Private Credit explained simply

Alongside private equity and private infrastructure, private credit is one of the largest and most popular asset classes among investors in the private markets and is considered an alternative form of corporate financing. The granting of private credit—that is, loans issued outside the banking system—increased sharply in the years following the global financial crisis, not least because banks in many countries were subject to strict regulatory regimes, capital requirements, and liquidity regulations. In areas where banks withdrew from lending, private credit funds stepped in. These are investment products financed by private and institutional investors.

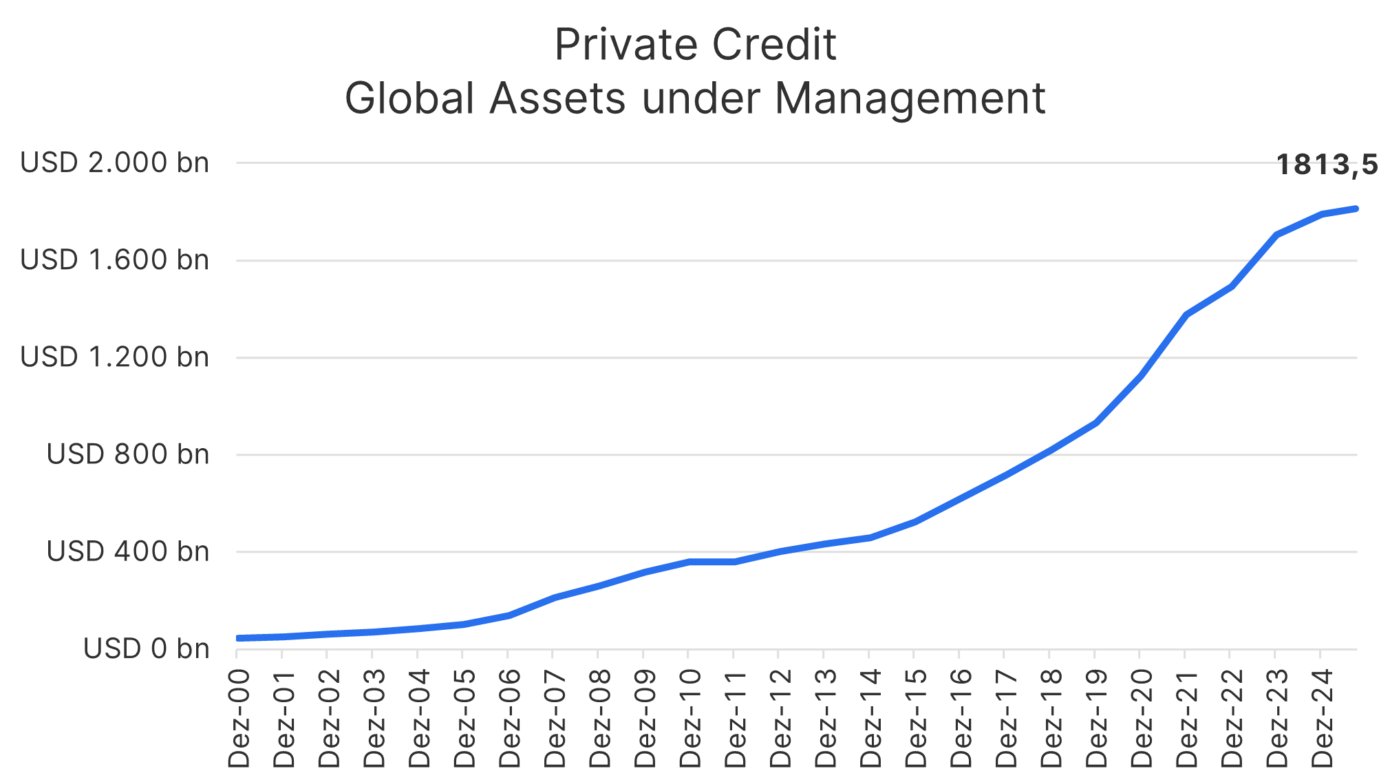

Global assets under management in the private credit sector have nearly tripled in the last 10 years alone.

Note: Please note that investing in securities involves risks as well as opportunities. Past performance is not a reliable indicator of future results.

Why do companies use private credit?

