At the beginning of the new year, the economic indicators published are supporting the “no landing” scenario. The key points for this scenario are:

- Economic growth at trend

- A halt to the decline in inflation

- Only few key-lending rate cuts

- Government bond yields moving sideways or moderately higher.

However, this positive environment for risky asset classes such as equities is being clouded by a number of uncertainties, in particular the design of the new US administration’s policy and the rise in government bond yields.

Trend growth

The growth of the gross domestic product adjusted for inflation (real GDP) is estimated to have been 1.7% for the developed market economies in the past year; the number is expected to decline to 1.5% in 2025. The monthly leading indicators confirm the favourable growth environment. The Global Purchasing Managers’ Index (PMI) has risen (from 52.4 in November to 52.6 in December), as has the OECD leading indicator for the G20 (the most important industrialised and emerging market economies).

Increasing growth differential

At the same time, there are still major differences in economic growth between individual countries, with US policy (tariff increases) potentially even leading to greater differences. In the Eurozone, economic confidence fell in December (European Commission Economic Sentiment index), but the PMI rose slightly in December, albeit remaining at a low level (49.6).

On the upside, we have noticed an improvement in lending volume. After almost two years of stagnation, the outstanding volume of loans in the Eurozone rose in October and November. Interpretation: economic growth in the Eurozone remains low, but the low growth looks more sustainable (2024 and 2025: 0.8%).

US boom

By contrast, the US economy is booming. After a 2.8% increase in GDP last year, only a slight slowdown to 2.4% is expected for this year. The latest data have confirmed the assessment of strong growth. In December, the purchasing managers’ index rose to a high 55.4, and the labour market indicators were strong (newly created non-farm payrolls: 256,000, unemployment rate: 4.1%). In the coming days, the focus will be on the publication of retail sales and industrial production.

Halt to declining inflation

Consumer price inflation in the G7 (the seven major industrialised countries) was 2.6% year-on-year in November. Inflation is estimated to have been 2.5% in the fourth quarter of 2024. According to the flash estimate, consumer prices in the Eurozone rose by 2.4% year-on-year in December. Excluding the food and energy components (core rate), the price change over the year was 2.7%. Inflation in the services sector remained high at 4% per annum. However, in the fourth quarter of 2024, inflation in the services sector fell to an annualised 2.8%.

The low economic growth in the Eurozone suggests that inflation will continue to fall towards 2%. By contrast, the prospect of a fall in inflation in the USA has decreased. This is because the economy is booming, and the future US policy could provide an additional boost to prices.

Less scope for interest rate cuts

In this environment, the scope for many central banks to cut interest rates is limited. In its base-case scenario, the ECB lowers its key-lending rate by 1.25 percentage points from the current level of 3.0%. For the US Federal Reserve, however, the question arises as to why interest rates should be cut at all when economic growth is above potential and inflation is above target, and upside risks to inflation have increased (forecast: 4% by the end of 2025, down from 4.5%).

The minutes of the last meeting of the Fed Open Market Committee (FOMC) in December still show a tendency towards interest rate cuts, but at the same time, indications of a more cautious attitude were emerging. Since September, the Fed funds rate has been cut rapidly by one percentage point (from 5.5% to 4.5%). The signals at least point to a slowdown. The market is not pricing in another rate cut until September.

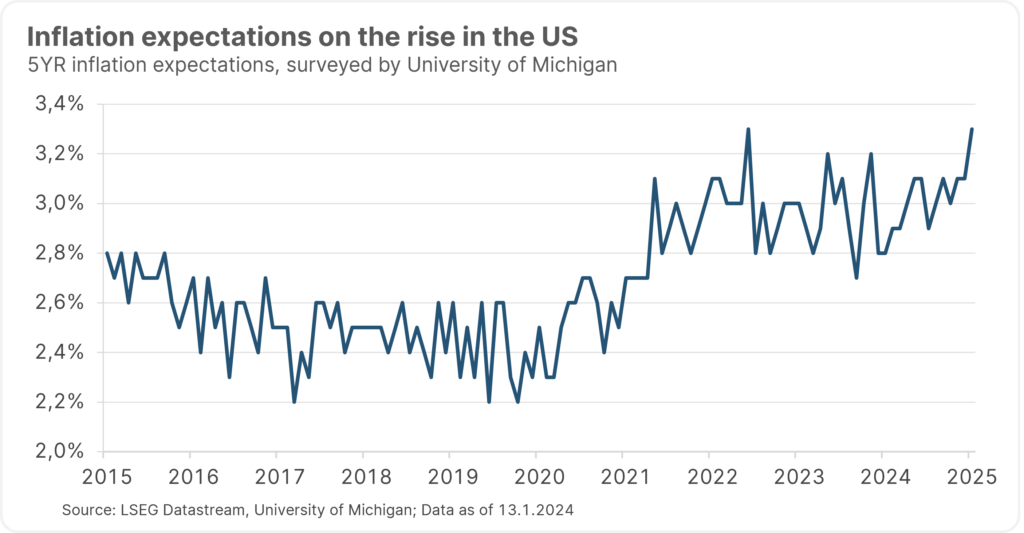

Inflation expectations have increased

It is an important prerequisite for interest rate cuts that long-term inflation expectations remain stable and low. On the data front, there have been two disappointments in this regard. In the Eurozone, the ECB reported that 3Y consumer inflation expectations had increased from 2.1% to 2.4% (November survey). The indicator showed a falling trend between October 2022 and October 2024. In the USA, long-term (5Y to 10Y) inflation expectations of consumers rose from 3.0% (December figure) to 3.3% (preliminary January figure) according to the University of Michigan. This high figure was last reached in 2008 (oil price shock).

Market risk: if long-term inflation expectations were to rise sustainably, market expectations of key-lending rate cuts would disappear. Even the necessity of key-lending rate hikes would probably be up for discussion again.

Yield increases

On the bond market, the rise in yields (price declines) of government bonds has been striking in the year to date. The most important reference value, the 10Y yield of US Treasury bonds, has risen from 4.57% to 4.76%. The inflation premium and the yield adjusted for inflation contributed to this in almost equal measure. The real yield rose from 2.22% to 2.31%. This can be explained by the strong economic growth, falling expectations of key-lending rate cuts, and the prospect of a persistently high budget deficit (7% of GDP). At the same time, the inflation premium rose from 2.34% to 2.44%.

Please note: past performance is no reliable indicator of future value developments.

Since the last low in mid-September, the rise in the yield on the 10Y Treasury bond has been more than 2 percentage points. It is probably no coincidence that, at the same time as key-lending rates started to fall (so far from 5.5% to 4.5%), the 10Y yield is no longer below but above the 2Y yield, with the difference between 10Y and 2Y widening (currently 0.38 percentage points). For around two years, from summer 2022 to summer 2024, the steepness of the curve (10Y minus 2Y yield) was negative. The normalisation of the steepness of the curve is not yet a cause for concern. The spread for holding long-term bonds should theoretically be positive (and not negative).

Conclusion

Generally speaking, the “no-landing” scenario represents a good environment for risky asset classes. Yield increases and fading expectations of key-lending rate cuts, caused by strong growth indicators, constitute only a temporary headwind. However, sharp yield increases driven by rising inflation expectations would have the power to seriously damage the positive market sentiment. The publication of US consumer price inflation for the month of December is therefore in the spotlight this week.