantine includes the avoidance of places that are associated with a heightened risk of contagion (e.g. events, restaurants, cinemas, travelling etc.), which has a negative effect on consumption.

As previous pandemics have shown, in particularly affected areas people also stay away from work so as to avoid infection. According to research, such forms of voluntarily taken protective measures account for about 60% of the knock-on costs of a pandemic.

By contrast, sick days at work make up only about 28% of total costs.

The framework has changed for the worse

Although the studies we analysed are relatively young, one can legitimately ask whether the assumptions made in the various models are still valid, or whether the framework has maybe changed drastically in recent years.

In other words: do the results of the studies apply to the spreading of coronavirus in 2020?

The most significant issue is the global increase in traffic over recent decades. This includes both the transportation of cargo and people travelling. Also, supply chains have become significantly more globalised in recent years. All of that has drastically increased the level of integration in the global economy.

After all, the economic environment is more challenging than many a previous pandemic. After several years of strong growth, economic growth is currently in a phase of slowdown. At the same time, the share of China and South East Asia in total global economic output has increased substantially in the recent ten years.

A pandemic can have a major impact on the global economy today

A pandemic, not the least one that originated in China, could therefore come with a stronger effect on the global economy in such an environment than previous pandemics. In addition, the central banks have little room to manoeuvre to thwart possible negative consequences effectively amid the current phase of low interest rates.

A study from 2006 for example makes the recommendation to the ECB to cut its key-lending rates by 100bps as first countermeasure.

Such a step would not be possible nowadays. Social media, having gained a strong foothold in our society in the recent ten years, are another important aspect. They can amplify the panic and thus further push up the costs of a pandemic. While the odd younger study does point out this effect, it has not entered the models yet.

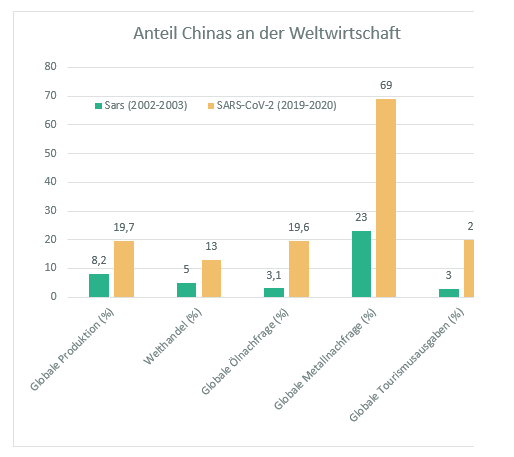

China’s share in the global economy

Source: IMF Global production; / Global trade / Global oil demand / Global metal demand / global tourism spending

Initial insights into the coronavirus do not suggest a severe course

While no final conclusions have been reached about the rampant coronavirus due to the early stages we are in, the progress so far allows for a few initial learning points. The transmission rate of the coronavirus seems to be equal to that of a cold or an aggressive form of influenza. Here, one infected person passes on the virus to two other people. In terms of the mortality rate, the Covid-19 virus ranks slightly higher than the common influenza virus, but clearly below the SARS virus. Also, the demographic groups of people above 70 and above 80 years old seem to be affected at disproportionately high rates by a severe course of the disease, whereas the age group of employable people (especially 20 to 60) shows a milder development of the disease.

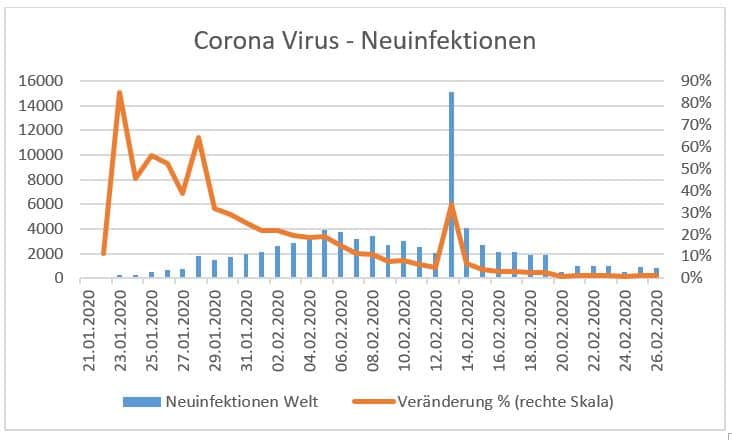

Coronavirus – new infections

Change in infections in %. The explosive dynamic is slowing down; new infections (blue); change in % (orange) (Source: WHO; edited by Erste AM)

The course of new infections in China also suggests that the time frame of the pandemic should roughly follow what we have seen in other pandemics (Spanish flu, swine flu, common flu etc.). In those cases, the pandemic reached its pinnacle about three months in.

In light of these facts and on the basis of various studies on this topic, current knowledge would suggest that, while the global spreading of the coronavirus will have an effect on the global economy, it will not be overly severe and should be levelled in about twelve month´s time.

Our dossier on coronavirus with analyses: https://blog.en.erste-am.com/dossier/coronavirus/

Sources:

- Win-Win? Assessing the global impact of the Chinese economy; Risto Herrala and Fabrice Orlandi BOFIT Discussion Papers; #4/2020

- The Economics of Pandemics and Quarantines; American Institute for Economic Research; Vincent Geloso; January, 2020

-

Epidemics and Economics; Author(s): International Monetary Fund. Communications Department; June 2018

-

Impact of a Hypothetical Infectious Disease Outbreak on US Exports and Export-Based Jobs; Bambery Z, Cassell CH, Bunnell RE, Roy K, Ahmed Z, Payne RL, Meltzer MI; 2018

- Ahmed, Shaghil, Ricardo Correa, Daniel A. Dias, Nils Gornemann, Jasper Hoek, Anil Jain, Edith Liu, and Anna Wong (2019). Global Spillovers of a China Hard Landing. International Finance Discussion Papers 1260. https://doi.org/10.17016/IFDP.2019.1260

- Future Global Shocks: Pandemics by H Rubin OECD; 2011; – www.oecd.org › gov › risk

- Global Macroeconomic Consequences of Pandemic Influenza; Alexandra A. Sidorenko and Warwick J. McKibbinWednesday, February, 2006

- Globalization and Disease: The Case of SARS; Jong-Wha Lee and Warwick J. McKibbin, May, 2003

- A Potential Influenza Pandemic: Possible Macroeconomic Effects and Policy Issues December 8, 2005; Congressional Budget Office; revised July 27, 2006

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

The Tariff Man

Last Sunday, the US government announced new tariffs on goods from Canada, Mexico and China, only to suspend them again shortly afterwards. How might the trade conflict develop? Is the EU also threatened with new tariffs?