The environment for the financial markets has improved, although some developments continue to give cause for concern. This is mainly for three reasons:

- In the US, the “soft” landing scenario (falling inflation without recession) has become much more likely.

- In China, the overcoming of deflationary pressures has become somewhat more realistic due to the announcement of unexpectedly extensive stimulus measures (at the monetary and fiscal level).

- The dockers’ strike on the US East and Gulf coasts has been temporarily ended. This eliminates or postpones an important stagflationary risk (higher prices, lower growth).

However, any of the three points could be a game-breaker for the Goldilocks party in the markets. Stubborn inflation in the service sector, an escalation in the Middle East, the uncertainty surrounding the outcome of the US elections, a possible EU-China tariff conflict over electric cars or a weak manufacturing sector – there would be plenty of potential risk factors.

Boom phase

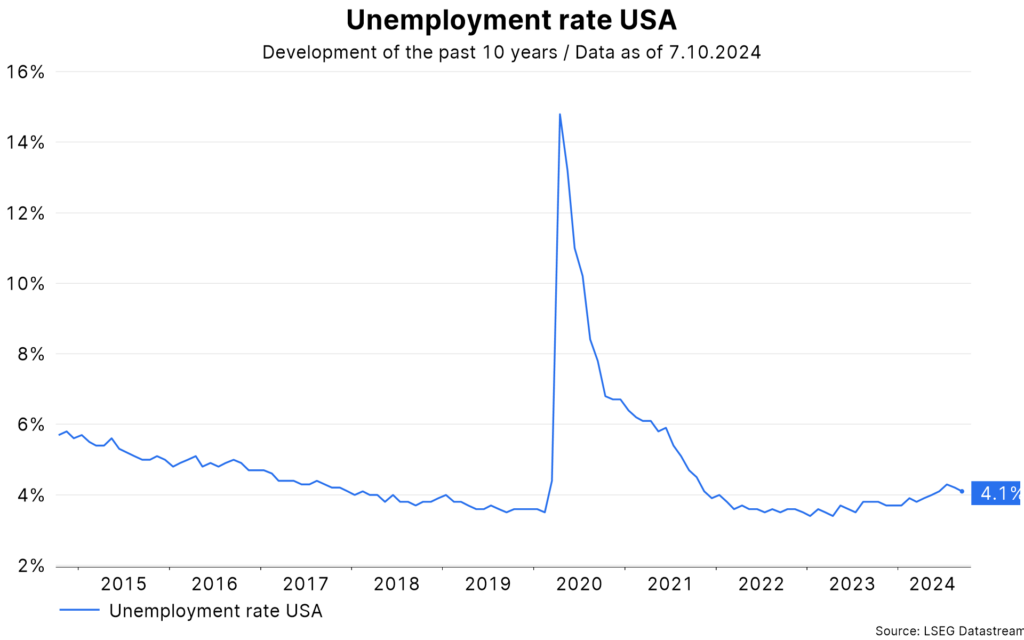

Last week showed one thing: economic growth in the US is above potential. The estimate for the third quarter is an annualized 2.5% (source: Nowcast by the Atlanta Fed). This means that the boom phase has continued into the third quarter. At the same time, labor market indicators have been pointing to a slowdown for months. Because the unemployment rate has the special characteristic of often being followed by a sharp increase after moderate increases, the risks for the economy were on the downside (= recession).

However, last week’s labor market data surprised on the upside with surprisingly strong employment growth and an unexpected decline in the unemployment rate. This has narrowed the gap between strong economic growth and the weakening labor market.

Strong employment growth

In detail: the number of new jobs created in the non-agricultural sector rose by 254,000 in September. This figure is well above expectations of 150,000 and above the figure for the previous month (159,000). The figures for the two previous months were also revised upwards. Before the September report, the three-month average of new jobs created had fallen to just 116,000. With the new September data, this figure has also risen to 186,000.

The unemployment rate thus fell for the second month in September (to 4.1%), after having trended upwards from January 2023 (3.4%) to July 2024 (4.3%).

At the same time, the participation rate remained unchanged at 62.7% over the last three months. Compared to January 2023 (62.4%), it is slightly higher. The reason for the increased unemployment rate is not a reduction in employment.

Rising wage growth

In terms of remuneration, average hourly wages rose by 0.4% month-on-month to 4.0% year-on-year. This is well above the recent July low of 3.6%. The rise in wage growth implies upward risks to the achievement of the inflation target (2%).

High productivity growth

However, the average weekly hours worked fell from 34.3 to 34.2. This means that total hours worked fell by 0.1% month-on-month. With the estimate for real GDP growth coming in at a high 2.5% annualized, the decline in hours worked implies a strong increase in labor productivity: 2.5% economic growth minus 0.8% hours worked (0.2% annualized) yields a gain of 1.7% annualized in the third quarter). Higher productivity eases inflationary pressure on the wage side.

Soft landing

However, some other survey-based labor market indicators continue to point to a slowdown. For example, the purchasing managers’ indices (PMIs) and “jobs plentiful minus jobs hard to get” in consumer sentiment. The divergence between these indicators and the strong increase in employment is difficult to sustain. One of the two sides will correct.

Moreover, too much weight should not be given to a single data point – in this case the September labor market report. All published economic data exhibit random fluctuations and are revised with subsequent more accurate estimates. Nevertheless, the US labor market data makes a “soft” landing scenario appear even more likely. This environment is favorable for risky asset classes such as equities. However, investment-grade government bonds suffer because both the speed and the overall extent of key interest rate cuts are lower.

No landing

However, the soft landing scenario involves not only avoiding a recession, but also sustainably achieving the inflation target. In this context, the publication of consumer price inflation for September will be in the spotlight in the coming days. Estimates point to a decline in the headline figure excluding food and energy (core rate: 0.2% mom, 2.3% yoy).

If the rise in inflation is higher than expected, the scenario of a failure to achieve a soft landing (inflation remains high) could be discussed more. In this scenario, the central bank has little scope to lower key rates. In this case, not only bonds but most asset classes would suffer initially.

Note: Please note that forecasts are not a reliable indicator of future performance.