After several years of boom in the luxury goods industry, growth came to a standstill for the time being last year. Growth in the sector averaged 5% per year between 2019 and 2023, according to a study published in January by management consultants McKinsey. By comparison, global gross domestic product (GDP) grew by around 3% per year in the same period.

Growing customer demand and purchasing power coupled with price increases were reflected in higher sales and margins during this period. However, sales fell slightly again in 2024. According to forecasts by the consulting firm Bain, spending on luxury goods is likely to have fallen by 1 to 3 percent worldwide in the past year.

The industry suffered in particular from weak demand in the important sales market of China. Nevertheless, some industry giants were able to surprise positively with their latest earnings figures. The companies were able to partially compensate for the weakness in China with strong sales in other regions and are now hoping that the important Chinese demand will also pick up again. Industry experts also believe that the long-term growth path remains intact.

Note: Past performance is not a reliable indicator of future performance.

Economic downturn in the important sales market of China

China is the most important growth market for the luxury industry. According to McKinsey’s industry study, sales of luxury goods in the country grew by an average of 18% per year between 2019 and 2023, significantly more than in any other region. According to McKinsey’s calculations, 40% of industry growth in this period is attributable to China alone.

Recently, however, demand for luxury products in China has stuttered. The economic downturn, a real estate crisis and high youth unemployment in the world’s second largest economy significantly dampened consumer appetite for luxury products. According to an analysis carried out by management consultants Bain last year, the economic uncertainty had a particularly negative impact on middle-class buyers.

New modesty among the Chinese population

According to Bain, there was also a change in attitude towards luxury goods: rich Chinese who could still afford luxury products now want to avoid showing off and no longer flaunt their wealth in public. “For the first time in history, we are experiencing so-called luxury shame in China,” said Bain expert Federica Levato. In the midst of the crisis, wealthy Chinese now prefer to opt for more subtle and discreet fashion.

The island of Hainan is considered a Chinese shopping paradise – but sales there have recently slumped. The picture shows the skyline of the city of Sanya on Hainan. Image source: unsplash.com

The new reluctance to spend on luxury goods also caused sales in Hainan, an important Chinese shopping paradise for the industry, to slump in the previous year. Spending on duty-free goods in the island province fell by 29.3 percent year-on-year to 30.94 billion yuan, or the equivalent of 4.1 billion euros, in 2024.

The slump in sales is also a setback for foreign luxury brands. Global luxury companies such as LVMH and Kering have set up shop on the island. They had expected a boom after the coronavirus pandemic and the end of the strict lockdowns. In particular, global cosmetics companies such as L’Oreal and Estee Lauder had high hopes for Hainan. Cosmetics products accounted for more than 40 percent of duty-free sales there in 2023.

Note: The companies listed in this article have been selected as examples and do not constitute an investment recommendation.

Some of Europe’s luxury goods giants performed better than expected in 2024

However, some of the major luxury goods groups performed better than expected in 2024 despite the slump in China. The French Hermes Group, for example, bucked the industry trend at the end of 2024 with a surprisingly large leap in sales. The handbag manufacturer reported a currency-adjusted increase in turnover of almost 18% to EUR 4 billion for its fourth quarter. Analysts had expected significantly lower growth. Net profit grew by 6.7 percent to 4.6 billion euros. The figures were received euphorically on the stock market.

The Hermes share even rose to a new record high after the figures were announced. In a one-year comparison, it has recently gained around 17 percent. Over a ten-year period, the Hermes share price has even increased tenfold. The company was most recently worth 284 billion euros on the stock exchange, putting it in second place behind LVMH in an industry comparison.

The figures of Swiss watch manufacturer Richemont and British Burberry also came as a positive surprise. Both companies were able to compensate for the slump in China with good business in the USA. Richemont, known for its Cartier jewelry and watches, posted surprisingly strong sales growth of 10 percent to a record 6.2 billion euros in the important Christmas quarter. The most important growth driver for the Swiss company was America, but Richemont also grew in Europe and Japan. In Greater China, however, sales shrank by 18 percent.

British luxury clothing manufacturer Burberry also got off surprisingly lightly in the Christmas quarter thanks to higher demand in the USA. Although retail sales shrank by 4 percent to 659 million pounds sterling or the equivalent of 780 million euros in the third quarter, experts had expected a much sharper decline of almost 13 percent. The increased demand in America was unexpected. Despite declines, things also went better than expected in China.

