Low productivity growth

Data on productivity growth in the USA showed an unfavorable picture. Hours worked, calculated from employment multiplied by average hours, rose strongly by 2.3% year-on-year. Because economic output rose by only 1.3% at the same time, productivity fell by a rounded one percentage point (negative productivity growth).

Compensation per hour worked increased by 4.8%, which is why unit labor costs, calculated as compensation minus productivity growth, rose by 5.8%. The development of unit labor costs is the most important determinant of inflation in the long run. Since 1960, unit labor costs have grown at an average annual rate of 2.9%, while the core rate of personal consumption expenditure inflation (core PCE deflator) has risen by 3.2%.

Firm labor market

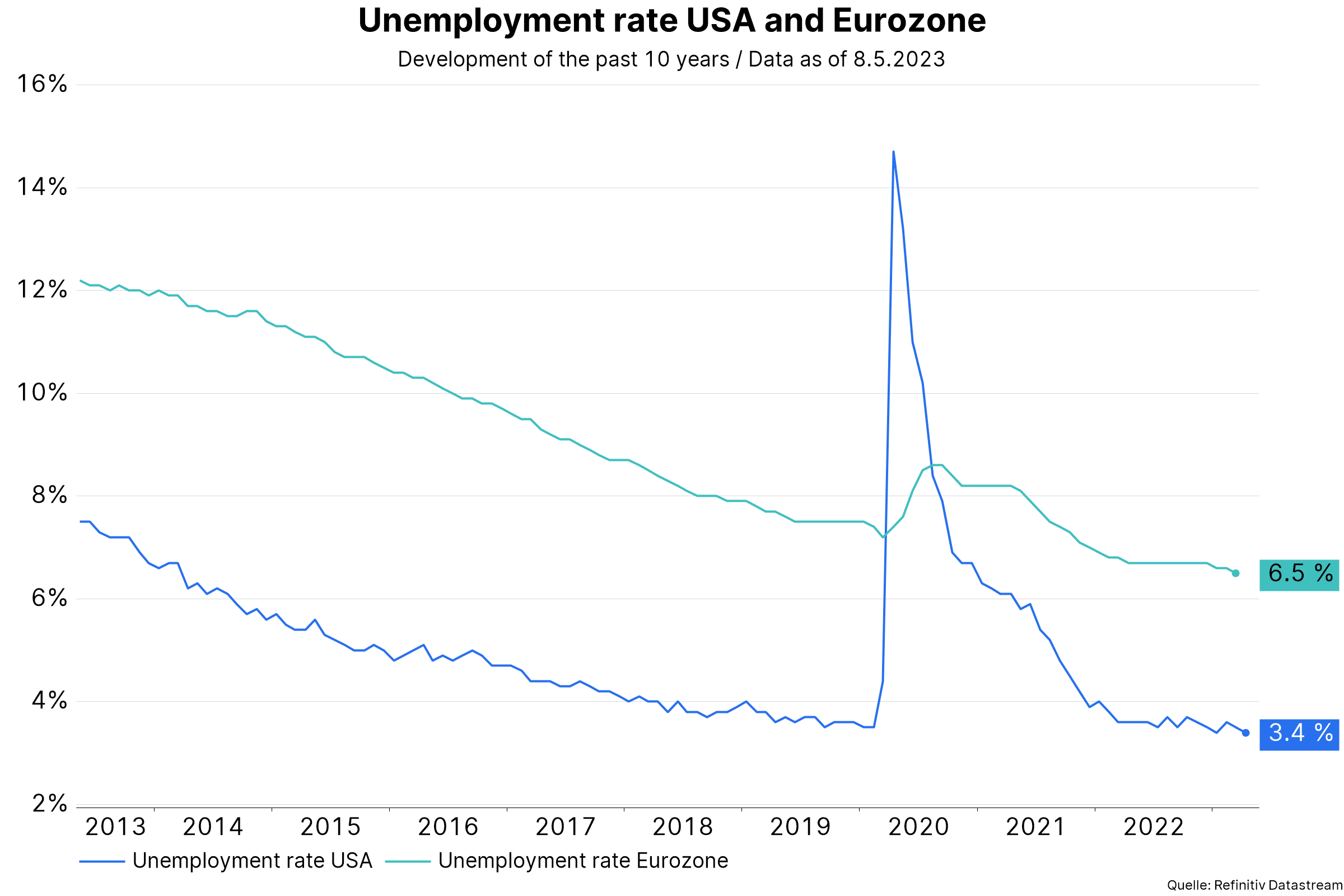

Overall, the labor markets remain very firm, i.e. in disequilibrium. In the USA, the unemployment rate was very low at 3.4% in the month of April. The Congressional Budget Offict estimates that full employment without inflationary pressures is one percentage point higher. At the same time, the JOLTS report for the month of March continued to show a very high ratio of job openings to unemployed, but the trend is downward. A soft landing for the economy equates to a significant decline in job openings without a sharp increase in the unemployment rate.