Companies seeking loans can access capital more directly, efficiently, and flexibly through private credit and increasingly view private credit providers as long-term and trustworthy financing partners. Private lenders can make faster investment decisions, operate without red tape, and offer customized repayment models. Companies particularly benefit from the flexibility in loan structuring and repayment terms.

However, financing is contingent upon a thorough review of the company—the so-called due diligence process. In many cases, contractual covenants are also agreed upon for the entire term of the loan, designed to ensure the company’s long-term success and a sound capital base. To this end, regular reports must be submitted to provide insights into the company’s performance.

Private loans are used to implement operational growth projects, for expansion, to enter new markets, for product development, for investments, or even for day-to-day operations.

An alternative to public bonds or syndicated bank loans

Private credit investments are, on the one hand, less liquid than investments in syndicated bank loans or high-yield corporate bonds. On the other hand, they feature variable interest rates and higher returns.

Stable returns

Private credit has the potential to deliver stable and ongoing cash flows (interest payments) during the investment period, whereas with private equity, for example, returns are often realized at the end of the term (sale of the company or “exit”). The establishment of covenants helps protect capital.

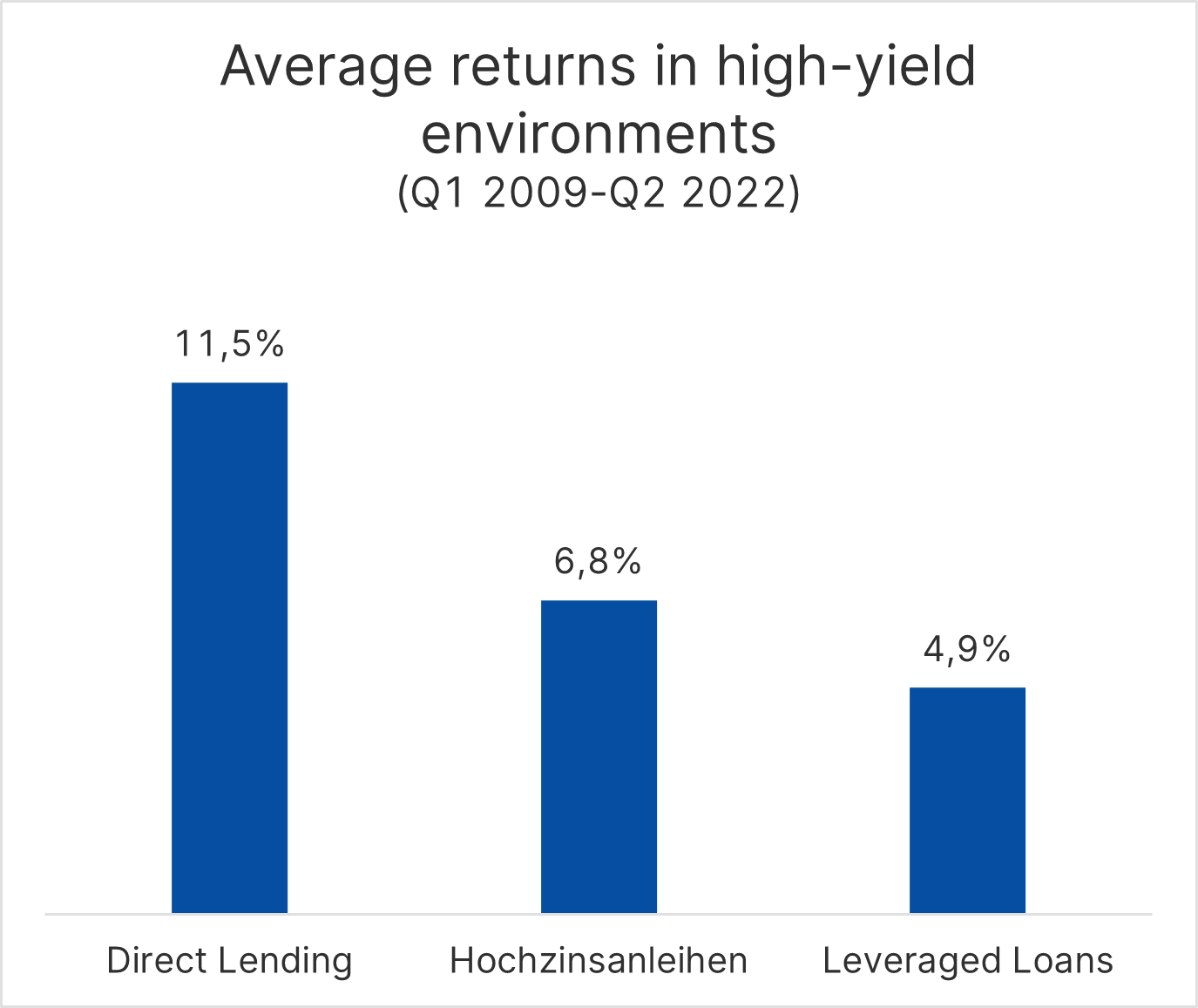

The excess returns of private credit compared to traditional debt investments are particularly evident in a rising interest rate environment. The chart below compares average returns in high-yield environments (quarters in which benchmark interest rates rose by more than 75 basis points) between the first quarter of 2009 and the second quarter of 2022.

Note: Investments in private credit may also result in a loss of principal. Past performance is not a reliable indicator of future results.

Inflation protection

Private credit financing typically features variable interest rates, and the amount of interest payments is regularly adjusted to a benchmark interest rate. Unlike fixed-income bonds, rising benchmark interest rates therefore do not lead to price losses but instead increase current income, which consequently carries lower to no interest rate risk. This allows investors to participate in rising interest rates and reduce the portfolio’s sensitivity to inflationary dynamics, which often lead to higher interest rates.

Low correlation with other asset classes

Returns from private credit often exhibit low correlation with those from traditional asset classes. Adding private credit to a portfolio can help diversify risk and stabilize the overall portfolio’s returns. This has been particularly evident in the past during turbulent market phases.

Private Credit – A Look Under the Hood

Private credit today takes many forms, differing in terms of seniority, collateralization, maturity, and risk profile.

