The crisis of confidence in the banking system continues to dominate market events and has significantly increased the uncertainty surrounding the further development of key economic indicators. One thing in advance: a recession has become (even) more likely.

Resilience

Published economic indicators point to an acceleration in real global economic growth to above potential growth in the first quarter of 2023 from the fourth quarter of 2022.

The V-shaped recovery in China after the pandemic-related opening measures has played a good part in this. However, higher growth is also emerging in the advanced economies. This is indicated by the flash estimates of purchasing managers’ indices for selected developed economies for the month of March. The aggregate index continued to rise.

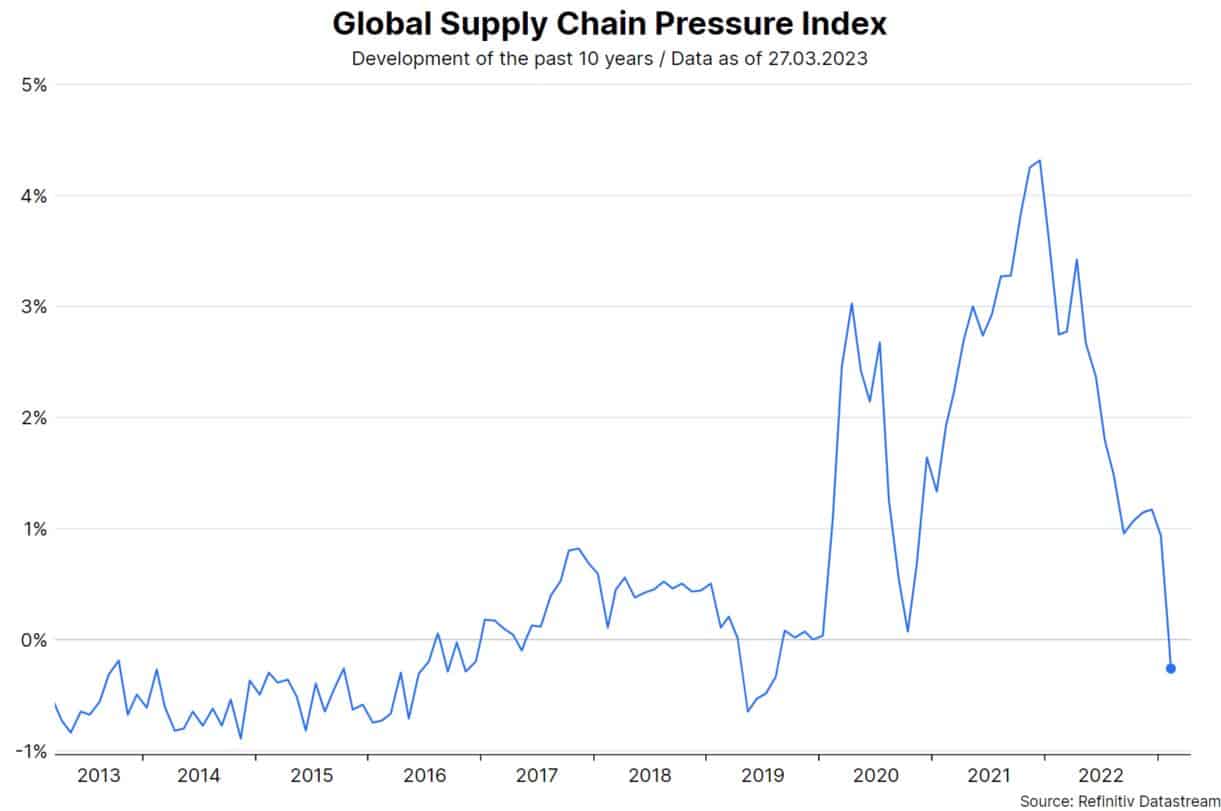

To date, economic activity has proved remarkably resilient. In Europe, the sharp fall in the wholesale price of natural gas has played a significant role in this. At the same time, the labor market remains very tight. In January, the unemployment rate in the OECD area reached a new low of 4.9%. In addition, a normalization is taking place in supply chains. The New York Fed’s Global Supply Chain Pressure Index fell below its pre-pandemic level in February.

Note: Past performance is not a reliable indicator for future performance.

