The gold rally has stalled in recent weeks and the price has plummeted from over USD 5,260 per ounce to USD 4,100. Although there has been a recovery since then – gold is currently trading at around $4,750 (as of 10 April 2026). Nevertheless, since the start of the Iran war, the price has fallen by about 12% (in USD terms).

Many investors have been asking themselves: why is the price falling when gold is widely regarded as the ultimate safe haven for investors? An even more critical question arises: is this sharp correction set to last, or could the rally resume after a brief pause?

Gold weak despite geopolitical tensions

It is clear that the crisis in the Middle East has done nothing to help the price of gold. On the contrary: although gold usually shines due to its defensive characteristics in times of geopolitical tension, the price of gold came under pressure as the conflict began.

The reasons for the setback:

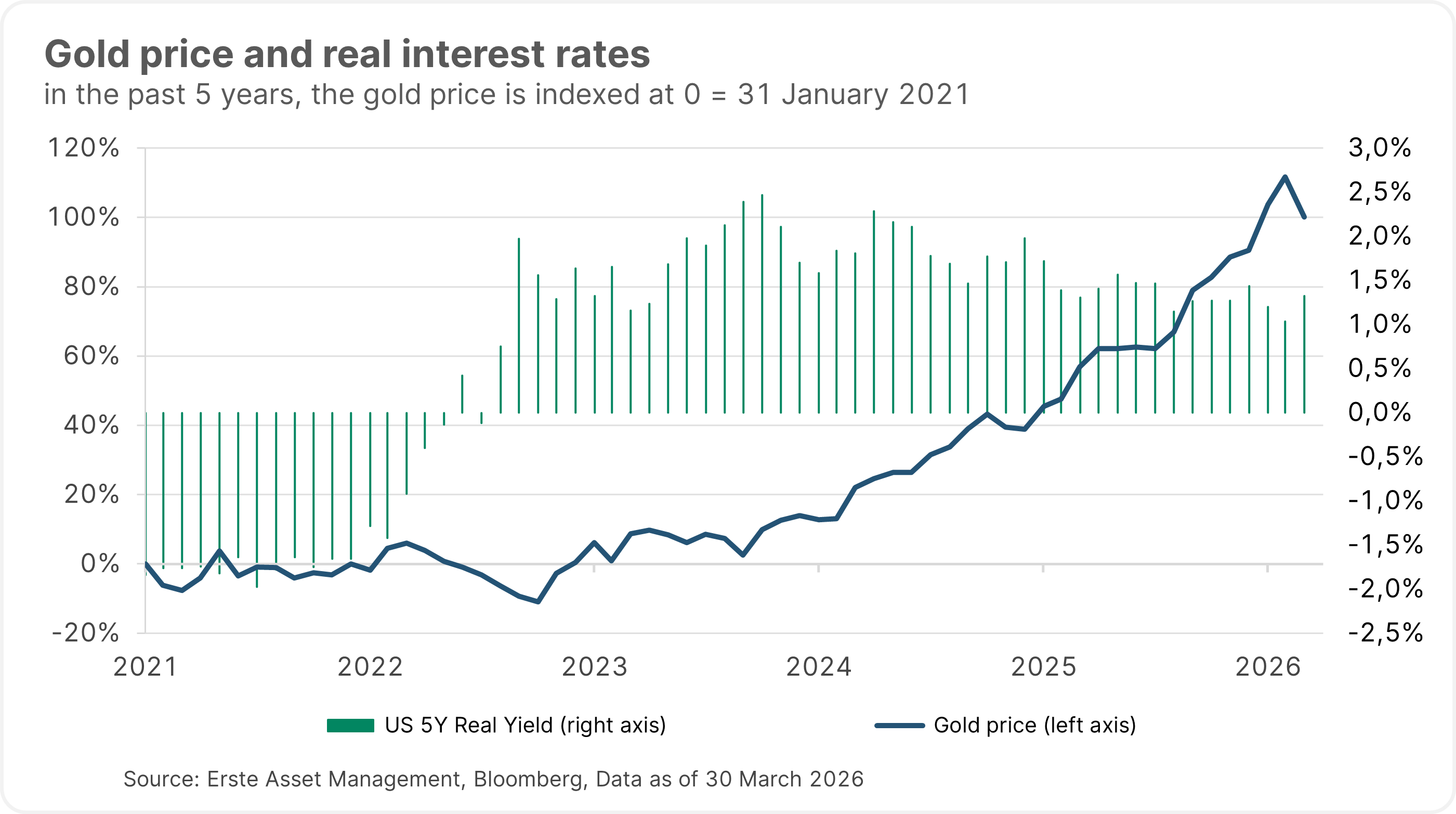

- As the most significant factor driving the price of gold, real interest rates / yields are providing considerable headwinds. Following the outbreak of war in Iran, the market quickly priced in a rise in interest rates worldwide – yields on 10Y US Treasury bonds shot up by around 40bps from 3.98% to 4.38% – yet at the same time, long-term inflation expectations remained modest: in the USA, the 5Y/5Y inflation swap rate, which reflects the market’s assessment of the long-term inflation rate, actually fell from 2.40% to 2.32%! As the spread between market interest rates and inflation widened by almost half a percentage point as a result, the opportunity cost of gold – an asset with no calculable return – rose accordingly. From this perspective, it is therefore currently less attractive to hold gold rather than investments with a regular return, such as bonds.

Please note: Investments in securities such as bonds entail risks in addition to the opportunities described. Past performance is not a reliable indicator of future performance.

- The US dollar has performed unfavourably for gold since the end of February. The dollar index rose by a good 2.50% from 98 to over 100, making gold, which is traded in USD, more expensive for investors outside the USA. The dollar’s performance has therefore had a significant negative impact on the price of gold. However, contrary to some claims, its relative strength is not currently excessive.

- Analysts have significantly lowered their expectations of interest rate cuts following the outbreak of war. The market is now pricing in no interest rate cuts from the US Federal Reserve (Fed) this year – instead of the two cuts previously anticipated – while the European Central Bank (ECB) is expected to raise rates twice rather than potentially cutting them once. The less accommodative monetary policy than expected is having a very negative impact on gold, as the previously more accommodative interest rate policy was a key driver of the rally.