Note: Please note that investing in securities involves risks as well as opportunities.

Senior Debt

A direct corporate loan, like bank loans, is considered a senior debt obligation and is negotiated with flexible terms. This form of credit is typically secured by the borrower’s cash flows and assets.

Subordinated Financing (Junior Debt)

Junior debt refers to subordinated debt. In many cases, it is not secured or only partially secured. Junior debt is repaid to creditors only after senior debt. For this reason, lenders demand higher interest rates to be appropriately compensated for the higher credit risk.

Unitranche

In unitranche financing, various private loans from multiple lenders are bundled into a single product. Instead of negotiating with several banks or financiers, there is only one lender or a small consortium. Since the lender pools more risk into a single product and assumes multiple seniority levels simultaneously, they receive a higher interest rate than in traditional senior debt financing. This is often referred to as “stretched senior” financing, as these liabilities typically result in a higher debt-to-equity ratio (leverage). Typical scenarios include corporate acquisitions or larger, more complex financing transactions.

Mezzanine Financing

Mezzanine financing is a form of financing that combines equity and debt capital. For example, companies receive subordinated loans, which in many cases have equity-like characteristics due to their subordinated status. This capital improves the company’s creditworthiness and, at the same time, its balance sheet ratios (such as the proportion of debt to total capital).

Convertible Notes

Convertible notes are loans that are converted into company shares—i.e., equity—at a pre-agreed (often more favorable) value during a subsequent equity financing round. As a result, the lender acquires shares in the company at a discount because they assumed the financing risk earlier than the new shareholders.

A convertible loan can be arranged much more quickly than a traditional equity round. Particularly in the case of startups or other rapidly growing companies, a final valuation has not yet been determined at the time the convertible loan is issued. This is deferred until the time of the equity round. The time until then is effectively used to increase the company’s valuation through further growth, increased revenue, or the expansion of the business model. Convertible loans and Simple Agreements for Future Equity (SAFEs) are widely used in the venture capital sector.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

China’s roadmap for the future: A look at the new five-year plan

Although China’s economy is expected to grow less strongly in the coming years, Beijing is focusing on quality and therefore growth in promising sectors. Read today’s blog post to find out why innovation, technology and key strategic industries are the focus of the new five-year plan and what opportunities this presents for investors.