Granted, so far the data are pointing in the right direction, but the risk of a sharp rise in the unemployment rate, synonymous with a recession, remains elevated. This is because the central bank is trying to reduce inflation with a restrictive monetary policy. The situation is similar in the euro zone. In March, the unemployment rate reached a new historic low of 6.5%. At the same time, the gross domestic product in the first quarter grew by only 0.1% quarter-on-quarter and 1.3% year-on-year. A soft landing in the euro zone is possible, but the restrictive monetary policy underscores the downside risks.

Positive growth momentum

The global Purchasing Managers’ Index for April rose for the fourth month in a row. With a value of 54.2, the index is well above the theoretical threshold of 50 that distinguishes expansion from contraction. Translated to real global GDP, the index implies growth of around 3% annualized (that is, annualized). In this context, the difference between the weak manufacturing sector and the strengthening in the services sector is widening. It is striking that in the manufacturing sector, new orders are shrinking slightly and employment is only slightly above the 50 mark. In contrast, in the services sector both indicators show an upward trend and are clearly in growth territory.

The development of selling prices also fits in with this: Falling but still slightly in the growth range in the manufacturing sector, rising and clearly in the growth range in the services sector. An important question regarding future development is whether this gap will be closed via a recovery in the manufacturing sector or a slowdown in the service sector. On the positive side, the report contradicts fears for an immediate recession. Unfortunately, this also dampens hopes for a rapid decline in inflation.

