The results of the presidential and congressional elections in the United States a year ago brought and continues to bring changes in many areas. Donald J. Trump was elected the 47th President of the United States, and the Republican Party gained a majority in both chambers of Congress (Senate and House of Representatives).

The swearing-in ceremony on 20 January 2025 marked the beginning of the US President’s second term in office and, in contrast to his inauguration eight years ago, this time it had been preceded by years of preparation. On the very first day of his term, Donald Trump signed more than 20 executive orders on issues such as the environment, energy, health, security, immigration, and development aid. Their number has since grown to over 150 – although the future of these decrees is uncertain, as they can be amended, revoked, or declared invalid by the courts.

The measures taken in recent months affect the American population across a wide variety of areas of life. But what are the potential implications for the US federal budget, the creditworthiness and thus the rating of the United States and, consequently, the global financial markets?

Initial situation

Naturally, the election manifestos of both parties lacked measures for a sustainable improvement in the US budget deficit.

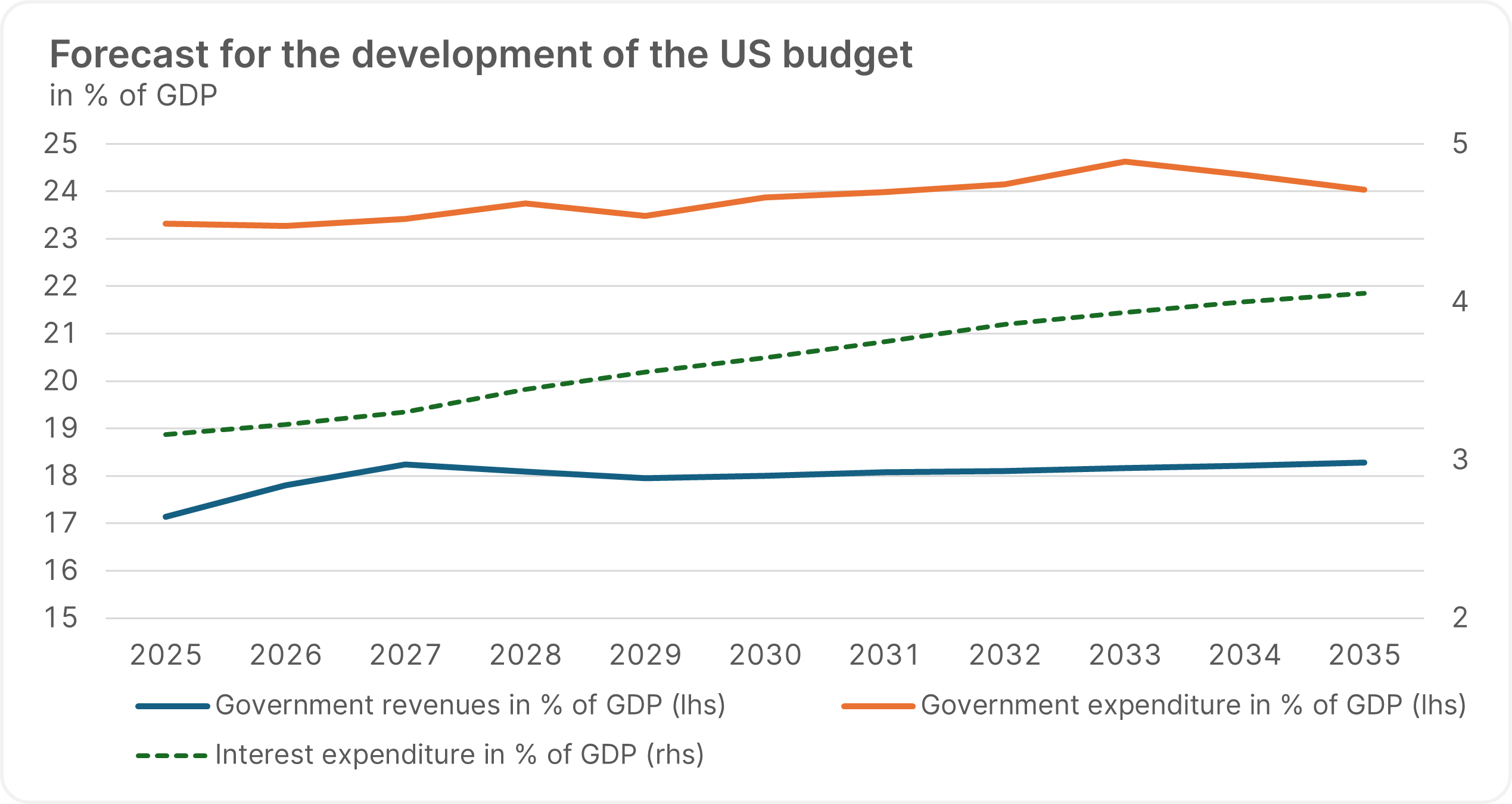

At around -6% (of which the primary deficit excluding interest payments is about -3%), the current overall deficit is at a level that appears unsustainable in the medium to long term. Even if revenues could rise from around 17% to 18.3% of gross domestic product according to the latest forecast, estimates suggest that spending is expected to increase by at least a similar amount. The resulting additional financing requirements could lead to an increase in interest expenditure of about 1% of GDP, from the current 3.2% to 4.1% in 2035.

Note: Prognoses are not a reliable indicator of future performance.

Source: Congressional Budget Office (CBO), 10-Year Budget Projections, as of January 2025

Government expenditure

