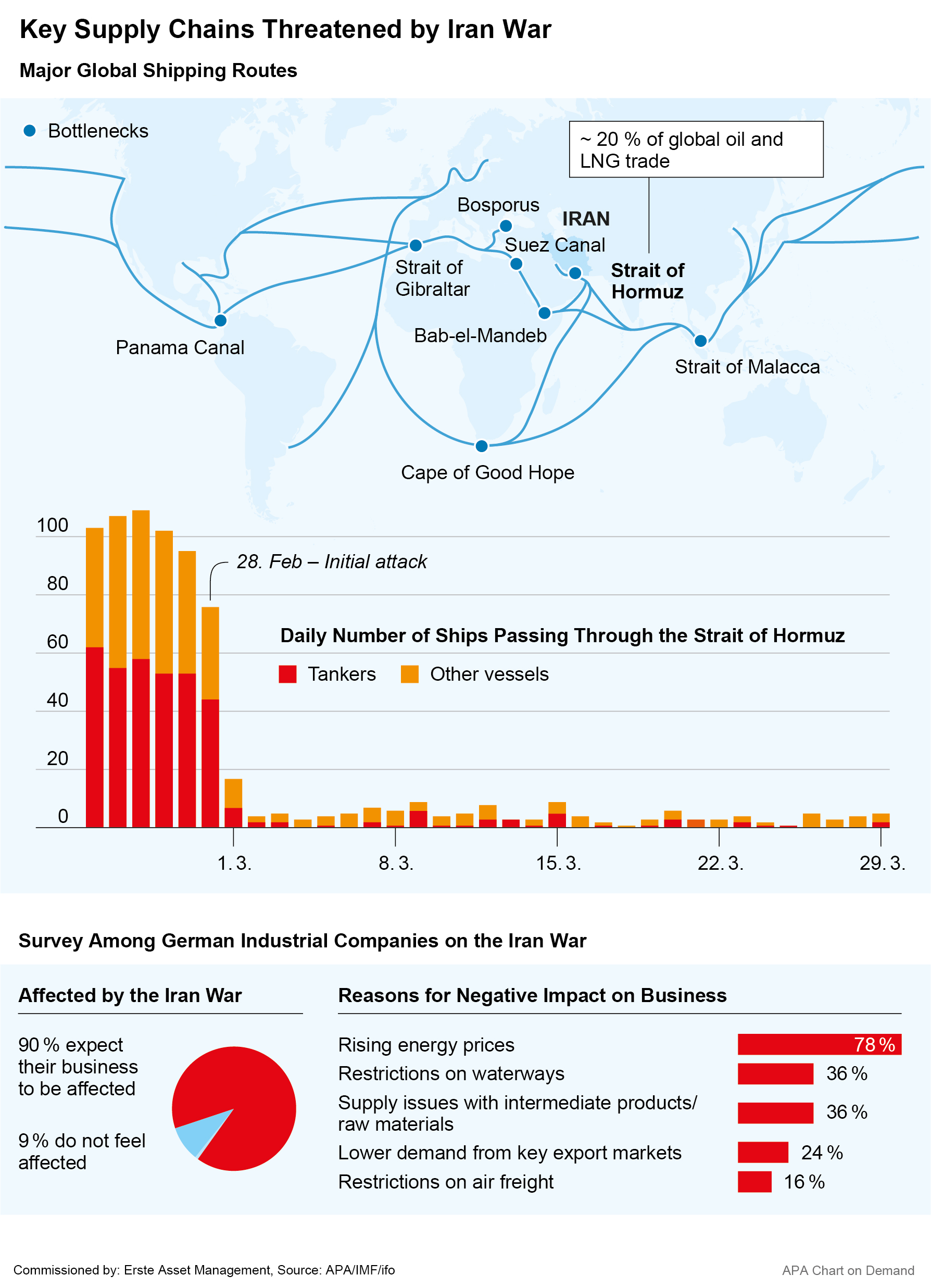

The economic consequences of the Iran War are difficult to predict but will most likely affect almost all regions and sectors. In addition to the sharp rise in energy prices resulting from the war, key supply chains are being disrupted. It is still unclear how trade through the Strait of Hormuz will resume following the agreement on a two-week ceasefire. With negotiations having made little progress so far, the US announced over the weekend that it would impose a naval blockade of the strait.

Nine out of ten industrial companies in Germany see their business negatively impacted by the Iran war, according to a recent survey by the German ifo Institute. Asked for the reason, 78 per cent of companies cited rising energy prices, 36 per cent per cent named restrictions on shipping routes, and 36 per cent named supply difficulties with intermediate goods and raw materials.

In a recent blog post, the International Monetary Fund (IMF) described the conflict as a “global but asymmetric shock” that is having an impact primarily through three channels: energy prices, trade and financial conditions. The disruption to energy supplies is particularly serious. “The war is also altering supply chains for everyday goods and critical inputs,” emphasised the IMF. The rerouting of tankers and container ships is increasing freight and insurance costs and extending delivery times. Flight cancellations at key hubs in the Gulf are affecting global tourism and complicating trade.

Data as of 31. March 2026

Chemical industry is affected twofold by the conflict

Some sectors, such as the chemical industry, are currently suffering particularly severely from the conflict. The recent rises in oil and gas prices are hitting the chemical industry twofold, as oil is not only an energy source for the sector but also a key raw material for the manufacture of countless products. In addition, the disruption to key supply chains is leading to shortages of other raw materials as well.

In mid-March, the German chemical industry reported signs of serious supply chain disruptions. “Our companies are reporting signs of initial extreme bottlenecks and the breakdown of supply chains,” explained Wolfgang Große Entrup, Chief Executive of the German chemical industry association VCI. Many essential chemical raw materials, such as aluminium, helium and sulphur, can no longer be transported via the Strait of Hormuz.