LVMH and Kering disappoint with annual results

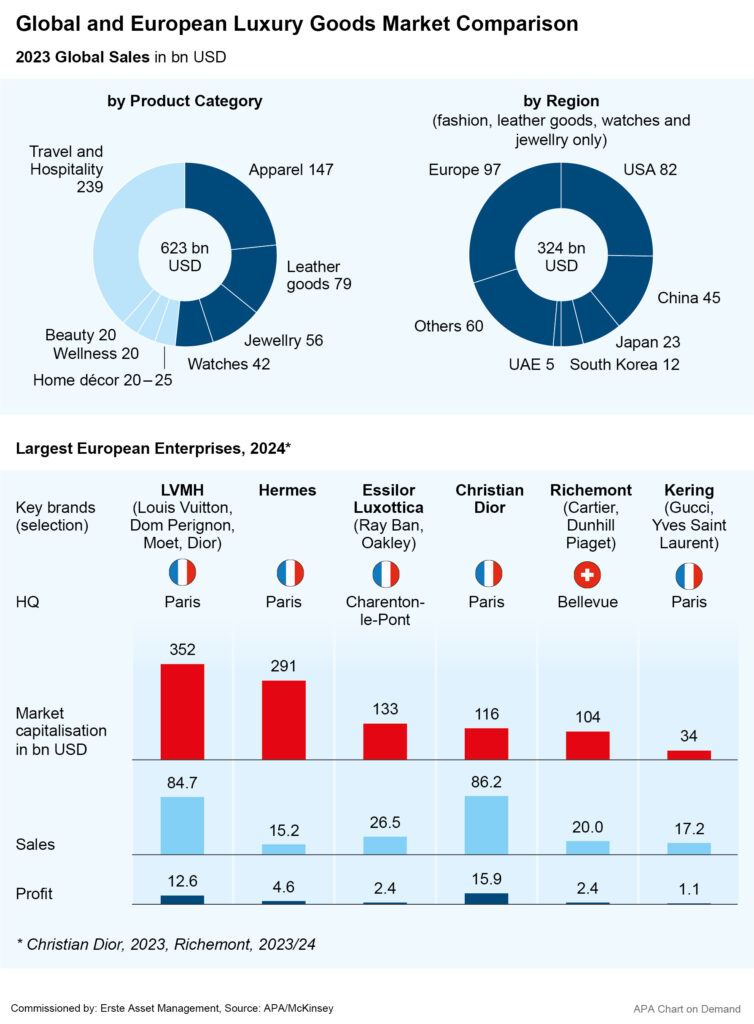

The figures for French industry giant LVMH (Louis Vuitton Moët Hennessy) were mixed. Although the group surprisingly achieved a small increase in turnover of 1 percent to 84.7 billion euros in the past year, operating profit fell more sharply than expected by 14 percent to 19.6 billion euros. At the bottom line, net profit fell by 17 percent to 12.6 billion euros. In terms of market capitalization of 350 billion, LVMH is the most valuable company among the European luxury goods groups.

The results of the luxury group Kering have been poorly received on the stock markets. The luxury goods group’s turnover fell by 12 percent to 17.2 billion euros in 2024. Sales of the Kering brand Gucci fell even more sharply by 23 percent. Despite the company’s cost-cutting efforts, the operating result fell by almost half to 2.6 billion euros. According to the Kering management, however, there has recently been at least a slight improvement in demand in China and North America.

Industry experts expect recovery to begin

Industry experts from consulting firms Bain and McKinsey also see the industry at a turning point before a coming recovery. According to McKinsey’s forecasts, the global luxury goods market is expected to grow by an average of 2 to 4 percent again between 2025 and 2027. The consultancy firm attributes particular growth potential to leather goods and jewelry, expecting these two product groups to grow by a combined 4 to 6 percent annually during this period.

Our colleagues at Bain, who define the concept of luxury goods more broadly, have identified a trend away from luxury goods towards experience-oriented luxury products such as exclusive travel or, in the case of wealthy customers, works of art and exclusive sports cars.

USA could become a new growth driver

Finally, the industry’s hopes are also pinned on the anticipated recovery of the Chinese market. According to McKinsey forecasts, China’s luxury goods market is likely to grow again by 3 to 5 percent in the period from 2025 to 2027. Government measures to stimulate the economy in particular could kick-start a recovery.

However, the McKinsey experts see even greater potential of 4 to 6 percent for the US market. This could take over China’s role as the industry’s growth driver. A decline in inflation and greater disposable income should have a positive impact on demand for luxury goods among middle-income consumers. Added to this is the growing number of wealthy buyers. However, the European luxury goods giants must be prepared for the possible threat of punitive tariffs imposed by the new US President Donald Trump..

Luxury groups strongly represented in leading European index

The luxury sector is a very important economic factor for the European stock market. The luxury companies LVMH, Kering and Hermes are among the companies in the Euro-Stoxx-50, the leading index in the eurozone. Overall, the index comprises the 50 largest and most important listed companies in the eurozone.

Investors looking to invest in the luxury sector will therefore find it difficult to avoid the European stock market. In any case, a broadly diversified investment that includes as many other sectors as possible in addition to the luxury sector makes sense. For example, the ERSTE RESPONSIBLE STOCK EUROPE equity fund could be worth a look. The three companies mentioned, LVMH, Kering and Hermes, are also part of the portfolio there. The fund has already gained x% so far this year. In general, European equities have outperformed US equities so far in 2025 – a trend from which luxury stocks could possibly also benefit in the future.

Broadly diversified investment in shares of European companies with ERSTE RESPONSIBLE STOCK EUROPE 👉 Invest now

Note: Please note that investing in securities involves risks as well as opportunities. Where portfolio positioning of funds is disclosed in this document, this is based on market developments at the time the document was prepared. As part of active management, the stated portfolio positioning may change at any time.

Risk notes ERSTE RESPONSIBLE STOCK EUROPE

The fund employs an active investment policy and is not oriented towards a benchmark. The assets are selected on a discretionary basis and the scope of discretion of the management company is not limited.

For further information on the sustainable focus of ERSTE RESPONSIBLE STOCK EUROPE as well as on the disclosures in accordance with the Disclosure Regulation (Regulation (EU) 2019/2088) and the Taxonomy Regulation (Regulation (EU) 2020/852), please refer to the current Prospectus, section 12 and the Annex “Sustainability Principles”. In deciding to invest in ERSTE RESPONSIBLE STOCK EUROPE, consideration should be given to any characteristics or objectives of the ERSTE RESPONSIBLE STOCK EUROPE as described in the Fund Documents.