The planned reduction in government spending is often promoted with slogans such as “cutting red tape” and “increasing efficiency”. The USA is no exception here, and one of the first measures taken by the new administration upon taking office was the creation of the Department of Government Efficiency (DOGE). However, the establishment of a ministry requires the approval of the US Congress, which is why DOGE was incorporated into the existing structure as a sub-unit and Elon Musk was appointed as a special representative of the US government.

The term of appointment as special representative was limited to 130 days per year, and the rapidly communicated success was increasingly met with criticism of the waves of civil servant redundancies, the credibility of the published savings figures, and the general approach. Assessing the reliability of the available figures is challenging and becoming increasingly difficult, as DOGE’s activities have taken a back seat since the rift between the US President and Elon Musk in May.

In the Department of Government Efficiency (DOGE), Elon Musk was supposed to reduce bureaucracy and cut spending as a special representative of the US government. DOGE has since been dissolved. (c) APA-Images / Zuma / Francis Chung

The U.S. Office of Personnel Management estimates that approximately 300,000 jobs could be terminated by the end of the year, and statements made in early November suggest that a 4:1 ratio (4 terminations per new hire) is likely to be achieved. However, no meaningful statistics on the actual amounts and savings volumes are currently available.

The US healthcare system has also been earmarked for cuts. This is a hot topic in the current debate surrounding the recent shutdown, as government subsidies under the Affordable Care Act, colloquially known as Obamacare, are set to expire at the end of the year. The Republican Speaker of the US House of Representatives, James Michael (“Mike”) Johnson, recently promoted a proposed solution that would address the significant premium increases in health insurance for parts of the population and improve the healthcare system. However, he has yet to provide the public with any details. Either way, there are growing calls within the Grand Old Party for a solution to this problem in order to increase their chances of re-election in the upcoming midterm elections. The impact of any reform on the budget is currently unclear and cannot be predicted.

