The International Monetary Fund/World Bank Group Spring Meetings 2024 have recently taken place in Washington, D.C., and I participated on behalf of Erste Asset Management. Thanks to a wide range of high-ranking representatives from various emerging market (EM) countries’ governments and central banks, financial institutions, think tanks and academics, the meetings offer highly valuable insights into current and upcoming global concerns in both economics and politics. Moreover, the conference serves as a platform for investors covering EMs to exchange thoughts and views.

Among all the diverse subjects which were covered throughout the panel discussions, interviews and meetings, the following topics have represented the most outstanding and shared global concerns among the conference’s participants.

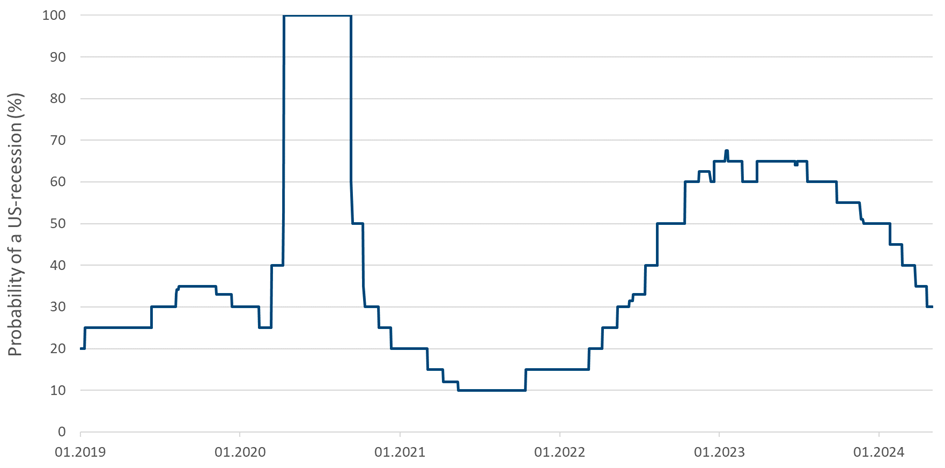

A potential US recession in the short-term is becoming less likely

One of the key themes was that the US economy proves to be much more resilient than anticipated. Despite the high level of interest rates in the US, a recession there is unlikely to be caused solely by restricting the lending activity of banks. This is partly due to some economic sectors’ relative insensitivity to changes in the interest rate paired with ongoing fiscal stimuli and strong economic activity as reflected by a high labour supply and productivity.

As shown in Figure 1, the one year ahead US recession probability forecast by Bloomberg peaked around 65% last year and is now down to 30%.

Figure 1: One year ahead US recession probability forecast as of April 30, 2024. Computed by Bloomberg using the median of estimates submitted by financial institutions and universities. The value depicts the current forecast of the probability of a US recession in one year. Data source: Bloomberg. Chart: Own chart.

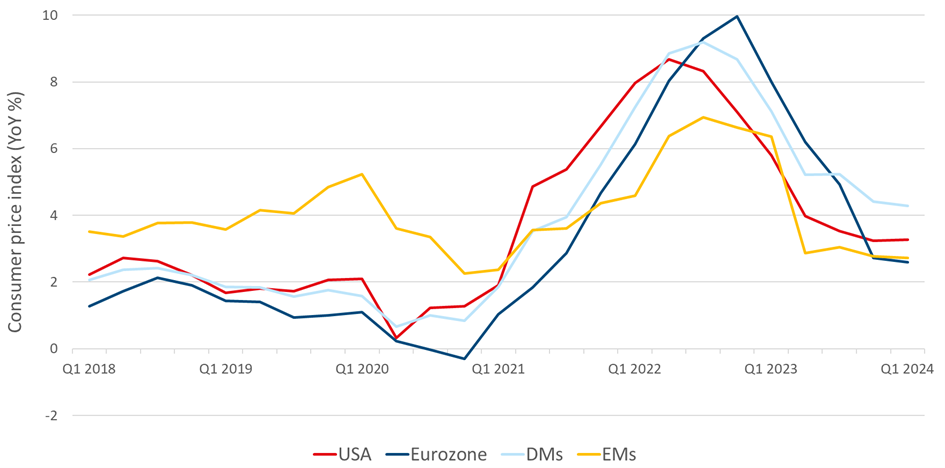

“High for longer” is the new “higher for longer”

At this time last year, the market consensus climaxed in the phrase “higher for longer”, i.e., that interest rates will be raised further by developed market (DM) central banks such as the Fed and the ECB and remain elevated for some longer period. Now, this view has just slightly changed to “high for longer” as further hikes in the respective key policy rates are not expected but the magnitude of previously priced in cuts is lowered.

The cause of this change is illustrated in Figure 2: As the inflation rates came down in the DMs and EMs after reaching a peak during the third quarter of 2022, the increase in prices started to become stickier one year later. This requires central banks to exert a less dovish stance and be more cautious in their forward-looking approach.

Figure 2: Year-on-year percentage change in the consumer price index as of April 30, 2024. The data is not seasonally adjusted. Data source: Bloomberg. Chart: Own chart.

