While the sharp losses on the equity markets about two weeks ago have largely been recovered, they have shown one thing: the path for achieving the so-called soft landing of the economy is a tight one. The financial markets are still hoping for this scenario where economic growth in the USA would slow to below trend and the Eurozone would return to sustainable growth. At the same time, inflation would continue to fall slowly.

However, the downside risks, which have recently increased again, make it clear that this scenario is far from a foregone conclusion. It is not only the geopolitically tense situation in the Middle East that is a factor of uncertainty. The latest economic data from the USA has also been on the disappointing side. In any case, the past few weeks have brought some new insights, also for positioning in the second half of the year.

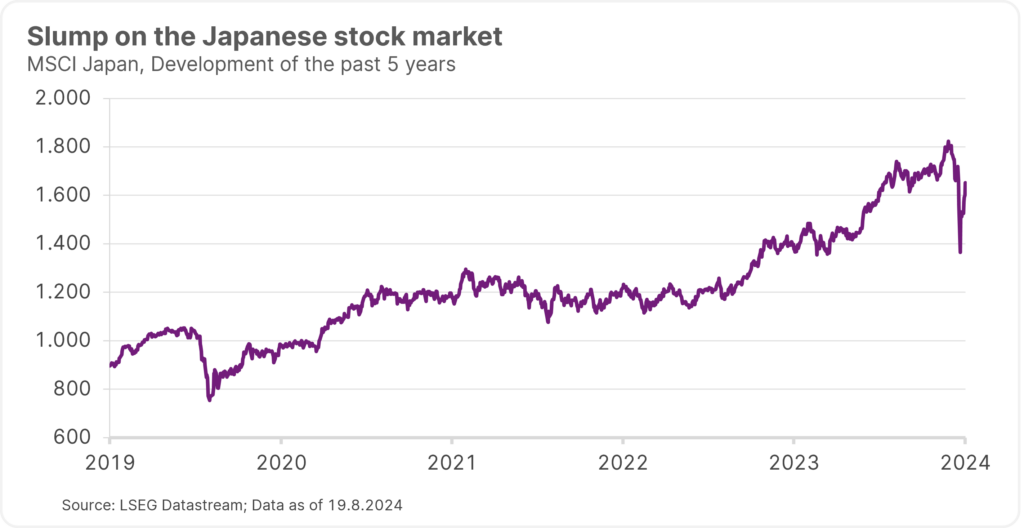

Shock waves from Japan

The market turbulence originated in Japan at the beginning of August. Surprising interest rate hike signals from the Japanese central bank caused real shockwaves in the financial system. To a certain extent, the reason for this was the undervaluation of the Japanese yen, which had been exacerbated in previous years by the ultra-loose monetary policy in Japan. While key-lending rates were raised in many other countries, they remained at 0.1% in Japan until recently.

As a result, the yen was increasingly used as a funding currency for investments that yielded higher returns: large institutional investors had taken out loans in yen in order to invest these funds in equities or other asset classes. This was reflected in the sharp rise in the volume of loans that Japanese banks had granted to investors from abroad.

However, after the Japanese central bank has raised the key-lending rate to 0.25% surprisingly early on and signalled possible further increases, the interest rate differential between Japan and the rest of the world is now narrowing. As a result, the yen exchange rate is appreciating, and the aforementioned debt financing is coming under pressure. The result was the cancellation of many of these so-called yen carry trades, which caused unrest on the equity markets and in some cases resulted in substantial losses.

Please note: past performance is no reliable indicator of future value development.

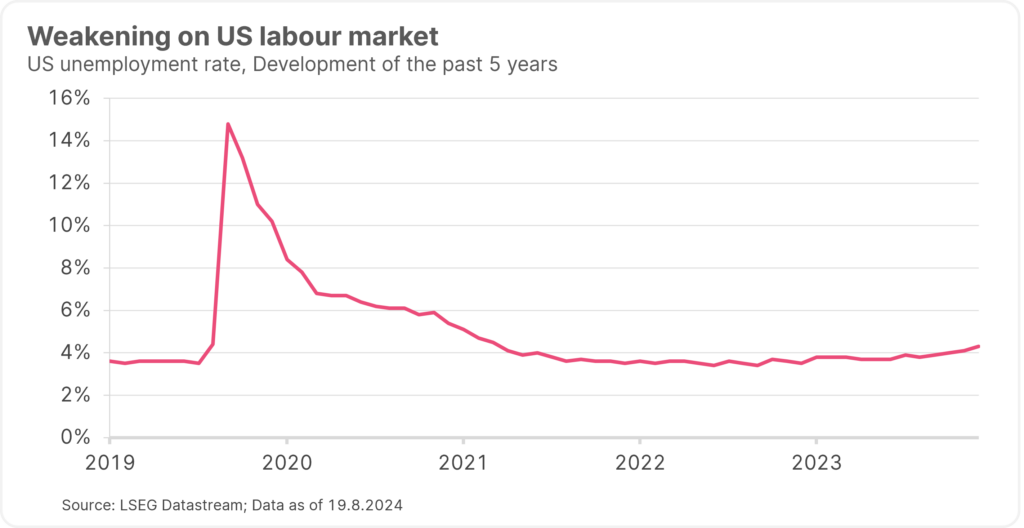

Weaker US job market weighing on the sentiment

In addition to the carry trades in Japan, burgeoning concerns regarding a recession have also dominated market activity recently. In the USA, growth risks have increased, primarily due to the weakening job market. From January 2023 to July 2024, the unemployment rate in the United States rose from 3.4% to 4.3%.

