Within two years, the global economy has been confronted by two negative events or, indeed, shocks: the Covid pandemic was the first one, having not only killed six million people globally at this point, but having also caused an unprecedented slump in the global economy and the subsequent recovery. The second one, i.e. the invasion of Ukraine by Russia, is of a geopolitical nature and has triggered a commodity price shock. The effects are in both cases stagflationary, because without them, the GDP would be higher and inflation lower.

Recovery and inflation before the invasion

With the Omicron variant on the decline, the cyclical economic indicators suggested another acceleration of economic growth in February (after the weakening in December and January) and confirmed the base case scenario of “continued recovery”. At the same time, inflation reports suggest persistently high inflation pressure. In January, consumer price inflation amounted to 7.8% y/y in January for the OECD region. On the labour market, the unemployment rates in the USA (February: 3.8%) and in the Eurozone (January: 6.8%) suggest a tightening. This in turn exerts increasing pressure towards rising wage growth.

Cold war and strengthened alliances

The invasion of Ukraine by Russia constitutes a far-reaching event on numerous levels, as it touches on fundamental risks: peace (the risk of a confrontation with a NATO state), energy security (the risk of supply shortfalls), and food security (the risk of food shortages, especially in developing countries). Maybe the current situation also highlights the value of democracy and the rule of law. This also affects the level of sustainability criteria. Indeed, ESG as a concept does is not only fight climate change but is also about the question of how sustainability and non-democratic states are inherently at odds with each other.

While the West is not intervening on the military front, the use of financial weapons (sanctions) and the supply of arms to Ukraine mean a new cold war. The relations of the West with Russia are sustainably damaged. Due to the sanctions, the states that do not consider themselves as belonging to the West also feel a rising motivation to emancipate themselves from the dependence on the US dollar and other reserve currencies. The likelihood of an Asian currency block forming around the renminbi has increased. In addition to the geostrategic fortification of China, the supranational organisations NATO and EU have also emerged stronger from the situation. This implies among other things that the approved NATO defence budget is actually fulfilled, that a possible expansion of NATO has become more probable, and that the exit of another EU state and/or the break-up of the Eurozone has become less likely. Further emergency packages would be passed if need be. In addition, the motivation to invest more in energy security and in defence (also outside of NATO) has increased as well. The trend of the state and private investment quotas will probably exceed the original scenario in the coming years, as will the budget deficits.

Sanctions dealing a hard blow to Russian economy

The West has responded with a comprehensive range of sanctions that should deal a strong blow to the Russian economy. This is what it looks like, as they are enforcing an even bigger degree of self-sufficiency. Some Russian banks have been excluded from SWIFT, the cooperative society providing services related to the execution of financial transactions and payments between banks worldwide. Also, more and more assets held by Russian citizens (oligarchs) abroad are being frozen. A large part of the foreign exchange reserves of the Russian central bank has also been frozen. In addition, foreign companies have suspended or indeed ended their relations with Russia. This has led to a slump in foreign trade and in the GDP (current working assumption: -10% this year) as well as to severely compromised supply chains. A credit crunch is also looming. S&P has downgraded the rating of Russia to CCC-. The exchange rate of the rouble relative to the US dollar has fallen off a cliff. The pressure on the Russian government has increased, because it cannot ensure stability and welfare any longer.

2012-2022, as of 16 March, 2022, USDRUB spot rate

The Russian population will be feeling the sanctions closely. History suggests that autocratic regimes are unlikely to change because of this sort of situation, let alone are removed due to it.

