Last Thursday, incriminating video and audio tapes emerged that linked current President Michel Temer to bribery. The accusations have thrown Brazil into a deep political crisis, and the capital markets have lost massively.

Temer followed the impeached President Dilma Roussef last August on an interim basis and was seen as a beacon of hope for change. Temer faced the press and categorically rejected the accusations. He clarified that he would not step down. Investors had put a lot of trust in the new government cabinet – trust that has now been dealt a severe blow.

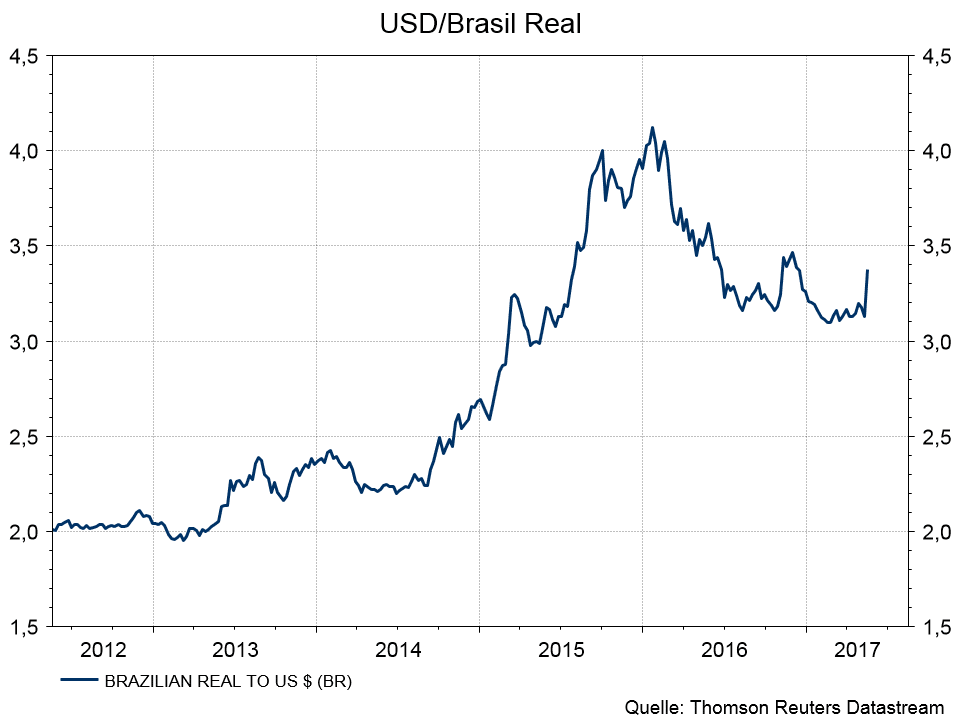

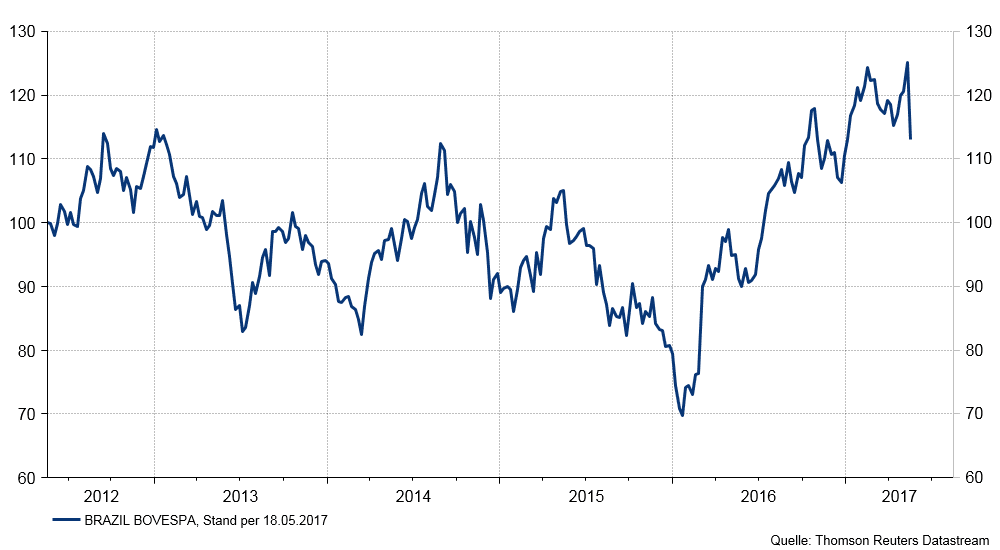

The response of the capital markets to the accusations of bribery was massive. The spreads of Brazilian government bonds widened by up to 80bps, the Brazilian real lost 7.2% relative to the USD, and the stock market shed almost 9%. Temer’s future is unclear. There are three possible alternatives: resignation, impeachment, or muddling through until the end of term in 2018.

