This week marks the 20th anniversary of the “new economy” or “dot-com bubble” peak. On 10 March, 2000, the leading indices for technology stocks reached record highs one final time before collapsing in weeks that followed, revealing the extent of massive misjudgements and overvaluations among telecom, media and technology stocks (TMT).

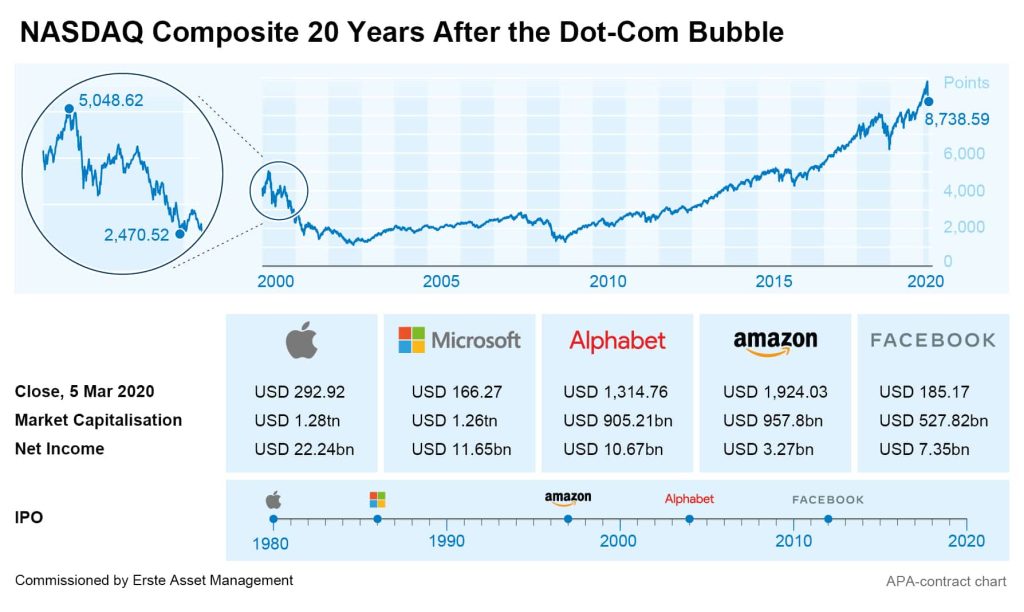

While the technology-oriented NASDAQ Composite Index of the New York Stock Exchange still stood at 5,048 points on 10 March, that value halved to 2,471 units by the end of 2000. In Frankfurt, the index for the “Neuer Markt” (NEMAX) segment dropped from 9,631 points to 2,869 points during the same period.

This market crash not only cost countless private investors their investments but also led to a massive industry reevaluation. Two decades hence, the promises of digital business seem to have been at least partially fulfilled.

Rise and temporary fall of an auspicious industry

Driven by high expectations of new technologies such as the Internet or the first mobile phone services and the innovative business models associated with them, the stock markets around the world were very much in a gold rush mood following the turn of the millennium. Long-term sales and profit expectations, particularly for young TMT companies, drew not only experienced and institutional investors, but increasingly small private investors to the stock exchanges.

A prominent example from Europe is the Deutsche Telekom, which was presented as a lucrative entry into the stock market for many Germans with several rounds of issues. Following an issue price of EUR 39.50 in mid-1999, the price of the heavily advertised “T-Share” reached its highest level of EUR 103.50 only a few days before the bubble burst in March 2000.

When a third wave of T-Shares was floated on the stock exchange only three months later, the issue price was still EUR 66.50, before the value dropped to below EUR 20 within a few months.

In view of the seemingly endless possibilities, “hard criteria” such as actual business figures were neglected in the share valuation. Clicks became a kind of new currency, and potential growth was pushed to the fore. Large parts of corporate spending went into marketing rather than infrastructure and development.

As the sector was heavily dependent on intangible assets such as IT expertise and computer programs, many valuations were not backed by physical assets. In addition, cases of accounting fraud and fraudulent activities in the shadow of the New Economy contributed to the development of the bubble.

The German media group EM.TV is a textbook example. The company had taken its business with TV marketing rights to the Frankfurt Stock Exchange and issued forecasts of massive increases in sales and profits before the summer.

In the last quarter of the year however, a profit warning finally put an end to the hype, leading to a drop in EM.TV’s share price as well as lawsuits from small investors and investigations into balance sheet irregularities and insider trading.