Pause in the rate hike cycle

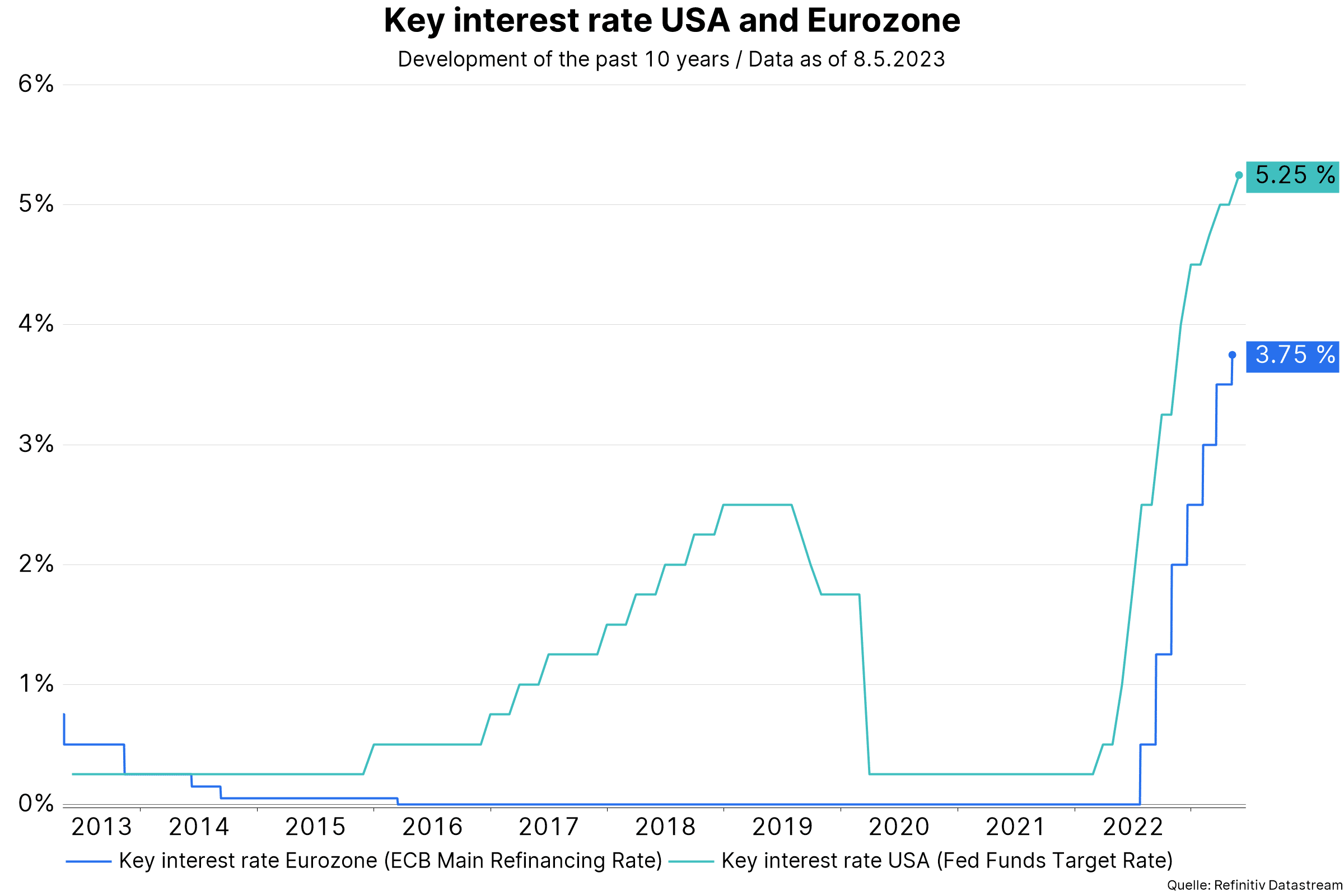

Despite uncomfortably high inflation, more and more central banks are signaling a pause in the rate hike cycle to better assess the effects of previous rapid rate hikes. In the U.S., the Fed raised the key interest rate further by 0.25 percentage points. The upper band for the effective key interest rate is now at 5.25%. The forward guidance, according to which the Fed expects that further key rate hikes may be appropriate, was dropped. A slight bias for further hikes was maintained, but overall, statement and press conference signal a pause.

However, a pause does not mean the end in the rate hike cycle, as last week’s surprise rate hike by the Reserve Bank of Australia demonstrated. Moreover, high inflation does not justify key rate cuts for the second half of the year, which are reflected in market prices. The European Central Bank also raised its key interest rates by 0.25 percentage points. The interest rate on the deposit facility is now at 3.25%. The main point to highlight in the ECB’s statement is that the cumulative key rate hikes are transmitted forecully to the monetary and financial environment. Indeed, the latest ECB Bank Lending Survey showed a further tightening of lending standards and a further weakening of credit demand.

More time in achieving the inflation target

Central banks are signaling a somewhat less sharp (hawkish) stance because an effect of the rapid key rate hikes on the monetary and financial environment has already become visible. Monetary policy is expected to have a restrictive effect, but not to become much more restrictive, because this would (once again) increase the risks of recession. This is probably to avoid the classic monetary policy mistake that often the last key rate hikes were too much and unnecessarily triggered a recession.

Inflation is still uncomfortably high, but an overall tight environment could gradually lower inflation. So central banks seem to be taking more time to reach their 2% inflation target. This is even more true when one considers that inflation is a lagging indicator of economic activity. The stumbling block in this story is that central banks may once again misjudge underlying inflation as being lower than it actually is.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.