Increase in commodity prices

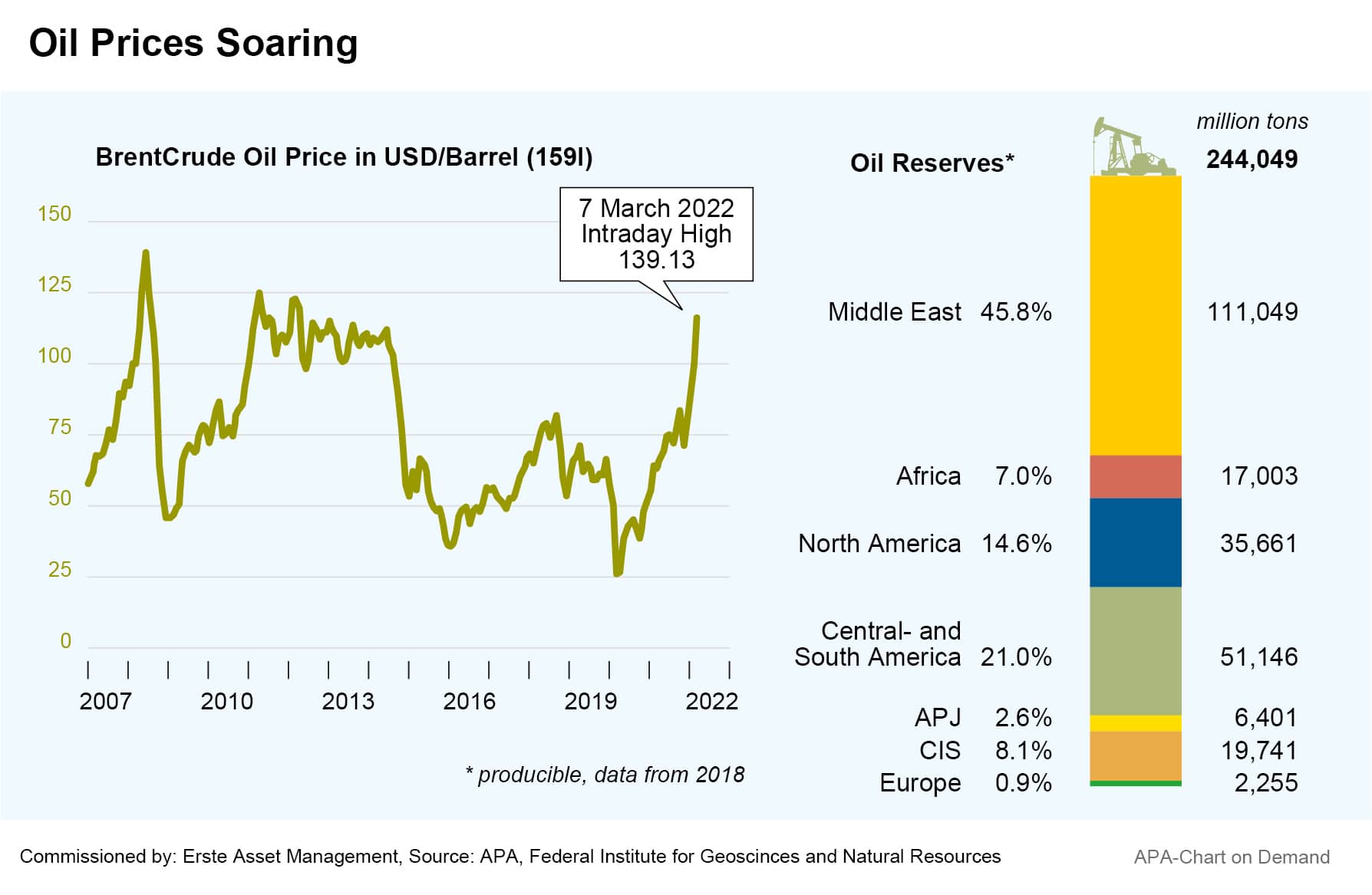

While Russia and Ukraine account for only 2% of global GDP, their main (and significant) influence is in the area of the production and export of energy, industrial metals, food, and fertilisers and of course in the large arsenal of nuclear arms held by Russia. The longer the war in Ukraine lasts, the bigger the influence of the commodity markets on the world (economy) will become. For example, Ukraine and Russia account for a joint 25% of the globally traded wheat and some 14% of the globally traded corn. Russia accounts for 13% of global oil production, for 17% of natural gas, for 11% of wheat, and for even 44% of palladium.

The increased likelihood of possible production downtimes (wheat), trading halts (Black Sea ports), further import limits imposed by the West or export limits by Russia, and the self-restriction by Western companies (insurance companies and banks) have led to massive commodity price increases (energy, metal, food).

The longer the war lasts, the more brutal it will become and the more the pressure on the West will rise to step up its sanctions and cut ties with Russia. The USA has imposed an import ban on oil and gas from Russia, and the UK has banned oil imports from Russia until the end of the year. The EU wants to cut down drastically on gas imports this year (by about two thirds). By 2027, the EU does not want to import any oil or gas from Russia anymore. Around the middle of May, the EU Commission wants to present an energy plan (RepPowerEU Plan) on the basis of which these targets are to be reached. In addition, we can see a certain degree of self-restriction by Western companies (banks, insurance companies, transport companies, trading companies) due to legal and reputational risks.

