The path towards a clearly fragmented global economy is continuing. Recently, the increase in tariffs on Chinese electric cars in the USA and the European Union has been particularly noticeable. Who are the winners? Who are the losers? Generally speaking, all sides lose in a trade conflict.

What is protectionism?

Protectionism (in the narrower sense) describes an economic policy that aims to restrict imports from other countries through tariffs, quotas and other measures. The aim of such measures is to protect domestic industry from foreign competition. On closer inspection, this definition falls short: in fact, it also involves measures to restrict certain exports (e.g. last-generation semiconductors) and investments in a country that is not a friend or to reduce the number of sites in that country (friendshoring, nearshoring). There are two reasons for this: Firstly, to strengthen national security and secondly, to prevent a country (such as China) from developing (containment). In the following, the term protectionism (in the broader sense) will apply to all these measures. The effects are a fragmentation of the global economy, which could end in deglobalization.

Driving forces

The two main drivers of this trend are the rise of nationalist populism in many countries and the rise of China as a major trading power. China even topped the list of top exporting nations in 2023 with around 3.4 billion US dollars. On the side of increasing nationalism in Western countries, the USA is particularly relevant. The Republican Party’s slogan “Make America Great Again” stands for the reindustrialization of the USA, among other things. Recent events (attempted assassination of the presidential candidate) have further increased the likelihood of Donald Trump winning the election. In Europe, too, the EU parliamentary elections and the elections to the French parliament have tended to weaken the integrative forces of the EU.

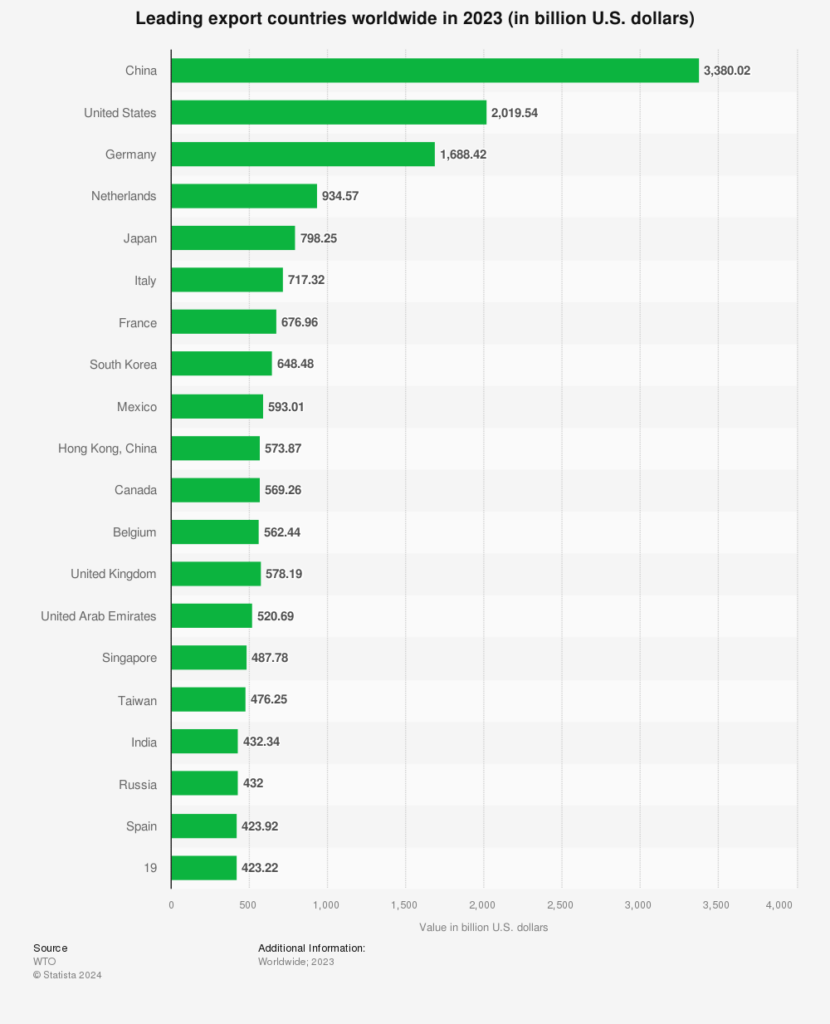

China remains world export champion in 2023. China exported goods worth around USD 3.38 trillion, making it the world’s largest export country, far ahead of the USA (USD 2.02 trillion) and Germany (USD 1.69 trillion). The statistics show the 20 largest exporting countries worldwide in 2023.