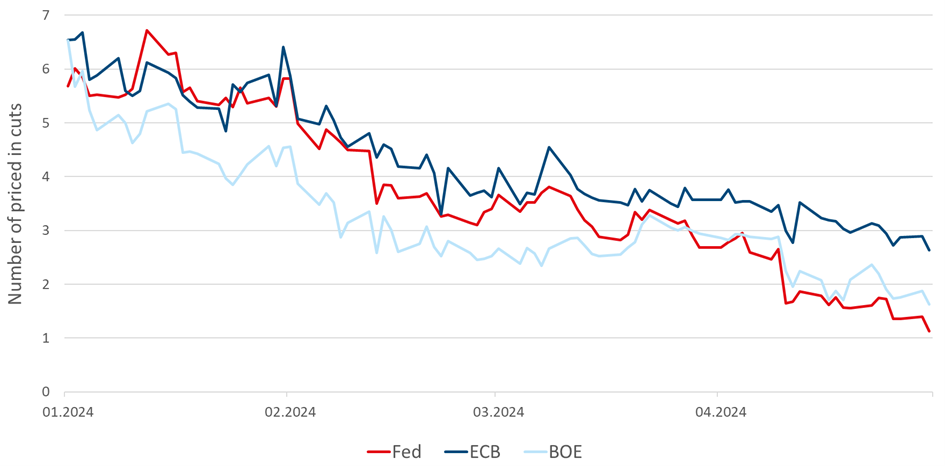

As depicted in Figure 3, at the beginning of the current year, markets expected around six cuts in the key policy rate, i.e., 150 basis points, for the Fed, ECB and BOE until the end of 2024. Over the past months, this value has dropped significantly. Now, markets price in only circa one cut for the Fed along with less than two and three for the ECB and BOE, respectively.

Figure 3: Number of priced in cuts in the key policy rate of the respective central banks until December 2024 as of April 30, 2024. Implied by using Fed Fund Futures in case of the Fed and Overnight Index Swaps in case of the ECB and BOE. One cut corresponds to 25 basis points. Data source: Bloomberg. Chart: Own chart.

Credit spreads globally as well as EM countries’ debt carrying capacity and currencies are the most vulnerable in such a hawkish pivot scenario, with Asian countries stronger exposed than Latin American or Central and Eastern European ones. On the other hand, the US-dollar would be the beneficiary in such a case albeit only with a limited upside potential.

Outlook on EM countries

The issuance of debt is picking up again globally since 2023 as fiscal deficits remain high in many countries which is partly due to the slow unwinding of COVID-era policies whilst a weakening medium-term growth outlook might render rising new debt more challenging. The debt service cost in EMs has risen in 2023, with 22% of overall tax revenue allocated to the coverage of interest payments. Nevertheless, for most of the EMs there is now light at the end of the tunnel as we slowly enter the phase of decreasing interest rates in the DMs which will likely cause an accretion of capital flows into EMs.

Latin America

Argentina’s new administration under Milei follows a very orthodox and prudent policy, both fiscally and monetarily, albeit signalling that it will take time to revert the wrong policies of the past. With the inflation rate projected to peak around 250% this year, monthly inflation is already showing promising signs of cooling. The economy is expected to grow again as of next year after being in a recession since mid-2023 which would allow for tax cuts. Once the central bank’s balance sheet has sufficiently recovered, capital controls are set to be removed.

Brazilian monetary policy makers aim to increase economic efficiency through further digitalisation of the financial system. They used the conference to demonstrate a hawkish stance after having limited the forward guidance to the next meeting, citing heightened uncertainty and the need for more flexibility. These actions come at a time when the government seeks to loosen its fiscal budget targets for the next two years which would delay the stabilisation of public debt levels.

Colombia is aiming to recover economic growth in 2024 it missed out on last year. Whilst planning a transition to renewable energy sources domestically, the reliance on fossil fuel exports, which are sought to be substituted by a stronger tourism sector as well as exports of agricultural produce and fabrics, is expected to persist for at least the next two decades. A key topic this year will be the potential revision of the debt ceiling with fiscal revenues revised downwards.

Mexico is facing a very tight labour market, a positive output gap and political stability as the ruling party is poised to win both elections in June. Under these conditions and despite an interest rate cut in March, Mexican monetary policymakers remain cautious, especially as the fight against inflation is not concluded yet. Nearshoring is seen as a big opportunity whilst the magnitude of the impact is not known yet as both private and public investments are needed to absorb production capacities. The rule of law, attracting skilled employees and interregional economic inequalities within the country are viewed as some of the current challenges.

Europe, Middle East and Africa

Egypt, which just recently has gone through a deep economic crisis, has managed to secure capital from multiple creditors within a very short time. Among the donors are, in descending order, the UAE, EU, IMF, World Bank and UK which together pledged USD 57.4 billion in total, parts of which will be used to pay off public debt. This funding is coupled with monetary reforms, namely allowing the Egyptian Pound to float and hiking the key policy rate to tame inflation. Overall, these developments have already attracted short-term investments by foreign investors who are keen to see if the Egyptian administration will stick to its reform commitments to achieve long-term stability.