FELIX DORNAUS: Senior Fund Manager Emerging Market Government Bonds

Felix Dornaus, Senior Fund Manager Emerging Markets Bonds

“The coming days will remain very volatile. From the current perspective, Temer’s resignation would be the option with the least amount of friction, whereas an impeachment would be the most time-consuming and therefore worst way to go as far as the markets are concerned. The parliamentary work regarding the most important reforms necessary for the economic recovery (pension and healthcare reform), whose preliminary votes had been going quite successfully in the various committees in previous weeks, has come to a halt or is at the very least badly impeded. The market is worried that a failure of the reforms to come through in time or at all would put budget consolidation at risk and possibly even trigger another rating downgrade.”

Brasilian Real to US-Dollar (- 5 years; as of 18.5.2017)

Quelle: Thomson Reuters Datastream; per 19.5.2017

“So far this event has been relatively isolated with little to no spill-over into other emerging stock exchanges. From my point of view this will not change, it is a purely Brazilian issue. In case of a sustainable economic deterioration of Brazil, Argentina, Brazil’s main trading partner, would be the first one to suffer. For the time being, my positioning remains neutral.”

PETER VARGA: Senior Fund Manager Emerging Markets Corporate Bonds

Péter Varga, Lead Manager Emerging Markets Corporates Erste Asset Management

“The news about the accusations of corruption against President Temer hit the markets like a bomb, given that Brazil used to be the market participants’ “darling” in view of the planned / and now possibly delayed – reforms.

Brazilian corporate bonds suffered almost as badly as government bonds. Interestingly, public or state-affiliated companies such as Petrobras, BNDES (Brazilian Development Bank) or Banco do Brasil lost more significantly than privately-held companies, which even benefited from the weak currency. The spreads had increased by about 15 to 60bps from the previous day, depending on maturity and issuer.

Overall, the weighting of our funds was neural, with the exposure in our ESG funds slightly lower. We engaged in minor reallocation during the correction and sold titles whose reaction to the events was insufficient from our point of view.

Generally speaking, we will continue to reduce our weighting in Brazilian corporate bonds if conditions are favourable. The planned reforms were essential for a possible turnaround of Brazil. If they were delayed, the country could embark yet again on a downward spiral. A weak economy would particularly affect sectors such as cement and steel, banks, and the meat industry, whereas export-oriented companies such as from the paper industry would be less severely affected.

I think the danger of contagion by other emerging economies is limited, at best via indirect effects on the basis of relative valuations.”

GABRIELA TINTI: Senior Fund Manager Global Emerging Markets Equities

Gabriela Tinti, Senior Fondsmanagerin

“Due to recent events we have reduced our weightings in Brazilian equities. Prior to the scandal, Brazil was among the best-performing stock exchanges worldwide. At the moment Brazil accounts for only 6.5% of our global emerging markets equity fund. In terms of valuation, the Brazilian stock exchange does not look bad. For example, the price-earnings ratio (PER) on the basis of expected company earnings 2017 is at a low 11.0x. By comparison, global emerging markets stock exchanges are traded at a PER of 15.0x, while developed markets trade at 21.0x.”

Brasilian Stock Exchange (BOVESPA-Index – 5 years; as of 19.5.2017)

Quelle: Thomson Reuters Datastream; per 19.5.2017

“We prefer export companies with a high share of sales in USD as well as titles with strong earnings power, high cash flow, and high dividend yields for our funds.

I regard the risk of contagion for other emerging stock markets as minimal. We have seen an impeachment and snap elections due to corruption in South Korea as well. Unfortunately, the issue of corruption is a recurrent theme especially in the emerging markets. But overall it might lead to a situation where the international investors become more cautious towards Brazil due to the high level of uncertainty.”

DOMINIK BENEDIKT: Senior ESG Analyst

Dominik Benedikt, Senior ESG-Analyst Erste Asset Management

“Particularly in emerging markets, the ESG (i.e. sustainable) company research yields additional benefits, given that governance risks are recognised earlier than by traditional methods of research. Ideally, they can be avoided altogether.

Brazilian companies are a very good example for this method, and we have had success in this field over the past years. For example, we excluded JBS, i.e. the biggest meat producer in the world and the institution that triggered the latest scandal around President Temer, from our sustainable funds at the beginning of 2016.

Our ESG analysis also indicated excessive corruption risks at Petrobras and Odebrecht in 2014. Both companies were central players in Brazil’s current crisis. Given that we were not invested, we managed to avoid a loss of 69% in the bonds of Odebrecht.

Of course it would be presumptuous to assume that we can predict every single one of those cases. But at the same time, these examples illustrate clearly how our sustainability research can improve the quality of the portfolio overall.”

Notice: Estimates are not a reliable indicator for future investmens.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

to the White House")

Best of Charts: The road (in)to the White House

Three weeks before election day, the race for the White House is wide open: While Kamala Harris is ahead in the nationwide polls, Donald Trump is currently likely to be ahead in the crucial “swing states”. In any case, the economic situation and mood in the USA are likely to play an important role in the race for the presidency.