Since the beginning of November, both risky security classes such as equities and credit-safe government bonds have recorded price increases. The US dollar, which is said to be an anti-cyclical currency, and the price of oil have thus fallen.

The market appears to be increasingly pricing in a so-called “soft” landing for the economy. The probability of this actually increased over the course of the year. Nevertheless, the economic data published in recent weeks and months does not contradict the “hard” landing scenario either.

Falling inflationary pressure

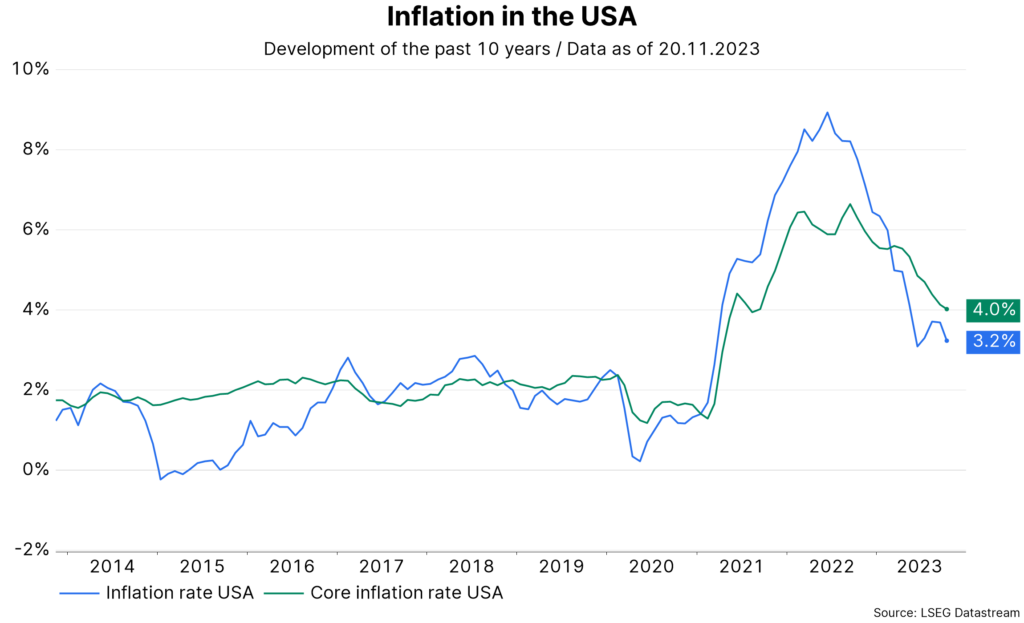

Last week, the most important economic report was consumer price inflation for the month of October for the USA. Compared to the previous month, prices remained unchanged, mainly because energy prices fell (-2.5% p.m.). Year-on-year inflation fell from 3.7% to 3.2%.

Most importantly, the various measures of underlying inflation showed a month-on-month decline in inflation. The traditional core rate, i.e. the overall figure excluding the volatile food and energy components, amounted to 0.2% p.m. after 0.3% p.m. in the previous month. Year-on-year inflation fell from 4.1% to 4.0%.

Note: Past performance is not a reliable indicator for future performance of an investment.