Inflation persistence

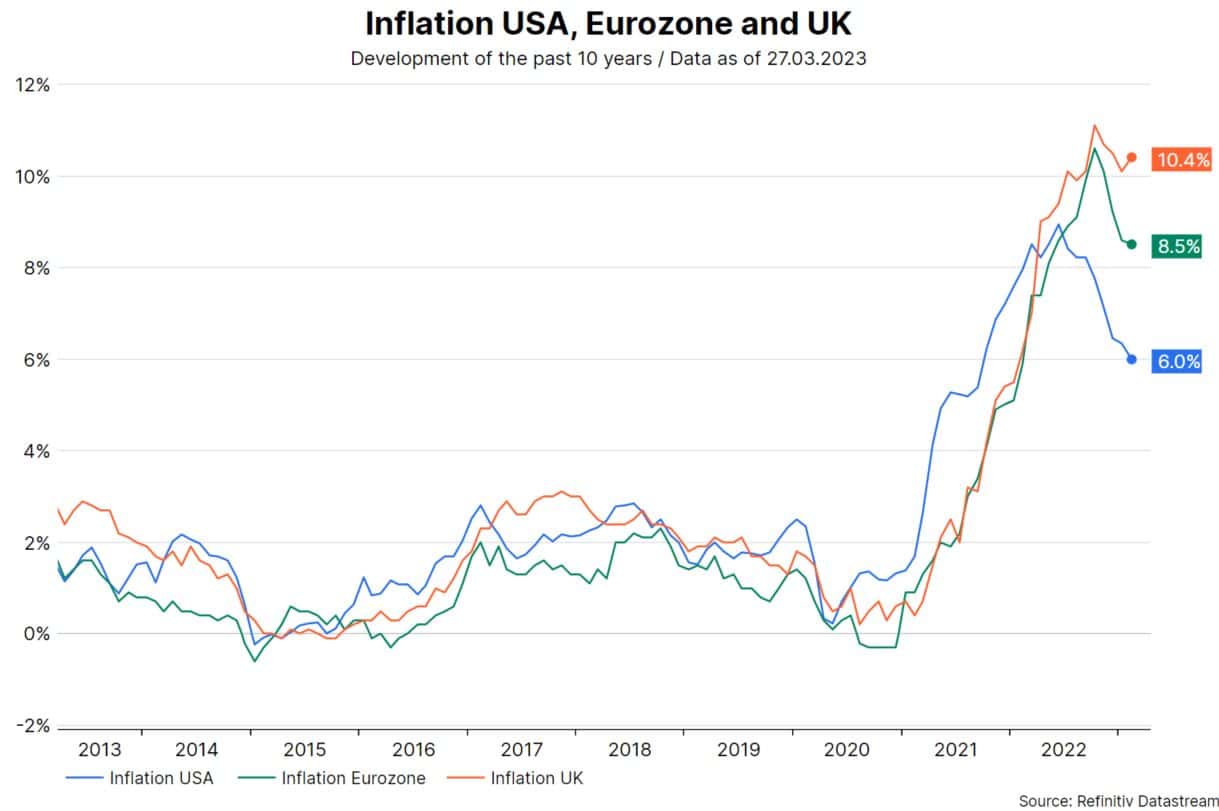

Unfortunately, the headwinds are increasing. Inflation rates remained uncomfortably high at the beginning of the year. In the OECD area, consumer prices rose 9.2% on an annual basis in the month of January. Last week, consumer prices in the UK for the month of February surprised with a sharp increase of 1.1% month-on-month to 10.4% year-on-year.

Note: Past performance is not a reliable indicator for future performance.

Next Friday, the flash estimate for consumer prices excluding food and energy in the eurozone for the month of March is expected to come in at a high 5.7% y/y (previous month: 5.6%). On the same day, the deflator (inflation) for personal consumption excluding food and energy in the U.S. is expected to rise by 4.7% year-on-year. There are indeed indications of a decline in trend inflation (NY Fed Underlying Inflation Gauge, NY Fed Consumer Inflation Expectations), but the published inflation rates are far too high.

Rapid hikes in key interest rates

High inflation is creating pressure on central banks to tighten monetary policy stances. Within a year, key interest rates have been raised very quickly and more and more central banks have started to reduce the very high bond holdings in their portfolios.

Last week, some major central banks continued to raise policy rates (U.S.: +0.25 percentage points to 4.7%-5%, UK: +0.25 percentage points to 4.25%, Switzerland: +0.5 percentage points to 1.5%). The week before, the European Central Bank raised key interest rates by 0.5 percentage points to 3.0% for the deposit facility.

Collateral damage

The goal of restrictive monetary policies is to push inflation down toward the central bank target. In the process, however, collateral damage has occurred: a crisis of confidence in the banking system. This implies two risks. First, financial market stability could be at risk. For this reason, central banks offer commercial banks a lot of liquidity, takeover partners for banks that got into troubles are quickly found (Credit Suisse) and, in the US, the authorities guarantee the full amount of deposits in problem banks.

The authorities assure that a systemic crisis can thus be prevented. Second, a further tightening of bank lending standards is very likely. In principle, central banks consider this desirable. After all, an important effect channel of key interest rate hikes is a slowdown in lending, which puts pressure on economic growth and, with a time lag, on inflation.

Uncertain Substitute

Uncertainty about the dampening effect of tighter monetary policy on economic growth and inflation in terms of magnitude and timing was already considerable before, but recent events in the banking system have raised it again. This is because the extent of the likely tightening of lending standards is still in the dark.

This also makes it difficult to assess the extent to which the (probably) tighter credit environment will serve as a substitute for a restrictive monetary policy. However, the risks of a recession have increased again in the medium term. At least, this is supported by the experience (econometric relationships) of the past decades.

Market implication

There could be a new driving factor for market development. Until now, rising interest rates have been primarily responsible for falling asset prices. If the expectation of a marked tightening of lending standards actually materializes, falling growth rates (a recession) could put pressure on risky assets, even if interest rates fall.

For a glossary of technical terms, please visit this link: Fund Glossary | Erste Asset Management

Legal note:

Prognoses are no reliable indicator for future performance.