Government revenues

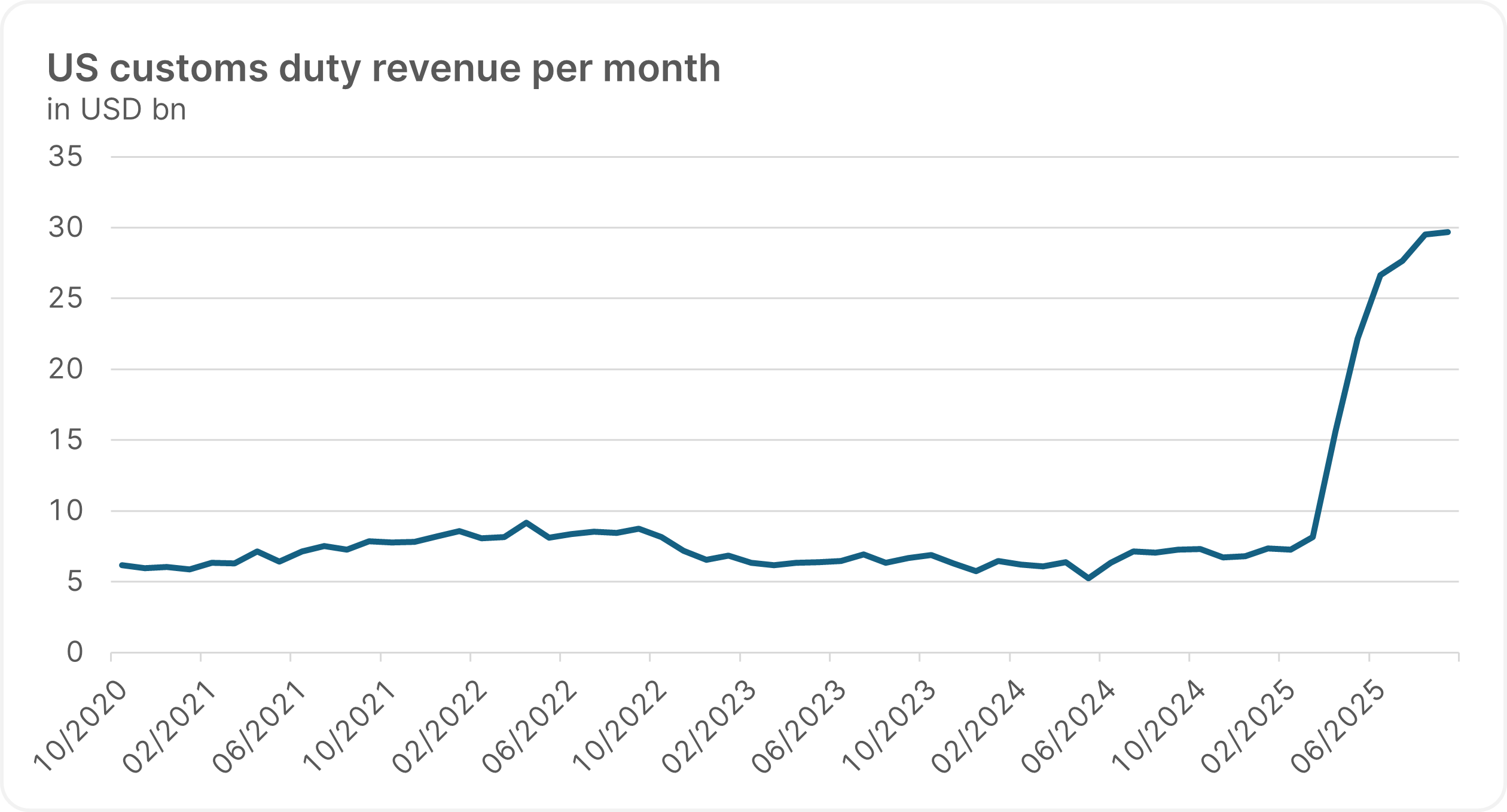

According to Donald Trump himself, the most beautiful word in the dictionary is “tariff”. Tariffs are currently regarded as a universal bargaining chip in many respects. Protecting key areas and sectors of the US economy securing the necessary resources and raw materials is one aspect of current tariff policy, while generating revenue to finance the critical election promises of the last campaign is another. These promises include extending the tax cuts from the Tax Cuts and Jobs Act, tax relief on overtime and tips, and increasing spending on defence and border security. In the past fiscal year, i.e. from October 2024 to September 2025, customs duties amounting to approximately USD 195bn were levied.

Source: U.S. Department of the Treasury – Monthly Treasury Statement (MTS), as of September 2025

Since the beginning of April (“Liberation Day”) and the introduction of reciprocal tariffs, revenues have risen significantly and, at about USD 30bn per month, would contribute significantly to financing election promises. However, the Supreme Court’s decision on their legality and thus their continuation in their current form is still pending. The core issue is whether the reasoning of a national emergency (IEEPA, International Emergency Economics Power Act) is justified, as tax policy would fall within the remit of the US Congress.

In the event of a negative court ruling, the administration has announced that it intends to pursue alternative avenues. Continuing the tariff policy seems conceivable on the basis of other legal rationales but could become more difficult or time-consuming. Alternative options for introducing tariffs may be limited in terms of amount or duration, or may offer less flexibility.

It therefore remains to be seen how the Supreme Court will rule and what impact this ruling will have on the revenue side of the budget. Recent statements by the US President promising parts of the population payments from these revenues would in any case make budget consolidation via customs revenues more challenging.

The financial markets

Investors on the capital markets are closely monitoring developments and changes. The discussions about the independence of the US Federal Reserve are unlikely to have strengthened their confidence, to say the least. International trade relations are being put to the test by the effects of protectionist trade policy, and the introduction of reciprocal tariffs has led to a sharp rise in volatility on the financial markets and a high level of uncertainty.

In May 2025, Moody’s (the last of the three major rating agencies) stripped the United States of its top Aaa rating and downgraded it by one notch (with a stable outlook). The main reason for this were years of lacking reforms to rein in the budget deficit.

