The day of the decision in the battle for the presidency in the USA, the world’s largest economy, is nearly upon us. The approximately 240 million people eligible to vote in the USA will not only decide on their future president, but also on the distribution of seats in the US Congress. What could follow after the election?

Exciting election campaign is coming to an end

First, the initial situation: The US economy is in fundamentally solid shape. Remarkable growth of around 3% (quarter-on-quarter, annualised), persistently low unemployment, and falling inflation could, under “normal circumstances”, provide a solid basis for the re-election of the incumbent and his party.

However, Joe Biden is no longer standing for re-election due to increasing concerns about his age and a weak performance in the presidential debate at the end of June. Also, public perception of the economy and inflation often does not reflect the positive development of the published statistics. And while Donald Trump is already well known nationwide, the Democratic Party is trying to establish and raise the profile of Joe Biden’s successor (and current Vice President) Kamala Harris in the election campaign.

According to the polls, the race for the presidency between Kamala Harris and Donald Trump is neck-and-neck, especially in the swing states (including Wisconsin, Pennsylvania, Michigan, North Carolina, Georgia, Arizona, and Nevada) that are crucial due to the electoral system and party preferences.

Costly campaign promises

Even though both campaigns have been trying to win the decisive votes in the last few days before the election through public appearances (with personalities from business, music, politics, and sports), an in some cases costly list of campaign promises has accumulated in the course of the election campaign. These include the following items:

- Extension of tax breaks from the Tax Cuts and Jobs Act (passed during Donald Trump’s first term in office; would partially expire in 2025 for individuals and 2028 for businesses)

- Tax exemptions for overtime and tips

- Improvement of social benefits

- Tax cuts for businesses

- Measures to secure the border and increase military spending

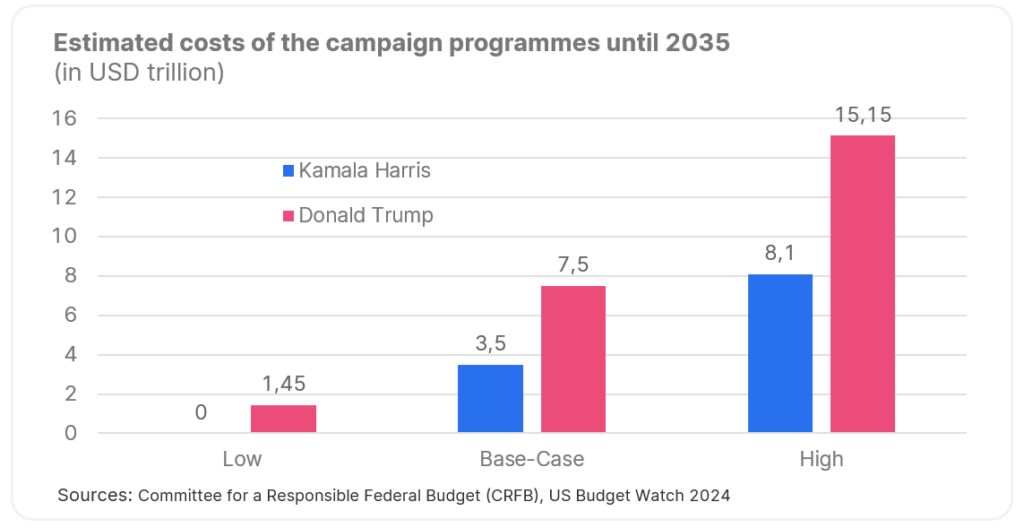

The CRFB (Committee for a Responsible Federal Budget) has scrutinised the plans as presented by the two candidates and estimated the costs for three different scenarios.

The range of estimates is wide and, in the case of Kamala Harris, is determined primarily by the level of social spending. The magnitude of Donald Trump’s plan is affected mainly by the extent of tax breaks (for companies and individuals), as well as military and border security measures. Depending on how they are actually implemented, both candidates’ plans would contribute to an additional increase in US debt until 2035.

