Winzer of the Week

The weekly market commentary by Chief Economist Gerhard Winzer

Since US President Donald Trump took office, uncertainty has increased on several levels. Initially, the markets had hoped that Trump’s political measures would be less disruptive than announced during the election campaign.

However, the announcements have become more extreme with the latest tariff increases. The stock indices are reacting negatively to this.

Out of balance

The new US government is turning a lot of things upside down and doing so at a rapid pace. The expectation was that the possible positive effects (deregulation, tax cuts) would be able to offset the possible negative effects (restrictive trade and immigration policy). As long as the four areas remained in an intellectual balance, this would have been possible. However, with the tariff increases on imports from Canada, Mexico and China, the measures have taken an extreme turn.

Tariff increases

The following new tariffs were announced on March 3:

- Entry into force of the delayed 25% tariffs on Mexico and Canada.

- Additional levy of 10% on Chinese imports. The overall quota now stands at 20%.

- In addition, 25% tariffs on aluminum and steel imports are to come into force on March 12.

- Canada and China have responded with their own tariffs. A trade war is looming.

- Further tariff increases in the USA could follow in April. An analysis on the reciprocity of trade barriers will be published in the USA on April 1.

Tariff increases can pursue three objectives: Non-trade objectives (border security, curbing drug trafficking), unfair trade practices or increased government spending. If the main objective is indeed to reduce the trade deficit in order to increase manufacturing in the US, a trade war is indeed looming. This could dampen economic growth and fuel inflation in many countries. Sentiment is an important channel of impact here. In the US, for example, a fall in sentiment could lead to a decline in investment, employment and consumption.

Defense

There have also been other negative developments. Firstly, new developments have emerged that are not only relevant in the long term: This is about nothing less than a new world order: alliances are de facto being terminated (keyword: US military aid for Ukraine) or called into question (keyword: NATO).

One direct effect of this is that the EU countries are announcing a massive increase in defense spending. The CDU/CSU and the SPD in Germany agreed on a billion-euro financing package for defense and infrastructure. At a press conference, CDU/CSU Chairman Friedrich Merz made it clear: “I want to make it very clear: in view of the threats to our freedom and peace on our continent, ‘Whatever it takes’ must now also apply to our defense”.

CDU/CSU and SDP have agreed on a billion-euro defense and infrastructure package as part of their exploratory talks for a future government. Credit: Kay Nietfeld / dpa / picturedesk.com

Mar-a-Lago

The discussion about changing the global financial system has also intensified. The USA provides a large sales market, the World Bank and the Monetary Fund grant loans on a rule-based basis and the Fed provides dollar liquidity in an emergency. For some time, however, an idea has been floating around about changing this system, known as the Mar-a-Lago Accord.

This is primarily about a weakening of the US dollar and low US interest rates. Both could be disruptive for the financial system. Possible consequences in a negative scenario include the loss of the US dollar as the most important reserve currency and of US government bonds as the most important safe-haven instrument, as well as a devaluation spiral on the currency side. One immediate effect of this is that US security classes become less attractive.

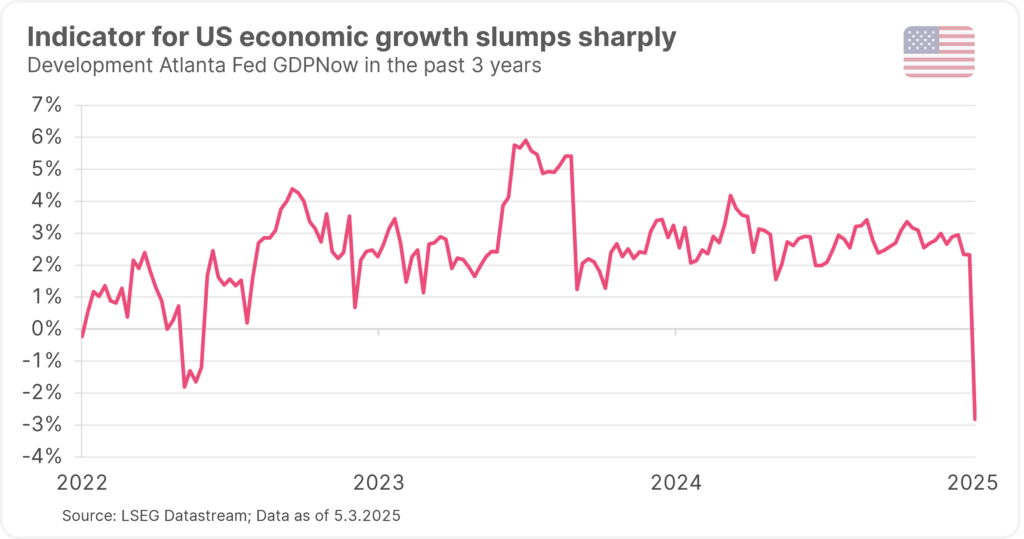

Weak US growth indicators

In addition, economic indicators in the US have been surprisingly weak for several weeks now. A well-known indicator that estimates US economic growth in the current quarter (Atlanta Fed GDPNow) now points to a dramatic slump in real economic growth of minus 2.8% (annualized).

Note: Past performance is not a reliable indicator of future performance.

Private consumption fell in January, the trade deficit was unexpectedly high at USD 153 billion in January and the ISM Purchasing Managers’ Index for the manufacturing sector was weak in February.

It remains to be seen whether the weak growth is the start of a downward trend or a temporary phenomenon. Private consumption was exceptionally strong in the fourth quarter, so a decline in the first quarter would not be surprising. The high level of imports in January could be a pull-forward effect in anticipation of tariff increases. In any case, the growth risks have increased. At the same time, some inflation indicators in the USA are pointing upwards. For example, the indicator for prices paid in the ISM index rose to a high level in February.

Conclusion: basic scenario has cracked

The baseline scenario of “no landing” (trend growth, inflation remains above target, only minor interest rate cuts, yields trending sideways to higher) has cracked in recent days. Growth risks have increased, share prices and yields on US government bonds have fallen.

Interestingly, the opposite is the case with German government bonds – yields have not fallen here. This can probably be attributed to the high upcoming spending on defense and infrastructure. The increased growth risks tend to go hand in hand with increased inflation risks, at least in the USA. The probability of the “stagflationary environment” risk scenario has increased. This environment would mean some headwinds for the financial market.