- Physical gold ETFs, which in 2025 had made massive purchases of gold for the first time in several years, played a significant role in the collapse of the gold price in March through their sales. At the start of the year, exchange-traded funds had still recorded high inflows. In March, the picture changed completely. The largest gold ETF, SPDR Gold, alone recorded outflows of around USD 25bn. It is likely that institutional investors sold highly liquid assets, such as exchange-traded gold funds, to cover losses in other assets or to meet margin calls.

Factors specific to 2026 and the Middle East

- A key factor behind the sharp rise in the price of gold in recent years has been the so-called “debasement trade”. This involves shifting capital from fiat currencies and government bonds into tangible assets such as gold in order to hedge against losses in purchasing power caused by high levels of government debt and rapidly expanding money supplies. This trend was further amplified by speculative positions, resulting in gold being heavily overweight on the long side – meaning there was excess demand. When market volatility rose significantly following the initial attacks, these positions were reduced on a large scale – partly to reduce risk in portfolios, and partly due to margin calls, which also occurred in the gold market.

- Another factor is that Dubai acts as the central hub for physical gold flowing from London to buyers in Asia. This channel is currently not functioning due to the war. Although this disruption is war-related and does not represent a structural change, a significant portion of physical demand is nevertheless absent.

- Some central banks, which had actually been buying up assets on a massive scale in recent years, have had to sell off their reserves to prop up their currencies or to circumvent sanctions. Turkey, for example, sold 80 tonnes of gold in March. The Polish central bank is also strategically reallocating its reserves and has sold several tonnes of gold.

What are the arguments in favour of gold at this level?

As highlighted above, there is currently plenty of headwind. However, several factors have been able to withstand this and continue to provide significant support for the price of gold: inflation, central banks, the debasement trade, gold discoveries and scarcity, as well as the (geo)political situation:

- Virtually no oil or LNG is transported via the Strait of Hormuz. We are feeling the effects first-hand – at the moment, admittedly, only at the petrol pump – but one thing is clear: rising transport costs will mean that energy prices will also have an impact on overall inflation. Unfortunately, this is by no means limited to energy prices: around a third of global urea exports originate from the Gulf region – a raw material that is critical for fertiliser production. As a result, agricultural products are also likely to become noticeably more expensive. All in all, it is foreseeable that inflation will rise again; the only question is to what extent.