Fertiliser shortages raise fears of exploding food prices

Ammonia exports intended for fertiliser production are affected particularly severely. According to Große Entrup, 20 per cent of global ammonia trade is shipped from the Middle East via the Strait of Hormuz. Ammonia is by far the most important raw material for fertiliser production, particularly for the important urea fertilisers.

Furthermore, fertiliser production is extremely energy-intensive and relies on natural gas. A large share of global production therefore takes place in the Middle East, and the attacks on energy facilities in the Gulf region have brought not only oil and gas production but also fertiliser production largely to a standstill there. However, fertiliser production is also suffering in many other regions. In India, several plants have been forced to scale back production. Bangladesh has closed four of its five fertiliser factories.

As a result, agricultural and food sectors are being affected – in the middle of the crucial northern hemisphere’s sowing season. In Canada and the US, fertilisers are already in short supply, with the US having to import half of its urea fertiliser from abroad in several recent years. According to the industry association The Fertilizer Institute, US farmers are now short of roughly 25 per cent of their usual fertiliser stock for spring sowing. Prices for available supplies jumped up by more than one-third since the start of the war. Farmers who have not yet purchased their fertilisers are faced with empty warehouses in many places or prices that are unaffordable for some. Brazil, too, which imports almost all of its urea fertiliser, sources just under half of its required amount via the Strait of Hormuz.

The fertiliser shortage, combined with higher production and transport costs due to the rising energy prices, could consequently lead to exploding food prices in the near future. High oil and gas prices are not only affecting transport; many cooling and production processes, such as drying or baking, also rely on natural gas. Ultimately, high energy prices could also tempt many agricultural producers into processing part of their harvest into fuel, which in turn would reduce the food supply.

Staple foods such as bread or butter could be particularly affected by the price increases, Wifo agricultural economist Franz Sinabell emphasised in an interview with APA. Michael Grömling, a researcher at the German Economic Institute (IW), supports this possibility: “The current Middle East crisis is likely to further exacerbate the overall raw materials problem and thus domestic production costs.” However, it is currently difficult to estimate when and to what extent food prices for consumers will be affected.

Shipping and logistics companies are suffering from blockade and energy prices

Logistics and shipping companies are naturally also being significantly affected by the war in Iran and the Hormuz blockade. Because the Strait of Hormuz is currently not safe to navigate, around six ships owned by the German container shipping company Hapag-Lloyd, with 150 crew members on board, are stuck in the Persian Gulf, said Hapag-Lloyd CEO Rolf Habben Jansen at a press conference last week. According to Habben Jansen, the Iran conflict is costing the shipping company an additional USD 40m 50m per week, primarily due to more expensive fuel and longer routes as well as higher insurance premiums and demurrage charges.

Please note: the companies mentioned in this article have been selected as examples and do not constitute investment recommendations.

German logistics associations also voiced deep concern, calling for government support. High oil and gas prices are putting pressure on the entire logistics chain. Transport companies, parcel services, moving companies, logistics providers and shippers are currently facing the challenge of managing the rising energy costs whilst keeping supply chains stable, the associations explained.

Germany’s largest seaport, Hamburg, is, however, indirectly benefiting from the rerouting of merchant shipping around the Red Sea. As reported by Hamburger Hafen und Logistik AG (HHLA), operator of three container terminals in Hamburg, significantly higher cargo volumes were recorded in 2025 in trade with deep-sea ports in the UK, Belgium, Spain and the Netherlands.

High kerosene prices could drive up airfares

The aviation sector is being hit hard by rising kerosene prices. According to the International Air Transport Association (IATA), the war in the Middle East will drive up airfares. “There will be no winners here,” IATA Director general Willie Walsh told the Reuters news agency. Global demand is currently still robust, but higher ticket prices could act as a damper.

Should the conflict persist and lead to kerosene shortages, airlines might also reduce their capacity. The US airline United Airlines has already scaled back its flight schedule in response to the rising fuel prices: around five per cent of this year’s planned capacity will be temporarily suspended, CEO Scott Kirby announced. As a result of the higher ticket prices, the tourism industry is also fearing a loss of business.

European airlines could benefit from the air traffic disruptions in the Middle East

There is a silver lining: Europe’s airline industry could also benefit from the disruptions in air traffic in the Middle East, explained Lufthansa CEO Carsten Spohr recently. The hubs of airlines such as Emirates, Qatar, Etihad and Gulf Air, serving as transit points for thousands of tourists travelling from Europe to destinations in Asia, Australia and Africa every day, came to a standstill virtually overnight.

Luxury car manufacturers have also been hit hard by the decline in business in the Middle East, as trade in the region has virtually ground to a halt due to the conflict. While most luxury car manufacturers sell less than ten per cent of their vehicles in the Arab world, their share of profits is significantly higher due to bespoke modifications, which can double or triple the price of these already very expensive vehicles. Car buyers from the Arabian Peninsula are known for their costly and extravagant special requests, and Bentley CEO Frank-Steffen Walliser recently described the Middle East as “the best market in the world”.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Europe’s Economy Faces Major Challenges After Parliament Elections

The European People’s Party (EPP) remained the strongest group in the EU Parliament in last Sunday’s EU elections. Right-wing populist parties made significant gains in many of the 27 EU member states. What impact will the election result have?

Will the gold rally continue?

The price of gold has recently climbed from one high to the next. The rally seems almost puzzling due to a number of negative factors in the first half of the year. However, two reasons in particular provided plenty of tailwind. Can the rally go even further?