After the slump in 2020, the first year of the pandemic, and a difficult subsequent 2021 business year, the automotive industry is once more cautiously optimistic about the future. Initial outlooks from major corporations and industry associations suggest a recovery. Opportunities as well as challenges are arising from the current switch to electric vehicles (EVs). However, continuing computer chip supply bottlenecks could further slow the recovery in the midst of this transformation process.

The year 2021 was a mixed blessing for the industry. “While, particularly during the first half of the year, some significant growth was realised due to the low year-on-year comparison and recovery tendencies, as the picture became decidedly negative in the second half,” concluded the German Association of the Automotive Industry (VDA). According to the VDA, the global semiconductor shortage was the main factor holding the industry back. However, bottlenecks in other intermediate products and raw materials also contributed to car production lagging behind demand.

On balance, the important sales markets of China and the US were able to recover somewhat in 2021, according to the VDA; however, Europe showed a decline. The number of newly registered passenger cars in Europe was 11.8 million, around 2 per cent less than in the previous year. The German car market in particular suffered from the semiconductor crisis. According to data from the German Federal Motor Transport Authority, sales in Germany fell to 2.62 million new vehicles in 2021, the lowest level since the 1990 reunification.

Lukewarm Sales Figures with Positive Q1 Results

Among the European key players in the industry, sales reports were mixed. The BMW Group, which includes both Mini and Rolly-Royce, reported an 8.4 per cent increase in sales to 2.5 million vehicles in 2021. Meanwhile, Volkswagen and Mercedes-Benz continued to suffer from the chip crisis and supply chain problems: after the weak 2020 figures, VW saw a further drop in sales of 8.1 per cent to 4.9 million cars in 2021. Mercedes reported a 5 per cent decline in sales.

On the other hand, the reported earnings of some car manufacturers turned out to be a positive surprise: Mercedes-Benz reported an operating income (EBIT) of EUR 14bn for 2021, performing better than expected. The Group also benefited from spinning off its truck business into the now independent company Daimler Trucks. The French Renault Group returned to the black in 2021 with a profit of EUR 967m, after having posted a loss of EUR 8bn in 2020. Sweden’s Volvo Cars increased profits to SEK 20.3bn, up from 8.5 billion in 2020, the first year of the pandemic.

A number of Japanese automakers have also recently reported strong figures. Toyota reported a profit of JPY 2.32tr, or the equivalent of just over EUR 17bn, for the first three quarters of its fiscal year 2021/22, which runs through March – up 58 per cent from the same period last year. Nissan made a profit of JPY 201.3bn in the same period, following a loss of JPY 367.7bn YoY.

Industry Associations Expect Auto Market to Recover in 2022

In the current year, the recovery in the automotive market is expected to continue despite difficult conditions. The German industry association VDA expects sales on the global auto market to increase by around 4 per cent in 2022, a similar growth to 2021. For China and the US, the association estimates a growth of around 2 per cent. A significantly larger increase of 5 per cent is forecast for Europe. However, the European market suffered a bigger drop than other regions in 2021 due to the shortage of semiconductors, so the need to catch up is also greater, according to the VDA. The European industry association ACEA is somewhat more optimistic and expects a growth of 7.9 per cent to 10.5 million cars sold in Europe in 2022. However, this would still leave the market 20 per cent below 2019 pre-pandemic levels.

Semiconductor Shortage Continues to Slow Production

The recovery continues to be held back by the semiconductor supply shortage. According to industry representatives, the situation is easing, but the shortage is not over. Supply of chips is improving, “but even in 2022 we will not be able to manufacture all the cars we could sell,” said VW CEO Herbert Diess at a recent works meeting, announcing possible capacity adjustments.

Against this background, Mercedes has imposed an order freeze in Germany for the current E-Class sedan model. Due to increasing order numbers, the production volume has been exhausted, a company spokesman said. According to the papers Stuttgarter Zeitung and Stuttgarter Nachrichten, the order freeze is also related to the computer chip supply bottleneck.

The EU now wants to bolster the European semiconductor industry, and thus also the companies in the electronics and automotive sectors that depend on computer chips, with its “European Chips Act” initiative. The aim is to double the EU’s market share of global production to one-fifth by 2030. In addition to the already planned investment of EUR 30bn by 2030, a further EUR 15bn is now to be raised.