The arguments of supporters and opponents

Proponents of higher tariffs put forward the following arguments:

- The protectionist measures are intended to compensate for an unfair competitive situation. In the specific case of Chinese electric cars, these are allegedly unjustified subsidies on the Chinese side.

- In addition, protectionist measures can exert pressure on the exporting country to align its environmental and ethical standards (ESG and human rights) with those of the importing country. This is intended to achieve a level playing field (fair conditions).

- Another positive incentive is the relocation of production from the exporting country (China) to the importing country (EU).

- Domestic companies are protected from foreign competition. This prevents job losses.

- The “protection from foreign competition” argument applies increasingly to key industries (technology, energy) and national security (defense). The economic policy measures are export and investment restrictions (note: chips that can be used for military purposes) and friendshoring.

- The time during the coronavirus pandemic has shown that global supply chains are vulnerable. In response, measures for nearshoring are being implemented. These are intended to reduce global dependencies.

- Traditionally, higher tariffs are intended to reduce a trade deficit. In 2023, the EU’s trade deficit with China amounted to 291 billion euros.

- The demise of the solar industry in Europe is often cited as an argument for protective measures (protection of industries that are at the beginning of their development).

- For the sake of completeness, nationalist parties cite the preservation of national identity.

Opponents of higher tariffs cite the following arguments:

- Higher tariffs have a similar effect to raising taxes. The question is whether this will reduce the profit margins of exporting companies or make the prices of imported goods more expensive. This depends above all on the pricing power of the exporting companies. It could be true that the motives of Chinese companies are not only geared towards short-term profit maximization, but also towards the long-term expansion of market shares. The empirical findings tend to point to an increase in the price of imported goods.

- Raising import tariffs could result in retaliatory measures. For example, the sales market for foreign companies could be restricted (e.g. for German car manufacturers in China). In addition, the export of important goods (rare earths) abroad could be more strictly regulated. Or regulations could be introduced to make it more difficult for foreign companies in China to do business. The last argument has lost some of its importance because foreign investment in China is declining and China wants to increase it.

- A protectionist policy reduces competitive forces (market distortion). The risk lies in an inefficient allocation of resources. Established industries with low innovative strength are protected. The incentive to invest in new technologies remains too low.

- The criteria used to determine the sectors worthy of protection and the key industries are not objective, but are subject to political influences.

- In the case of electric cars, the cheaper Chinese models could accelerate decarbonization.

- Economic theory would suggest that the currency of the country raising tariffs would appreciate. However, this would negate the purpose of the higher tariffs. In order to attempt reindustrialization, a weakening of one’s own currency is necessary. Imports should become more expensive, exports cheaper. For this to succeed, a looser monetary policy compared to other countries is necessary. However, this would have inflationary consequences. The US dollar in particular is currently expensive by historical standards (in real effective terms). However, the real effective valuation of the euro is also slightly above average. This observation shows once again how dangerous a trade conflict can become. The increase in tariffs and counter-tariffs could also lead to a spiral of currency devaluation.

- The increased uncertainty generated by a trade conflict could dampen companies’ willingness to take risks. Corporate investments could be held back.

Since the global financial crisis in 2007, the number of protectionist trade policy measures in the G20 countries has increased. In all G20 countries, more discriminatory measures than liberalizing measures came into force in the period from November 2008 to 2021 (as of October). The USA (7,376) and China (5,891) had a particularly high number of discriminatory measures.

Summary

Targeted tariff increases can protect certain domestic industries from cheap foreign export goods. An intervention in free trade makes sense if not all countries pursue the same standards. However, domestic prices for the goods concerned are likely to rise. This is offset by the continued existence of domestic industry. The net effect could therefore be positive. There are two main risks with protectionist measures: firstly, they may not be targeted and well-considered. Industries that are not worth protecting could be subsidized. Secondly, a trade conflict could escalate. There is a risk of a spiral of tariffs, counter-tariffs and other retaliatory measures, such as a spiral of currency devaluation. This uncertainty could have a negative impact on the investment climate.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.