Fears grew throughout the New Economy industry that the high cost of investment in the necessary infrastructure might never pay off. The first bankruptcies of start-ups led to further valuation losses through equity investments – which were often financed by shares.

When this caused experienced investors to withdraw, prices fell even further, triggering the crash of the entire sector. In Austria, the Internet service provider YLine and online bookseller Lion.cc were at the centre of the turmoil in the market, which ultimately also dragged the stationery retailer Libro down with it.

Corrections and late winners in a badly shaken industry

While private investors missed the timely exit and lost their investments, the start-ups experienced a market correction that many did not survive. On the other hand, several companies that later became global players survived the bursting of the dot-com bubble pretty much unscathed and subsequently continued on their way to the top of the stock markets, unfazed.

While the Frankfurt Stock Exchange’s NEMAX index was discontinued in the early 2000s, the US’s NASDAQ Composite Index fought its way up to new record highs after the dot-com bubble burst from the 2,500-point mark to over 9,000 points.

Today, Apple, Microsoft, Google’s parent company Alphabet, the online retailer Amazon and Facebook dominate the list of the most valuable listed companies in the telecom, media and technology sectors and are considered – under conditions that were significantly influenced by the stock market crash 20 years ago –particularly sought-after stocks.

ERSTE STOCK TECHNO: Difficult start – rapid catch-up

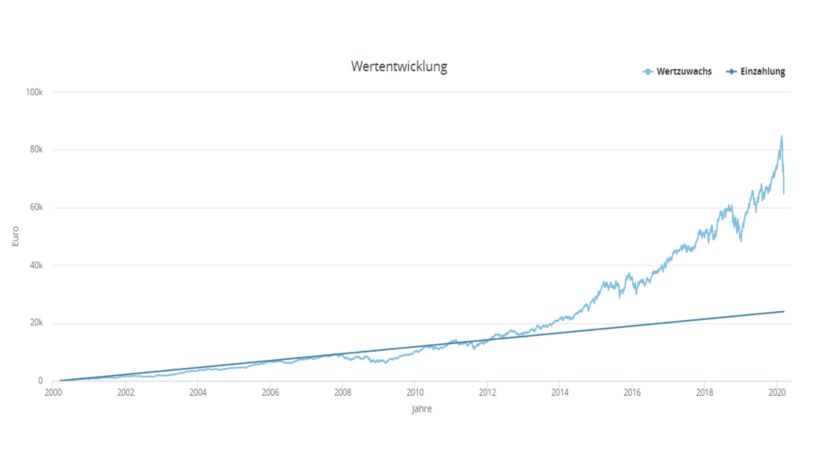

Tech-stocks such as Apple, Alphabet, Amazon, Facebook, Microsoft and others are also included in the ERSTE STOCK TECHNO fund, which was launched on 16.3.2000 and has been invested in the largest and most important companies in the technology sector from the outset.

Like many equities, it had to accept a loss in value at the beginning of the fund, but as the investment period increased, the companies and also the price gains returned. Those who started out with 0 Euro and regularly bought 100 Euro technology stocks can now enjoy a small fortune of more than 64,700 Euro.

This results in a proud increase in value of over 9 percent per year* (see “Performance Calculator”, https://www.erste-am.at/de/sfondsplan/rechner/performance-rechner). This figure takes into account all significant price slumps in the history of fund, such as the bursting of the dot.com bubble, the financial crisis of 2008 or the recent price setbacks due to the corona virus.

The same applies here as in earlier phases of correction: Price declines can be used to build up new positions. The outlook for the technology sector is still intact in the longer term.

Performance

*This result is based on a historical return in % p.a., excluding fees and processing costs. Past performance is not a reliable indicator of future performance of the fund.

Advantages for the investor

- Broad diversification in technology companies with little capital investment.

- Active stock selection based on fundamental criteria.

- Opportunities for attractive capital appreciation.

- The fund is suitable as an addition to an existing equity portfolio and is intended for long-term capital appreciation.

Risks to be considered

- The price of the funds can fluctuate greatly (high volatility).

- The investor mainly bears the risk of the commodity sector as well as the issuer risk of the participating companies.

- Due to the investment in foreign currencies the net asset value in Euro can fluctuate due to changes in the exchange rate.

- Loss of capital is possible.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Losses on the stock markets: an overview of the reasons and consequences

There was little to cheer about on the stock markets at the start of the week: there were significant price losses in both Europe and the USA and the Japanese Nikkei-225 recorded one of the biggest daily losses in its history. What were the reasons for Monday’s sharp sell-off, what impact could the latest events have on the markets and what will happen with the increasingly weak economy?