EV Transition is in Full Swing

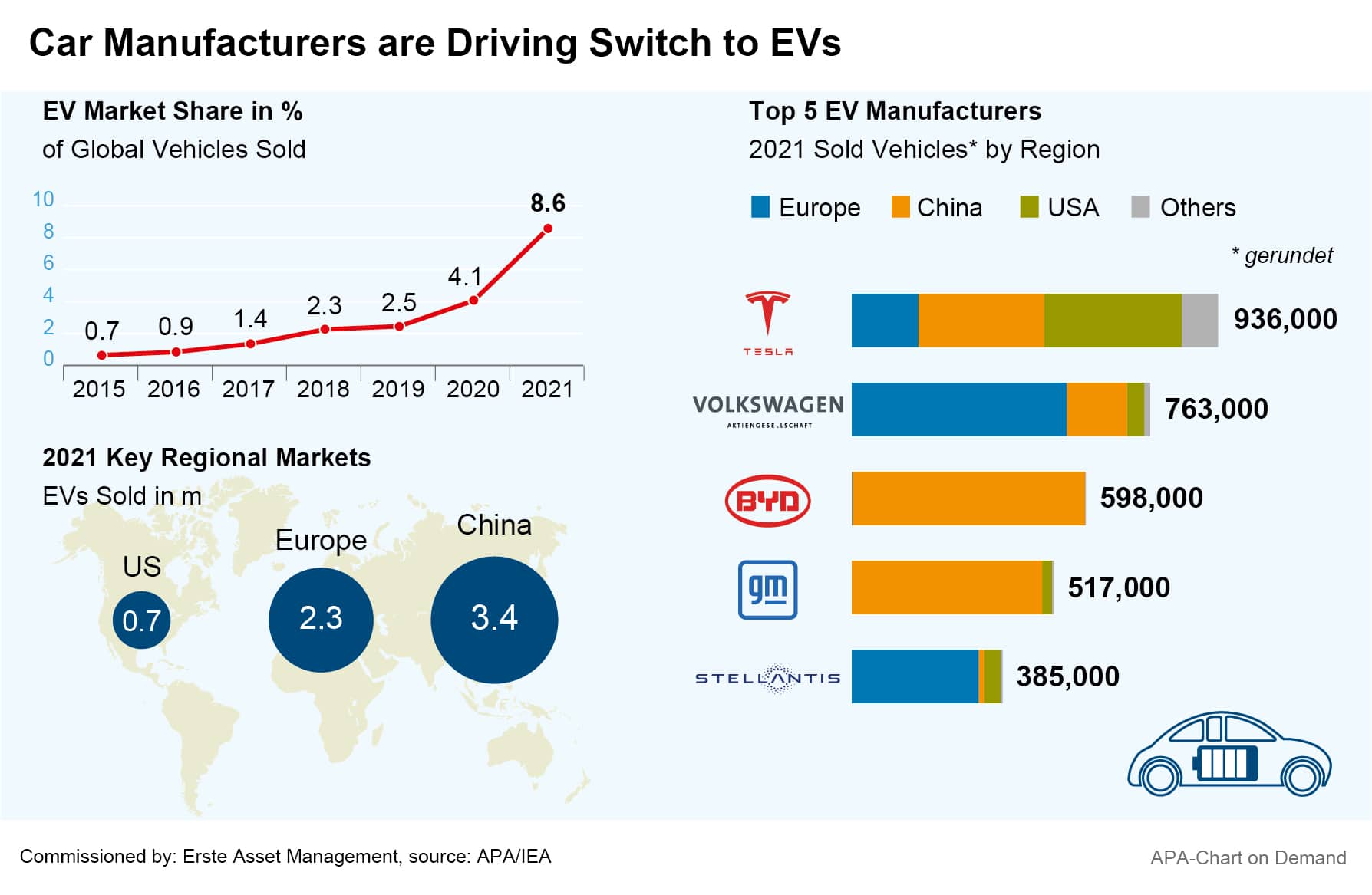

The trend toward electric cars is expected to continue in 2022. According to an analysis by the International Energy Agency (IEA), sales of electric cars more than doubled in 2021, with 6.6 million vehicles sold. Even in the crisis year of 2020, EV sales increased. According to the IEA, China accounts for more than half of all EVs sold, but there is also strong growth in Europe and the United States.

The switch is also being driven by many countries’ climate targets. The UK government wants to ban new cars with combustion engines starting 2030. In Italy, combustion engines in passenger cars will be phased out by 2035, and the Italian government is already planning an extensive aid package to support the country’s key industry in making the transition. Furthermore, government subsidies for EVs in many countries are also an important factor in the transformation process.

The major automotive companies are pushing ahead with the transition. After the sector was long dominated by the US Tesla group, other major car manufacturers are now also driving the change with billions worth of investments. Swedish car manufacturer Volvo plans to invest almost EUR 1bn into converting its production facility in Gothenburg to EV manufacturing. VW has already converted its factory in Zwickau to build EVs. At its headquarters in Wolfsburg, VW also plans to build a completely new factory for its planned Trinity EV brand. In the important sales market of China, too, the company is continuing to invest heavily in e-mobility. VW subsidiary Audi was recently greenlighted by China’s authorities to co-build an electric car factory with Chinese partner FAW to the tune of USD 3bn.

