Global real gross domestic product (GDP) growth is expected to cool from 4% in the first quarter to around 2% in the current quarter. One reason for this is the weaker expected economic growth in China, the world’s second largest economy.

Growth momentum in China cooling off

The dynamics of global real economic growth are strongly influenced by the development of GDP in China. After the pandemic-related opening measures at the end of 2022, GDP in China showed a V-shaped recovery with growth approaching 12% quarter-on-quarter (annualized) in the first quarter.

Growth indicators released for April (retail sales, investment and industrial production) point to a marked slowdown. The estimate for the current quarter is around 4%.

Low growth in the USA and in the Euro zone

For the USA, the aggregate of economic indicators points to continued low growth below potential. After quarterly real GDP growth of 1.1% (annualized), the estimate for the current quarter holds at 1%. In the month of April, retail sales increased after declines in the previous two months. Overall, private consumption grew strongly in the first quarter. Growth early in the second quarter suggests that consumers will continue to support GDP growth in the second quarter.

Industrial production continued to recover from the Q4 2022 slump, but the level is still slightly below the November level. In the construction sector, there are increasing signs of stabilization. For example, the NAHB index, a key sentiment barometer, has been rising since the beginning of the year. In the first quarter, residential investment still reduced GDP.

Growth in the euro zone was confirmed with an increase of 0.3% (annualized) quarter-on-quarter. The GDP components have not yet been published. However, the 0.6% (annualized) contraction in industrial production in the first quarter suggests a contribution to growth in the service sector.

Pressure for further key interest rate hikes remains in place

At the same time, employment in the euro zone increased by 2.4% (annualized) quarter-on-quarter. The labor market thus remained tight. In March, the unemployment rate reached an all-time low of 6.5%. Thus, the mismatch between a tight labor market and weak economic growth remains in the euro zone as well. The result is a deterioration in labor productivity and increasing pressure for higher unit labor cost growth.

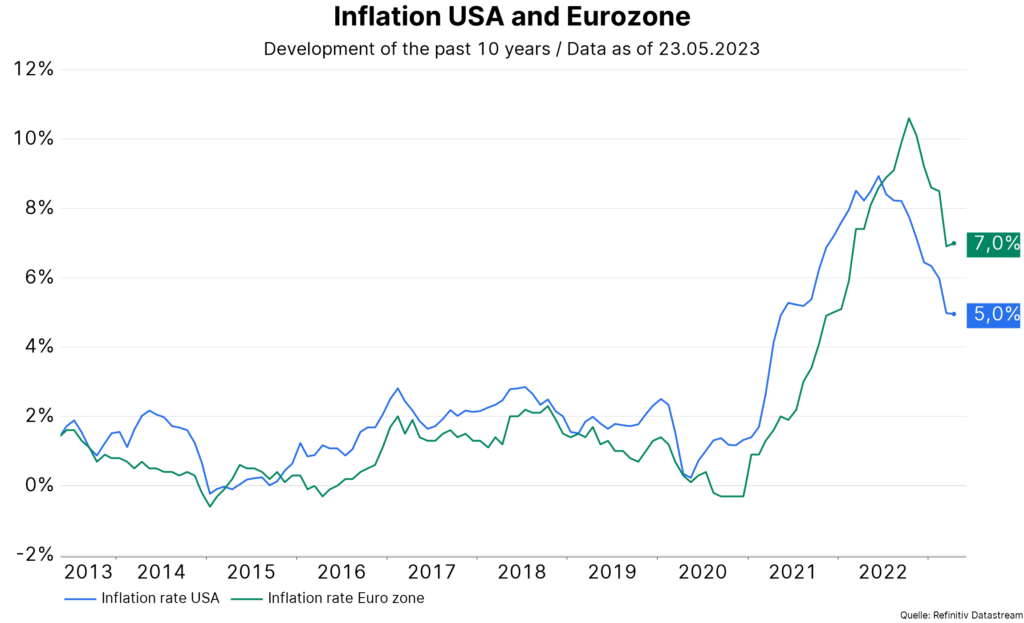

The latter is an important determinant of long-term inflation developments. Consumer price inflation was confirmed at 7.0% y/y for the month of April. The European Central Bank thus remains under pressure to raise key interest rates further. The main refinancing rate currently stands at 3.75%. However, the further tightening of lending guidelines and the further decline in demand for credit reduce the potential of total future interest rate hikes.

Growth risks

At the same time, in the USA, the Conference Board’s Leading Index declined for the thirteenth time in succession, once again pointing to recession risks. In addition, the numerous survey-based reports from the regional central banks (NY Fed, Philadelphia Fed) are tending toward weakness.

In Germany, the ZEW index (for expectations), an important barometer of investor sentiment, fell for the third month in a row. Between October and February, the index showed a strong recovery, influenced primarily by the sharp drop in energy prices. In the meantime, sentiment has clouded over again.

On the market side, the ten-year yield on US government bonds is around 0.6 percentage points below the two-year yield. This describes a so-called inverse yield curve and is a reflection of a restrictive monetary policy with the associated recession risks. However, the market is increasingly focusing on the possibility of a technical bankruptcy of the USA.

Negotiations on debt ceiling

In June, the USA will probably reach the limit above which the Treasury is not allowed to increase the debt any further (debt ceiling). This means that the USA would not be able to service its financial obligations. Negotiations between US President Joe Biden and Speaker of the House of Representatives Kevin McCarthy on Tuesday night again ended without a result.

The problem is the pronounced polarization of the two parties, the Democrats and the Republicans. A technical bankruptcy of the US would trigger a strong uncertainty, because the government bond curve is the most important reference for the entire global financial market.

The working assumption is a further postponement of reaching the debt ceiling by a few months. Any timely agreement between the two parties would likely involve significant government spending cuts. Technically, this would have a dampening effect on the economy, which would help monetary policy in reducing inflation. In addition, as in the eurozone, there has been a further tightening of lending standards and a decline in the demand for credit.

Mainly because the various measures of underlying inflation have fallen more in the US than in the eurozone, unlike the ECB, the US central bank may pause in the rate hike cycle in June. The upper range for the effective key interest rate is currently 5.25%.

Conclusion

On the positive side, published growth indicators are consistent with a “soft” landing. That would mean weak economic growth, falling inflation and a foreseeable end of key rate hikes. This scenario currently appears to be reflected in market prices.

On the negative side, the full effect of the key rate hikes on growth will only become visible with a considerable time lag. Moreover, the decline in inflation may be too slow or inflation may stabilize above the central banks’ inflation target. Because economic growth in the developed economies is already meager, not much is missing for a contraction. Recession risks remain uncomfortably high.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.