Central and Eastern European countries such as Czechia, Hungary, Poland and Romania have one thing in common, namely that their inflation paths are strongly correlated and that they achieved to bring price increases down significantly over the last year. However, closing in on their respective target bands proves to become harder in the final stages with Romania struggling the most among the four.

South Africa suffers from a services inflation which is not due to a tight labour market but rather indexation effects. Moreover, elevated food price pressure is likely as the country has just gone through a bad growing season due to El Niño. However, the central bank’s view is that the monetary policy is restrictive enough to reach the inflation target band’s mid-point of 4.5% which might be revised down until the end of next year. Although the currency is considered undervalued, there is not much evidence yet that this has supported exports.

Turkey’s top economic policy priority now is achieving disinflation, with the central bank aiming to reach an inflation rate of 9% at the end of 2026, besides strengthening fiscal policy, narrowing the current account deficit and implementing structural reforms. Some of the planned fiscal measures include the review and cut of expenditures, reduction in energy subsidies and combatting the informal economy.

Asia

Despite news of a potential economic decoupling between China and Western countries, most of the Western firms are scaling up their investments in China. If the latter manages to stabilise its real estate sector, then it could reach its 5% GDP growth target this year. Nevertheless, political suggestions such as the one made by a US congressional committee to revoke China’s Permanent Normal Trade Relations status, which essentially would allow the USA to apply whatever tariff rates it wishes on Chinese goods, raise concerns. Economically, China needs to stimulate private consumption and the effectively regressive tax system must be reformed.

India has had a high real GDP growth in the last ten years, namely 6% on average, and is set to maintain this trajectory whilst transforming this growth into employment will be crucial. Public investments into infrastructure and industry production are part of the planned measures to achieve this. With the country’s ongoing inclusion in global investment indices, further capital is routed into the economy. Challenges remain in the realm of corporate consolidation, simplifying taxation, advancing deregulation and reducing the economy’s energy intensity. In the face of a weak opposition, the ongoing general elections are set to be won by the incumbent National Democratic Alliance with a vote share of again more than 40% which – due to the electoral system – translates into more than 60% of the seats in parliament.

View on risky assets remains bullish

The sentiment among investors is still bullish as most of them state that they are slightly overweight positioned in risky assets. Fixed income securities are expected to profit the most from the anticipated decline in interest rates in DMs, with EM credits likely to perform as well as in the recent past. Both the US and Eurozone interest curves are on a path to become steeper with the long end stickier to the upside than the short end.

Going forward, equities linked to the new economy are less vulnerable than those of the old economy with the latter exposed to price corrections if big tech firms stop delivering good numbers. In this context, 2023’s productivity growth can mostly be attributed to economic cyclicality and not significantly to the rise of AI.

Commodities are generally seen bullish. Oil markets remain tight with supply limited due to output cuts by Russia and Saudi-Arabia. Gold’s positive correlation with US real interest appears to be broken and the price increase in the last two months was mostly driven by a strong demand from China. The stockpiling of commodities performed by some market participants and geopolitical risks are further concerns for elevated prices.

The most favoured investment cases among the EMs are currently Turkey and Argentina where there is a complete overhaul of monetary and fiscal policies. Investors are already rewarding these positive changes by allocating capital to local assets after a long period of absenteeism. On the contrary, most investors have either significantly reduced their exposure to Chinese assets or are not invested at all. A potential resurgence in inflation is the most feared scenario which would harm the performance of risky assets.

Risk potential due to (geo-)politics remains high

The exchange of blows between Israel and Iran has forced the markets to be on alert but fortunately the tensions between the two countries have declined again as neither of the two is interested in a further escalation. Regrettably, the conflict between Ukraine and Russia is likely to persist in its current form and intensity with Russia being able to finance the war internally whereas Ukraine is reliant on Western support. Generally, current and potential wars are seen by investors as the largest threat to global economic development over the next decade.

Both the USA and China favour bolstering the bilateral trade – the former to avoid a political confrontation and the latter to focus on internal issues. But this stability through economic cooperation is fragile as both countries raise issues: China criticises US efforts to control Chinese access to advanced computer chips whereas the USA is concerned about China’s view on Taiwan’s status, its political support for Russia and price dumping through overcapacities in some of its industry sectors.

Further concerns arise from global supply chain disruptions. One cause for the latter are unilateral actions by countries to heavily subsidise the national production of computer chips and semiconductors which leads to an inefficient global resource allocation. Even though these subsidies constitute a breach of WTO rules, a negative ruling is not to be expected against these countries. Another cause is the trend of nearshoring which has a net negative effect globally. China is most adversely affected whilst Mexico and Thailand are beneficiaries and foreign direct investments are mostly rerouted to the USA and Europe. Ultimately, these disruptions give rise to the formation of blocks of trading countries.

The US presidential elections later this year are still too close to call whereas the likelihood, that the congress will remain split, is high. Both candidates have a strong voter base and the winning party will most likely be determined in the swing states. Independent of who will win the elections, it is certain that the outcome will have significant implications globally.