Every year at the beginning of May, investors are faced with the question of whether they should leave the stock exchanges and take the profits generated up to that point, and return at a later date in autumn. But is the old stock market adage “Sell in May” still valid? Peter Szopo, Head of Equity Fund Management with Erste Asset Management, does not believe in an imminent end of the bull market, let alone a stock market crash.

How do you explain your general optimism about stock markets?

Risky asset classes – such as equities – are being supported by the good global economic environment and monetary and fiscal policy. The International Monetary Fund (IMF) has recently confirmed its optimistic forecast for global economic growth. For 2018 and 2019, the organisation expects global growth of 3.9%, which matches the January figure. While the phase of growth acceleration is over, there are many signals suggesting that we will continue to experience clearly positive growth for a good number of quarters to come. We would want to be cautious if the USA were sliding into a recession, but nothing of that sort can be seen at this point. According to an indicator by the New York Fed, the probability of a recession in the coming twelve months is only about 10%.

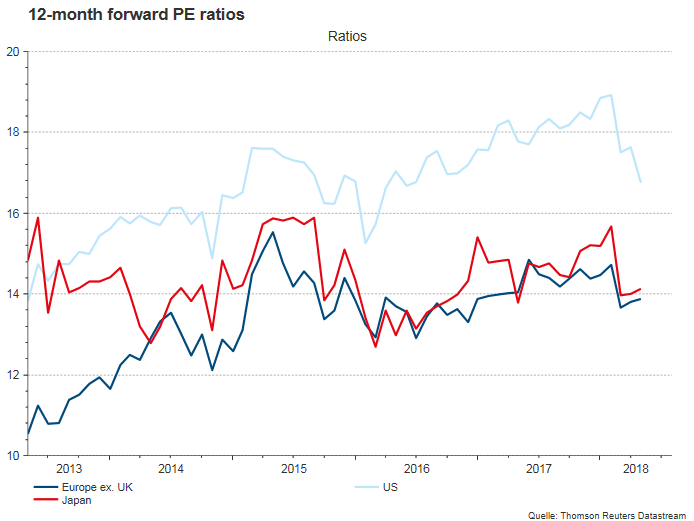

After a bull market of ten years, are equity valuations not quite ambitious at this stage? Do company earnings justify the valuations?

Erste Asset Management equity expert Peter Szopo: “Global company earnings are expected growing at roughly 15% this year”

Based on forward earnings, the markets are not excessively expensive – not even US equities. In the USA, the forecasts have even been revised upwards in the wake of the tax reform, and the current reporting season continues to produce positive surprises. In Europe, the current reporting season paints a mixed, but certainly not a negative picture: positive and negative surprises are roughly in balance. According to the current analyst consensus, company earnings in the United States should increase by about 20% this year. Emerging markets are also expected to post double-digit growth, while in Europe and Japan earnings growth is anticipated to come in at 8%. This translates into a global growth rate for company earnings of 15%, which constitutes a solid support for the markets.

Now, we do know that stock exchanges are often driven by abrupt changes in investor sentiment, which is reflected in volatile share prices. What are the threats that you see?

A possible risk that could thwart another recovery of the equity markets is an acceleration of inflation and a related overreaction of monetary policy. Will we see that? Not necessarily! Recent indicators suggest a very gradual acceleration of inflation. Rising interest rates against the backdrop of a robust economic environment do not have to stall the bull market, as the rate hikes by the US central bank since 2015 have shown. Central banks are aware of the importance of a cautious adjustment.

Another risk for the equity markets is the escalation of the trade conflict and geopolitical perils – do you agree?

The IMF regards the trade conflict between the USA and China as risk factor. Therefore, numerous players are making efforts to dissuade the two opposing parties from introducing new trade barriers. But it is true: if the sabre-rattling that we currently see were to end up in an escalation, both the global economy and the equity markets would suffer.

No risk of a crash then, which some doomsayers seem to see closing in?

We can, of course, identify risks that have been building and that endanger the run we have had on the bull market. But it is practically impossible to predict a crash. I do not know anybody who would have achieved that feat systematically. Many of those who try are constantly talking about a crash. And if it does hit, they would say: “See – I told you!” That is unsound practice and really does not help the investment community in is day-to-day business.

What stance do you recommend an equity investor take in the current situation?

Actually I am not allowed to issue specific investment recommendations, at least not as part of an interview like this one. But there are a number of principles that still apply, and by that I do not mean “sell in May”. After all, equities are still attractive and should not be absent in any well-diversified portfolio. That said, it is also not advisable to allocate one’s entire disposable financial capital to equities.

The overall situation has not changed in such a way since last December as to warrant a complete re-alignment of one’s investment strategy. Whether retail investors should reduce their equity ratios now depends on their risk appetite. It is not possible to systematically, i.e. repeatedly, time the market correctly anyway. A strategy that I like is to invest into a broadly-diversified equity portfolio over long periods of time. For example, via the s Fonds Plan, which also makes it possible for the investor to benefit from the cost-averaging effect (i.e. the principle of the lower average price). Depending on the performance of the investment fund, the performance of an s Fund Plan will differ from that of a one-off investment (higher or lower). A loss of capital is possible in both cases. It is also advisable to only invest in themes that one understands and to refrain from chasing after fads.

Note: Depending on the performance of the investment fund, the performance of an s Fonds Plan will differ from that of a single investment (higher or lower). A loss of capital is possible in both cases.

Author:

Dieter Kerschbaum, Communications Specialist Austria

Legal note:

Prognoses are no reliable indicator for future performance.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Investment View | February 2025

What’s happening on the markets? In our Investment View, the experts of our Investment Division regularly provide insights of current market events and their opinion on the various asset classes.