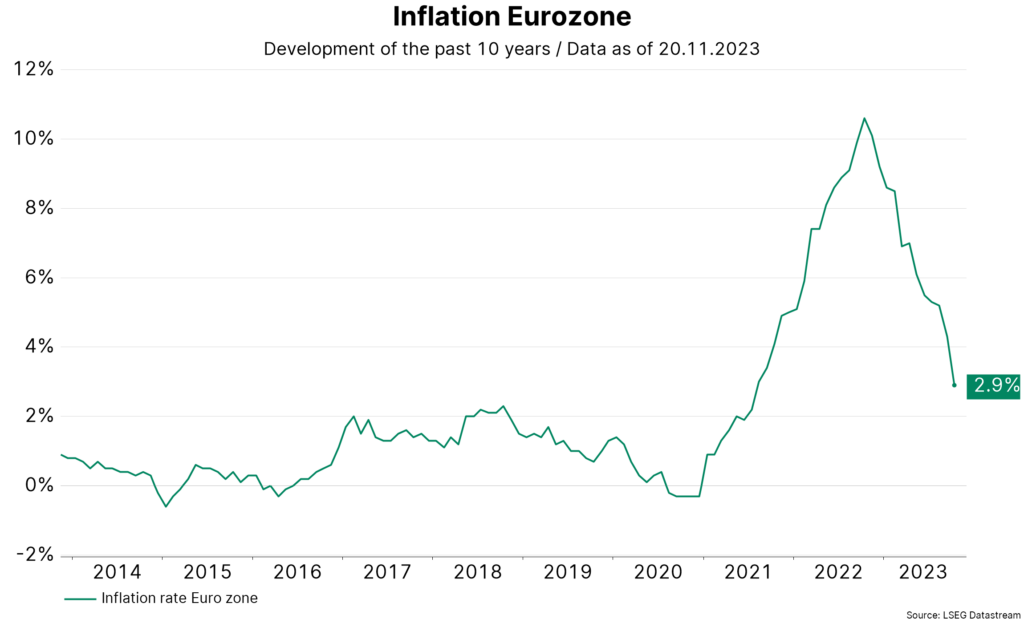

Slowly falling inflation, also known as disinflation, can also be seen in many other countries. In the eurozone, consumer price inflation fell from 4.3% in September to 2.9% in October, while the core rate fell from 4.5% to 4.2%. In the OECD area as a whole, inflation has fallen from its high in October 2022 (10.7%) to 6.2% (in September 2023). Overall, inflation rates are trending downwards, but the levels are still too high.

Note: Past performance is not a reliable indicator for future performance of an investment.

Slowly declining demand on the labor market

In addition to falling inflation, the second important development at the macroeconomic level is a slow weakening of the still very tight labor market. Unemployment rates remain at a very low level. In September, the unemployment rate for the entire OECD area was just 4.8%. This is very close to the cyclical low of June.

However, the number of job vacancies is trending downwards in many countries. In the USA, job vacancies have fallen from around 12 million (March 2022) to 9.5 million (September 2023). A similar trend can be observed in Germany (May 2022: 870.000, September 2023: 731.000). To date, the widely expected decline in demand on the labor market has therefore not taken place via a significant increase in the unemployment rate, but primarily via a decline in job vacancies.

Note: Past performance is not a reliable indicator for future performance of an investment.

Trend growth

Against the backdrop of the sharp and rapid increases in key interest rates, economic growth has remained surprisingly strong. In fact, central banks raised the average key interest rate in the OECD area from 0.5% at the beginning of 2022 to 5.7% in September 2023.

The significant tightening of the monetary policy environment had led to fears that economic activity could be severely dampened with an uncertain time lag (falling gross domestic product, significantly rising unemployment rate). However, real gross domestic product grew by 0.5% from the first to the second quarter. This may not sound like much, but it represents an annualized figure of 2% and is actually in line with the long-term average (since 2000).

The strong growth in the USA in the third quarter (4.9% annualized) may even have boosted OECD growth, although both the eurozone (-0.2%) and Japan (-2.1%) are showing signs of contraction. Historically, restrictive monetary policies will significantly dampen economic growth. However, this is “merely” a statistical view. The most important argument for avoiding a “hard” landing is that the continuation of the falling inflation trend would cause real incomes to rise and central banks would soon cut key interest rates.

Resilient financial system

Not only has there been a positive surprise in terms of growth, but the indicators for the state of the financial markets also show surprising resilience. The fear was that the rapid increases in key interest rates could lead to liquidity crises and bankruptcies. However, the previous liquidity crises (UK pension funds, US banks) were quickly digested. The various indicators on financial conditions are currently at an average level.

Conclusion: “Soft” landing not yet clear

Before the description of the economic environment sounds too positive. Inflation is still too high. For this reason, central banks will continue to pursue a restrictive policy. However, because inflation is trending downwards and monetary policy only affects economic activity with an uncertain time lag, the central banks have now adopted a wait-and-see stance.

However, this is not a pivot towards an easing of monetary policy. The central banks want to avoid the mistakes of the 1970s. Back then, key interest rates were too low and key interest rates were cut too early. What remains: Falling inflation is encouraging, but a continuation of this trend is needed for a “soft” landing for the economy. However, this is by no means clear.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.