Investments are also being made to drive EV battery technology. Mercedes is investing in Taiwanese battery manufacturer Prologium to jointly develop vehicle batteries. Volvo plans to build a battery factory together with battery manufacturer Northvolt, expected to be in operation by 2025. VW has already announced battery development collaboration plans with Bosch.

Governments must now continue to support the trend toward e-mobility with the necessary infrastructure investments. The German industry association VDA is calling on the new German government to accelerate the installment of charging points for EVs, criticising that the expansion of charging infrastructure is currently not keeping pace with the booming e-mobility. This picture is similar across most of Europe. According to ACEA data, the number of electric and hybrid cars in the EU has increased tenfold since 2017, but the number of charging stations required for them has only slightly more than doubled.

Corporations are Focusing on Autonomous Driving

The development of autonomous driving cars is also continuing rapidly. Following in the footsteps of Google and Tesla, many European companies are now also developing such systems and acquiring expertise through partnerships and takeovers. VW has hired around 1,000 software engineers in 2021 and is strengthening its software subsidiary Cariad through acquisitions. In addition, the partnership with Bosch is intended to accelerate the development of automated driving. VW CEO Diess expects that in 25 years, virtually all cars will be able to drive autonomously. Early functionality such as automatic distance-keeping are to be introduced in models of all VW brands in 2023. VW subsidiary Audi then plans to launch a fully autonomous EV in 2025 to compete with Tesla.

Mercedes wants to enable highly automated driving in standard S-Class sedans this year still, allowing drivers to let the vehicle drive completely autonomously in situations such as traffic jams on the highway. To this end, the carmaker is cooperating with, and has also invested in, the US company Luminar, which specializes in laser radar technology.

Investing in electromobility and hydrogen technology

Those who want to invest specifically in shares that cover the topic of alternative drive systems/electromobility more broadly will find a good opportunity in the ERSTE WWF STOCK ENVIRONMENT fund: With Nio, a pioneer in the premium market for smart electric vehicles, and the electric scooter provider Niu, the fund currently holds shares in two direct manufacturers. In addition, the fund management around Clemens Klein also focuses on other aspects such as charging infrastructure (Fasted, Alfen, Chargepoint), batteries (Ecopro, Freyer) or mechanical engineering companies in the fields of electric motors and batteries (Aumann, Manz).

In the ERSTE WWF STOCK ENVIRONMENT, hydrogen/fuel cell companies are also a major theme: with shares such as Plug Power, Ceres, Ballard Power, NEL or Hexagon Purus: the latter has just landed a major order from a Toyota subsidiary with its high-pressure cylinders for hydrogen applications and complete battery systems for medium and heavy-duty trucks.

Shares in the environmental technology sector are sometimes subject to high fluctuations, as recent developments have shown. The long-term growth opportunities are mainly provided by the transition to a climate-neutral economy. The EU wants to do away with greenhouse gas emissions as far as possible by 2050 at the latest and become CO2 neutral overall. There is no way around these technologies.

CONCLUSION: The carmakers are still suffering from the shortage of semiconductors, but after the difficult years of 2020 and 2021, there is light at the end of the tunnel. The European car manufacturers recently presented figures that were better than expected. The switch to electromobility is now in full swing.

The fund employs an active investment policy and is not oriented towards a benchmark. The assets are selected on a discretionary basis and the scope of discretion of the management company is not limited.

For further information on the sustainable focus of ERSTE WWF STOCK ENVIRONMENT as well as on the disclosures in accordance with the Disclosure Regulation (Regulation (EU) 2019/2088) and the Taxonomy Regulation (Regulation (EU) 2020/852), please refer to the current Prospectus. In deciding to invest in ERSTE WWF STOCK ENVIRONMENT, consideration should be given to any characteristics or objectives of the ERSTE WWF STOCK ENVIRONMENT as described in the Fund Documents.

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

DeepSeek: the Sputnik moment for AI?

A new AI model is making headlines and causing US tech giants to falter. Developed by a Chinese start-up, DeepSeek is now forcing us to fundamentally question some of the assumptions made during the AI boom. Find out what this could mean for the tech and chip industry in the article 👉

What effects could DeepSeek have on the technology sector?

The new AI model from Chinese start-up DeepSeek caused a stir on the stock market a fortnight ago. The seemingly much more efficient and therefore cheaper model caused the share prices of many a tech heavyweight to plummet. Although the initial market reactions were probably exaggerated, one question remains: what long-term impact will DeepSeek have on the big tech companies?