The development of the commodity prices from here on out will mainly depend on the kind of sanctions imposed by the West and possible counter-sanctions from Russia. Both hinge on the course of the war in Ukraine, among other things.

High inflation and dampened recovery

Even without any actual loss in production volumes, the war in Ukraine represents the second stagflationary shock within two years. The actual impact on real economic growth and inflation comes with a great deal of uncertainty. Both the extent and the duration of the shock as well as the response by the various countries and the resulting second-round effects are uncertain.

The massive price increases of commodities will keep inflation rates high in the coming months (globally at about 6% p.a.). In the base case scenario, global inflation could exceed the pre-Ukraine scenario this year by 1 percentage point (Q4 2022: 5% p.a.). The EMU is more severely affected (+1.5 percentage points to 4% p.a.). The risks are on the upside. The high inflation dampens purchase power and reduces consumer sentiment. Real global GDP growth is likely to fall short of the pre-Ukraine scenario by about 1 percentage point (Q4 2022: 3% p.a.). Here, too, the EMU is more severely affected (-2 percentage points to 2.5% p.a.).The risks are on the downside. The risk of a recession would increase especially in case of supply interruptions.

Dilemma for central banks

The central banks are confronted with a dilemma. Inflation rates are surprisingly high, driven by commodity prices. In some countries (USA), we can already see spill-over effects from the costs driven by the pandemic to other price components. Companies will try to pass on higher commodity costs. Employees will demand higher wages. Since the unemployment rates are already low and the base case scenario is that of a continued recovery, the spill-over to other price components has become more likely.

At the same time, the commodity price shock hampers economic growth, recessionary risks have increased, and the uncertainty on the financial markets has increased.

Interest rate reversal initiated

The central banks can do little to influence the development of inflation this year. The goal is to contain the second-round effects and to keep inflation expectations as stable as possible. While the Ukraine crisis is dampening the exit from the ultra-expansive monetary stance, it is not preventing it. The US Fed initiated the cycle of rising interest rates on 16 March by increasing the Fed funds rate from 0.25% to 0.5% (upper band for the effective key-lending rate). In its projections, the Fed has signalled a Fed funds rate of 2.8% by the end of 2023.

Even the ECB has announced the exit from its ultra-expansive monetary policy, albeit at a very slow pace. The net purchases of bonds (APP) will come to an end in Q3 if the medium-term inflation outlook does not weaken and the financial context does not deteriorate. This means the path has been cleared for a rate increase in the second half.

The environment supports the scenario of inflation being elevated also in the longer term:

- Even before the Ukraine crisis, inflation was elevated and was so for a longer period than expected

- The tendency towards deglobalisation is being reinforced: after the US-China conflict and the pandemic (supply chain), the sanctions against Russia followed suit. All that means higher costs.

- Companies will try to pass on a part of the higher costs to their customers (cost-push inflation).

- Higher expenses and investments in energy security and defence will support the trend growth of the economy, should result in high budget deficits, and could have an inflationary effect.

- The likely subsidisation of energy consumption would lead to a drastic increase in budget deficits.

- The central banks in the developed economies currently cannot react to the elevated inflation pressure with particularly restrictive measures, as the dampening effect on growth would be excessive. However, this implies a higher interest rate and inflation level in the medium term.

Additional uncertainty driving up risk premiums on the capital markets

For the markets, the environment remains strained, at least in the short run:

- The development of the commodity prices in the foreseeable future will be crucial. In particular, three developments could cause commodity prices to fall:

- The West can credibly convey that it does not want to sanction commodities any longer

- Prospect of successful peace negotiations

- Alternative sources of supply are being found, at least for oil

- Recession (of course not beneficial to high-opportunity investments)

- The central banks cannot pursue a more expansive monetary policy to support the markets as inflation is high. Also, if inflation rates do not fall as expected, central banks will increase key-lending rates more significantly than expected.

- The valuations already reflect a moderately stagflationary environment (implied in the commodity prices), but no deterioration (further commodity price shock, supply interruptions). On the upside, if the worries turn out not to be (fully) substantiated, this would support the markets.

Legal note:

Prognoses are no reliable indicator for future performance.