Outlook

The political environment for a consensus-based proposal to counteract debt development in the long run does not appear to be in sight at this point in time. It is fair to assume that expensive promises will also be made to win voters’ favour in next year’s midterm elections. The longest shutdown in US history is possibly further evidence that the possibility of broad-based political solutions has not become any easier under the current conditions in recent months.

However, it is also a fact that the US financial market occupies a special position globally and that US Treasury bonds are unrivalled due to their excellent credit rating, high liquidity, and market depth. Uncertainty on the capital markets has become significantly less noticeable with the conclusion of many trade agreements in recent weeks, and the US dollar remains the undisputed global reserve currency. This should continue to support demand for US Treasury bonds, even if far-reaching reforms may not materialise for the time being.

The innovative strength of companies and the economic potential of the United States of America should not be underestimated in the future. Developments in recent months confirm the views of those who had focused more strongly on the USA, and it may be advisable to keep a close eye on changes and their effects in the coming weeks and months.

Note: Please note that investing in securities entails risks in addition to the opportunities described.

Legal disclaimer

This document is an advertisement. Unless indicated otherwise, source: Erste Asset Management GmbH. The language of communication of the sales offices is German and the languages of communication of the Management Company also include English.

The prospectus for UCITS funds (including any amendments) is prepared and published in accordance with the provisions of the InvFG 2011 as amended. Information for Investors pursuant to § 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in conjunction with the InvFG 2011.

The currently valid versions of the prospectus, the Information for Investors pursuant to § 21 AIFMG, and the key information document can be found on the website www.erste-am.com under “Mandatory publications” and can be obtained free of charge by interested investors at the offices of the Management Company and at the offices of the depositary bank. The exact date of the most recent publication of the prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the key information document are available, and any other locations where the documents can be obtained are indicated on the website www.erste-am.com. A summary of the investor rights is available in German and English on the website www.erste-am.com/investor-rights and can also be obtained from the Management Company.

The Management Company can decide to suspend the provisions it has taken for the sale of unit certificates in other countries in accordance with the regulatory requirements.

Note: You are about to purchase a product that may be difficult to understand. We recommend that you read the indicated fund documents before making an investment decision. In addition to the locations listed above, you can obtain these documents free of charge at the offices of the referring Sparkassen bank and the offices of Erste Bank der oesterreichischen Sparkassen AG. You can also access these documents electronically at www.erste-am.com.

Our analyses and conclusions are general in nature and do not take into account the individual characteristics of our investors in terms of earnings, taxation, experience and knowledge, investment objective, financial position, capacity for loss, and risk tolerance. Past performance is not a reliable indicator of the future performance of a fund.

Please note: Investments in securities entail risks in addition to the opportunities presented here. The value of units and their earnings can rise and fall. Changes in exchange rates can also have a positive or negative effect on the value of an investment. For this reason, you may receive less than your originally invested amount when you redeem your units. Persons who are interested in purchasing units in investment funds are advised to read the current fund prospectus(es) and the Information for Investors pursuant to § 21 AIFMG, especially the risk notices they contain, before making an investment decision. If the fund currency is different than the investor’s home currency, changes in the relevant exchange rate can positively or negatively influence the value of the investment and the amount of the costs associated with the fund in the home currency.

We are not permitted to directly or indirectly offer, sell, transfer, or deliver this financial product to natural or legal persons whose place of residence or domicile is located in a country where this is legally prohibited. In this case, we may not provide any product information, either.

Please consult the corresponding information in the fund prospectus and the Information for Investors pursuant to § 21 AIFMG for restrictions on the sale of the fund to American or Russian citizens.

It is expressly noted that this communication does not provide any investment recommendations, but only expresses our current market assessment. Thus, this communication is not a substitute for investment advice.

This document does not represent a sales activity of the Management Company and therefore may not be construed as an offer for the purchase or sale of financial or investment instruments.

Erste Asset Management GmbH is affiliated with the Erste Bank and austrian Sparkassen banks.

Please also read the “Information about us and our securities services” published by your bank.

More on the topic

Deficit spiraling out of control: French government plans drastic austerity program

The high deficit in the French national budget is forcing the new government to implement drastic austerity measures. Investors are keeping a close eye on the announced plans, as the tense financial situation has been noticeable on the stock market for some time.

What effects could DeepSeek have on the technology sector?

The new AI model from Chinese start-up DeepSeek caused a stir on the stock market a fortnight ago. The seemingly much more efficient and therefore cheaper model caused the share prices of many a tech heavyweight to plummet. Although the initial market reactions were probably exaggerated, one question remains: what long-term impact will DeepSeek have on the big tech companies?