The initial financial situation

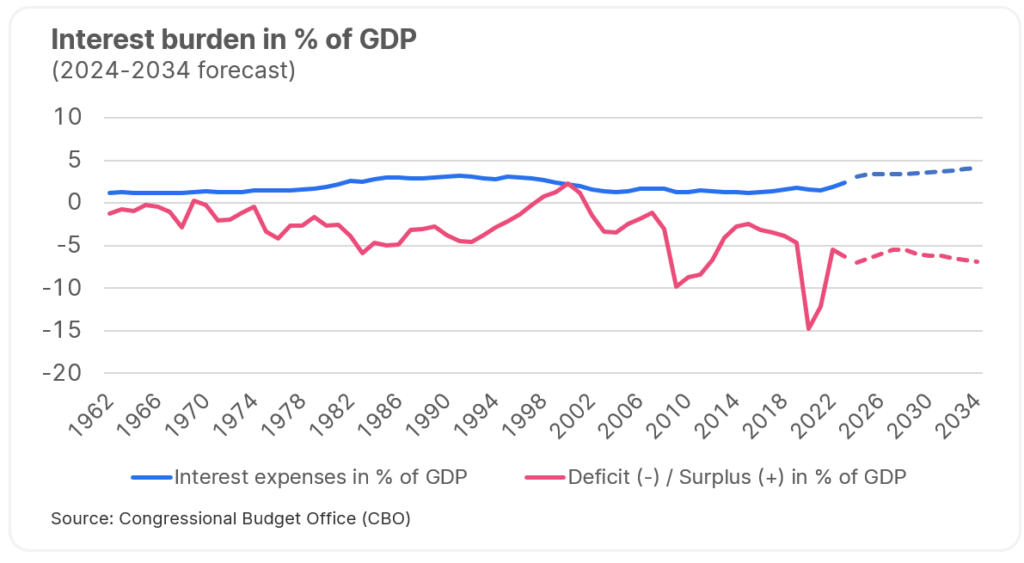

The high budget deficits of recent years and the increased yield levels on the financial markets have caused the interest burden on the US budget to rise sharply to a level of around 3% (or USD 886bn) last year, which means that, for the first time in a while, it slightly exceeded the level of military spending.

Even without the possible additional costs of implementing campaign promises, the latest CBO projections show that interest expenses as a percentage of GDP will continue to rise to around 4% in 2034. For tactical reasons, both parties have refrained from including a plan for consolidating the high budget deficit in their election programmes. The increasingly tense climate between and within the two parties in recent years suggests that medium- to long-term solutions could be a long time coming.

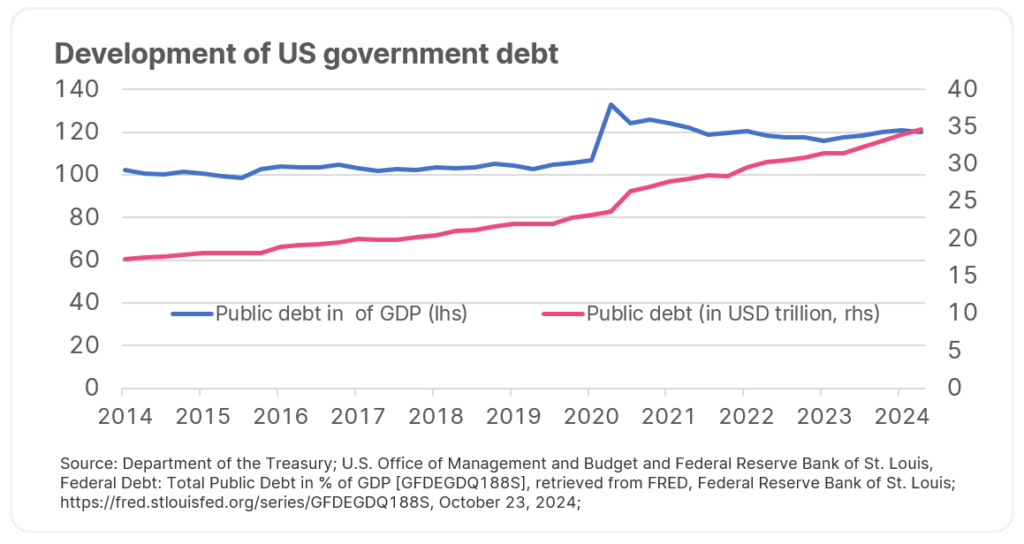

The United States’ total debt at the beginning of April was about USD 34.6 trillion (currently around USD 35.7 trillion), with the publicly held portion (excluding debt between agencies and government entities) amounting to about USD 28.4 trillion or 97.3% of GDP. According to the latest CBO estimate, this publicly held portion could grow by around 25% to over 122% over the next ten years, and this is before taking into account the potential costs of implementing election promises. In the absence of appropriate compensatory financing, this would further strengthen the already expansive fiscal policy and could additionally increase the debt significantly.

But in addition to the US president, members of Congress (the House of Representatives in its entirety, about a third of the Senate) are also standing for re-election at the same time. The forecasts for the election of Senate members currently expect that the narrow majority of the Democratic Party could switch to the Republican Party with the votes of the independent candidates. The balance of power in the House of Representatives after the election is as difficult to predict as the outcome of the presidential election, with both parties having roughly an equal chance of winning a majority in this chamber.

Outlook

The actual potential for keeping the election promises will depend, among other things, on the outcome of the congressional elections and the majorities required for decision-making. The effects of a further expansion of debt and the resulting higher issue volume of US Treasury bonds will depend, among other things, on the extent to which investors are willing to buy, on the reaction of the Federal Reserve to possible interactions with the labour market and inflation, and on the time frame for implementation.

Also, the election campaign has addressed a number of areas with potential for reactions on the financial markets (tariffs and NATO, among others). It remains to be seen whether and to what extent the statements in the areas of global, economic, and military cooperation can be realised and how the financial markets will react to them.

However, domestic policy issues are on the agenda in a more immediate fashion. After no agreement could be reached in the annual budget negotiations in Congress in September, bridge finance was approved until 20 December 2024. If no agreement is reached by then, there is a risk of a government shutdown before Christmas. The debt ceiling, which is currently suspended until early 2025, must also be renegotiated, otherwise it will come back into force. It remains to be seen how the majorities in the two chambers of Congress will be distributed after the election.

The coming weeks and months will therefore show in particular how much willingness to compromise will be necessary or available in order to solve the problems at hand. The eventful recent past has also indicated that with narrow majorities, the inhomogeneity within the two parties cannot be ignored.