Last week, volatility returned to the stock markets. The US leading index fell by more than 3.3 per cent. The European markets fell by 1.2 per cent (source: Refinitiv Datastream). The reason for the losses was the tension between hopes for a less restrictive US Federal Reserve and actual inflation and economic data. Producer prices in the US, released on Friday, rose 7.4 per cent year-on-year, more than analysts had expected. The previous day, signs of a slowdown in the labour market had fuelled hopes for a less restrictive monetary policy. The number of applications for unemployment benefits in the USA rose for the third time in a row by 62,000 to 1.7 million – the highest level since the beginning of February.

This week, the financial markets are once again in for an exciting ride: the US Federal Reserve will hold its last meeting of the year on Wednesday. Against the backdrop of the mixed economic data described earlier, we expect the Fed to reduce the pace of its rate hikes from the previous steps of 75 basis points (100 basis points = 1 per cent, note) to 50 basis points. We do not believe that it will be able to send a clear signal of the end of the rate hike cycle as early as December. This will be followed by the European Central Bank (ECB) meeting on Thursday: most economists expect a hike of another 50 basis points. The ECB also wants to decide on important key principles for reducing its balance sheet, which has been swollen by years of bond purchases. ECB President Christine Lagarde had held out the prospect of a measured and predictable reduction in bond holdings.

Note: Past performance is not a reliable indicator for future performance.

Robust companies

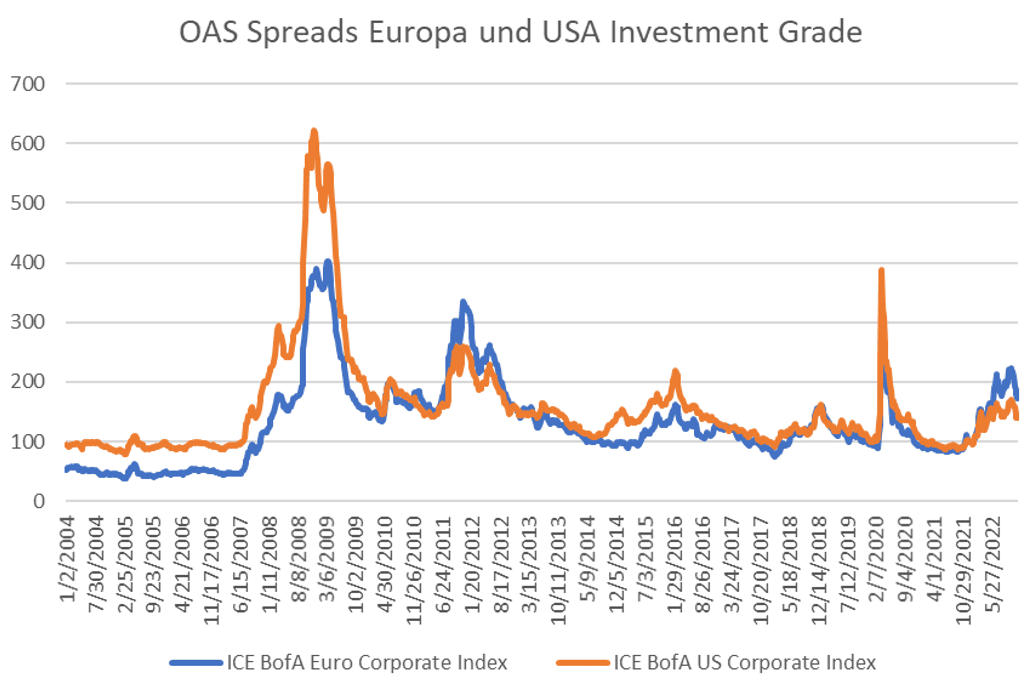

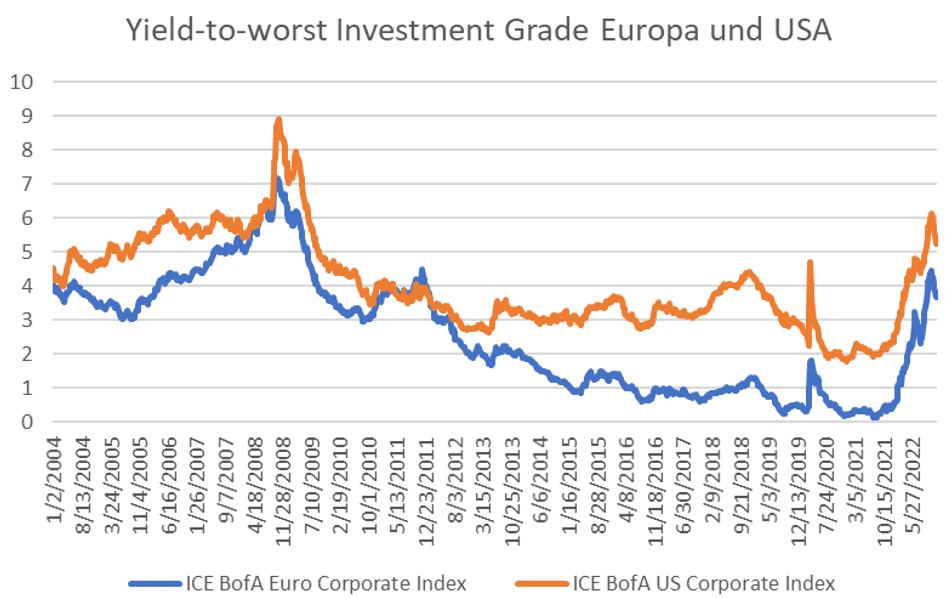

In general, we will keep the risk appetite of our portfolios slightly below the strategic risk budget. The risks of recession have increased, as we have often described. In our opinion, this is already partly reflected in the market prices of some asset classes. This is especially true in the segment of corporate bonds with an investment grade credit rating where we see yield levels averaging over 5 per cent in the US (source: Bloomberg). Even in the event of a global recession next year, we expect the high-quality companies in the investment grade segment to weather it well.

Correction potential for commodities

Energy and industrial commodities are moving in an environment of physical scarcity. OPEC’s policy continues to supporte for example crude oil. Nevertheless, we see a higher correction potential in the event of a recession than for other asset classes. The situation is similar for industrial metals. The necessary and government-supported expansion of renewable energy has a positive effect on the one hand. However, market and valuation aspects also speak against this segment.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.