- The “debasement trade” is more relevant than ever due to the war in Iran. A look back at history shows that, during times of war, budget deficits have always risen. The US government recently submitted a request for an additional USD 200bn in funding for the war and it is safe to assume that EU member states will also increase their defence spending. At the same time, economic growth is slowing, which reduces government revenues. In this situation, countries must issue more bonds to finance their deficits, which provides significant support for real assets such as gold.

- Central banks are continuing to make purchases. Although volumes have fallen slightly, they are stabilising at a high level. Due to US sanctions against Russia, many central banks are seeking to diversify their reserves. Consequently, some emerging markets and Russia’s allies, Iran and China, are keen to avoid the USD as a reserve currency and to buy more gold.

- The supply side is weakening in relation to the increased demand. Not a single major gold deposit has been discovered in the last two years. Mining companies are exercising strict investment discipline and are slow to respond to the rise in prices. Furthermore, the gold that remains in the ground is often found in deeper layers or in regions that are politically unstable.

- Political risks and geopolitical tensions are providing significant support for the price of gold, despite developments in March. As explained, other factors contributed to the slump; gold remains a defensive asset and is therefore sought after in times of (geo)political turbulence. We have experienced this virtually non-stop since Donald Trump took office: tariffs, the attack on Venezuela, the issue of Greenland, war in Iran, and no ceasefire in Ukraine.

The charts

There are therefore several aspects to consider when looking at gold. However, to assess short-term movements and the prospects for future developments, the technical picture is also essential.

