This week, the markets are eagerly awaiting the upcoming interest rate decisions: today, Wednesday, the US Federal Reserve begins; tomorrow, Thursday, the European Central Bank (ECB) will follow; and on Friday, the Bank of Japan (BoJ) will update its course.

The central banks would like to take a break from raising key-lending rates to better assess the effects of the previous rate hikes. However, the ongoing high inflation rates make this approach difficult, despite the fact that inflation has recently slowed down somewhat.

Two shocks

The global economy has been confronted by two major shocks, i.e. the pandemic and the war in Ukraine. In the meantime, economic indicators such as gross domestic product and employment have embarked on a process of normalisation. However, this process is extremely slow because of the long-lasting nature of the after-effects of the shocks. High inflation and the tight labour market stand out in particular.

High inflation and low productivity

In addition to the interest rate decisions, another focus this week was on the release of consumer price inflation data in the USA for the month of May. Traditionally, the volatile components of energy and food are excluded to establish the so-called core inflation.

This indicator fell slightly year-on-year from 5.5% in the previous month to 5.3%. A somewhat more pronounced decline to 5.2% had previously been expected. As in the previous month, the month-on-month change was 0.4%. Annualized (0.4% times 12 months), inflation is still far too high to be in line with the central bank’s inflation target of 2%.

In the Eurozone, the release of the Q1 GDP showed a 6.2% year-on-year increase in the overall price level. Both unit labour costs and corporate profits contributed to this situation. At the same time, labour productivity shrank because employment growth outpaced economic growth.

Rate hike pause?

Central banks have responded to this environment with a rapid cycle of interest rate hikes. But real economic growth in the developed world is subdued. In this environment, central banks would like to pause to better assess the lagged effects of rate hikes on growth, employment, income, investment, profits, and ultimately, inflation. This is because uncertainty about the relationship between monetary policy, growth, and inflation is traditionally high.

The medicine is starting to take effect

There are growing signs that the monetary policy “medicine” is beginning to take effect. In particular, bank lending guidelines have become more restrictive. Last week, the Institute for Supply Management’s purchasing managers’ index for the service sector pointed to growth risks in the USA with a drop to stagnation territory (50.3).

At the same time, the second estimate for economic growth in the Eurozone brought a downward revision. Now, real GDP contracted slightly in Q4 2022 and in Q1 2023 (by 0.1% quarter-on-quarter in each case). This development, known as a technical recession, is not an actual recession, but it does point to a difficult environment (stagnation).

What is the central banks’ strategy from here on out?

Inflation momentum is the fly in the ointment. Last week, two central banks, the Reserve Bank of Australia and the Bank of Canada, unexpectedly raised key-lending rates further (Australia to 4.10% and Canada to 4.75%).

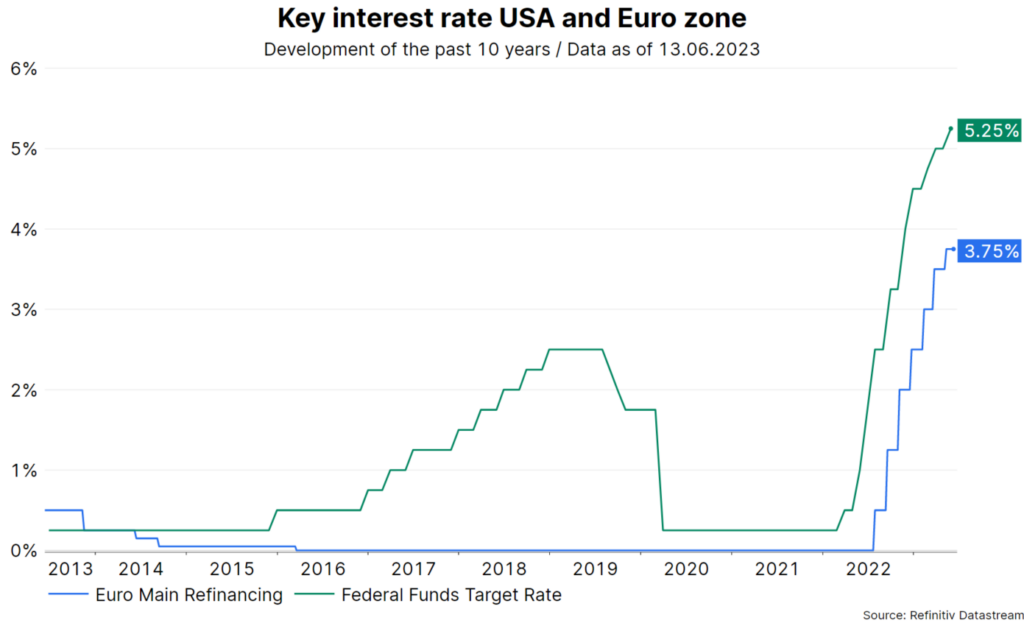

This week, as already mentioned, three important monetary policy decisions are on the calendar. For the Fed, no hike is expected for the first time in the current cycle. The upper band for the effective key-lending rate is at 5.25%.

By contrast, statements by ECB members suggest another increase. Market prices reflect an increase in the main refinancing rate from 3.75% to 4.00%. While no rate hike is expected for the Bank of Japan (currently: -0.1%), there is speculation about a further increase in the ceiling for the 10Y government bond yield (currently at 0.5%).

Please note: past performance is no reliable indicator of future development.

Risk management

The central banks are following a risk management approach. Inflation is to be lowered with a restrictive policy. If possible, a recession should be avoided. This is because inflation could fall even without a recession (“immaculate inflation”).

At the same time, the risk of inflation persistence should be kept as low as possible. This means that as long as inflation remains uncomfortably high, central banks will signal a propensity for (and indeed raise) further hikes, even if the growth environment is weak and some indicators point to recession risks. Thus, if the Fed were not to raise rates in June, it would be bold to speak of the end of the hike cycle at that point.

The overall view of growth indicators such as the global purchasing managers’ index for May suggests that the world economy will grow by 2% in the second quarter (annualised). The developed economies will grow at around 1%.

In the most likely scenario, there is thus no immediate recession. This has a directly positive effect on risky securities classes such as equities. That being said, numerous heuristics continue to argue against a “soft” landing of the economy. Only the timing is uncertain.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.