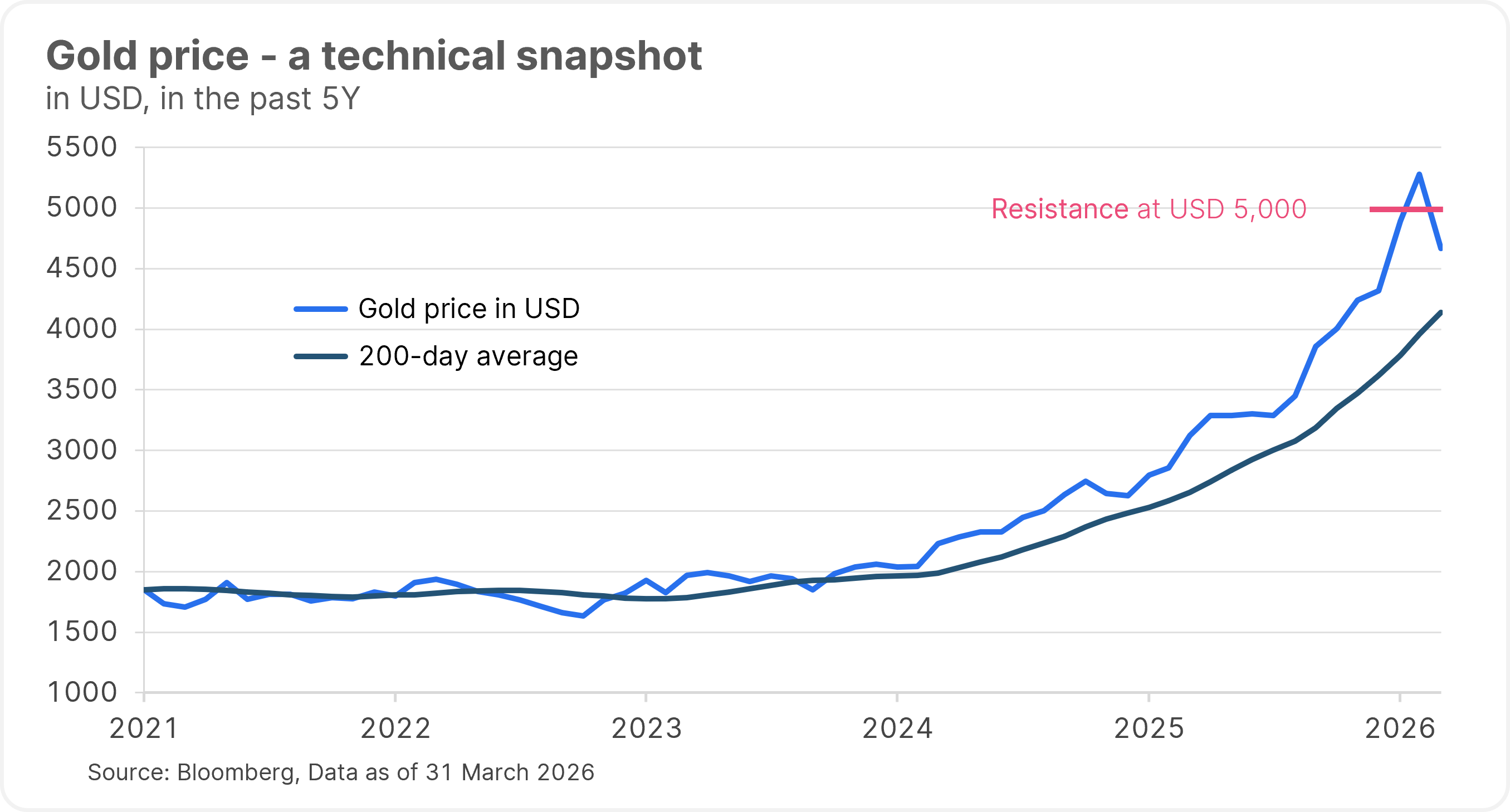

Although this picture is clearly gloomy, it is not hopeless. Gold reached an all-time high of over USD 5,600 per ounce at the end of January. The price failed to hold this level and corrected by more than 20% following the nomination of Kevin Warsh for the position of Fed Chair. The price subsequently bounced back quickly, rising above USD 5,400 in early March. Once investors realised that the war in Iran would last longer after all, the price plummeted sharply and, following a total fall of more than 20% within a week, it bounced off the 200-day moving average at USD 4,100. Since then, we have seen a sideways movement between USD 4,400 and USD 4,800, although the dollar remains strong.

Please note: Past performance is no reliable indicator of future value development.

Should the price fall again, the 200-day moving average would be the first strong level of support. Below that, the USD 4,000 level is worth watching, as it acted as support last autumn. On the upside, there is room to rise to practically USD 5,000 – a price that could prove to be a more significant hurdle. In any case, a sideways trend with significant volatility would come as no surprise.

Given the arguments outlined above, it would be logical to take a positive view of gold. However, should the war in the Middle East drag on, or even escalate, a sideways trend is certainly conceivable. After all, gold did virtually nothing for two years following the outbreak of the war in Ukraine. It was only exactly two years later, once a more accommodative interest rate policy by the Fed became increasingly likely, that the gold rally began.

Conclusion

Gold was unable to escape the knee-jerk reactions following the outbreak of war and fell sharply in March. This move was exacerbated by positioning, rising yields, the strong US dollar, and the metal’s high liquidity.

However, the factors supporting gold in the long term remain intact – with the possible exception of the US Federal Reserve’s loose interest rate policy. We should also bear in mind gold’s low correlation with traditional asset classes. Gold therefore remains not only the ultimate safe-haven asset, but also a valuable addition to the portfolio as a good instrument for diversification and a fundamental component of our asset allocation in Discretionary Portfolio Management.

Note: Investment in securities entail risks in addition to the opportunities described.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Central banks are becoming more cautious: these are the implications for the bond market

The investment package in Germany and the associated ‘abandonment of the debt brake’ has caused a lot of movement in the eurozone bond market. Meanwhile, central banks have to manage the balancing act between slowing economic growth and rising inflation. Dániel Bebesy, Fixed Income Portfolio Manager at Erste Asset Management Hungary, talks in an interview about the recent central bank meetings and their impact on the bond market.

US tariffs trigger a price slide – what to do now

The latest US tariffs have caused considerable turbulence on the financial markets worldwide. What is the background to the tariffs and how can investors react in the current environment?

Five years since Covid hit: a historic crash, and the lessons learned

This week marks the fifth anniversary of the low point of the coronavirus crash. In February and March 2020, global financial markets experienced one of the fastest downturns in history. The coronavirus crisis brought the economy to a virtual standstill and caused a massive decline in stock prices, unsettling many investors.

Our new blog post looks back at the events that led to this crash and analyses what lessons investors can learn from the Covid crash. Because as quickly as prices fell, they were also largely able to recover the losses.