This triggered a recession indicator observed by many market participants, i.e. the so-called Sahm Rule. This barometer compares the three-month moving average of the unemployment rate with its lowest point over the past twelve months. In the past, the indicator has proven to be quite reliable in predicting a recession. With the latest US job market report, the ratio reached the decisive value of 0.5 percentage points for the first time since the coronavirus crisis.

This means that unemployment is still at a relatively low level. In the past, however, initial slight increases were often followed by a stronger rise in the unemployment rate, which was tantamount to a recession. The risk therefore manifests itself as a downward spiral: a reduction in employment would lead to lower incomes, which would dampen consumption. Companies would react by cutting jobs and reducing investment.

Prospect of rate cuts, with one exception

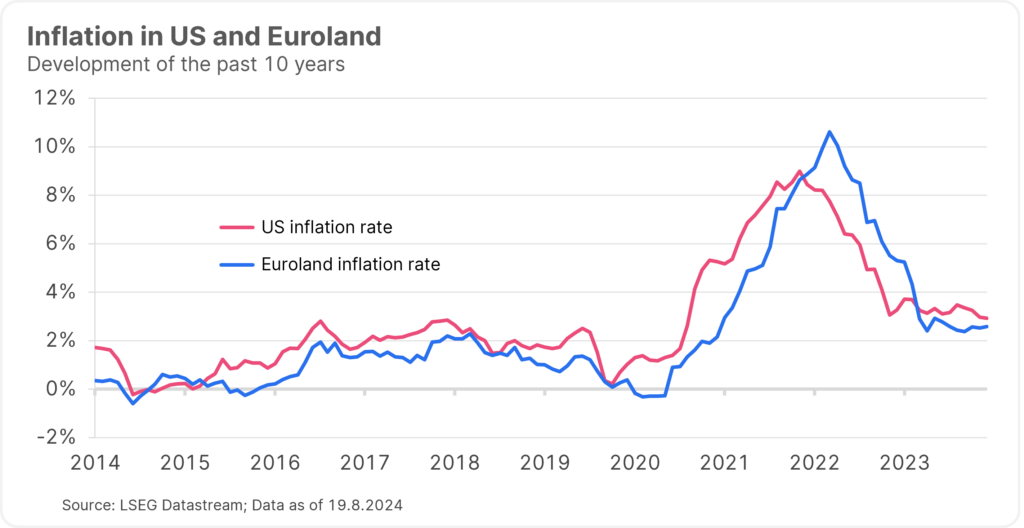

In any case, the weakening job market and the further decline in inflation are fuelling expectations of interest rate cuts in the USA in the near future. According to Gerhard Winzer, Chief Economist at Erste Asset Management, the US key-lending rate could be reduced from the current 5.5% to 3.0% by the end of 2025. In the Eurozone, too, many an indication would suggest further interest rate cuts. Winzer expects the deposit rate to be lowered from the current 3.75% to 2.0% by the end of 2025.

The Bank of Japan is the notable exception here: as already described, the key-lending rate is likely to continue to rise. Our current expectations are for a level of 0.75% by the end of 2025.

Expectations for the development of inflation from here on out are all pointing in one direction: downwards. Inflation in both the USA and the Eurozone is likely to remain above the central banks’ target of 2% in the coming year. With 2.3% for the USA and 2.2% for the Eurozone, chief economist Winzer expects inflation to come close to the central bank target in 2025.

What is our positioning strategy for the second half of 2024?

The soft landing, i.e. a gradual decline in inflation without the outbreak of a recession, is currently considered the most likely economic scenario, even if it is not yet possible to conclusively assess whether it will actually come to pass. It would certainly be positive for risky asset classes such as equities.

However, the recent losses show that there are still some downside risks that could lead to selling pressure. The tense geopolitical situation in the Middle East adds to the mix as an additional uncertainty factor.

We therefore slightly cut the equity component in Erste Asset Management’s mixed funds as a result of the uncertainty starting in Japan in order to reduce risk. At the same time, we overweighted bonds in the portfolios. On the one hand, this is due to the persistently high interest rates at the short end (inverted yield curve) and the continuing economic risks. On the other hand, there appears to be a negative correlation between equity and bond prices on the market again: losses in equities can therefore be partially cushioned by bonds.

In Anleihen investieren mit fixer Laufzeit

Adding bonds to the portfolio can therefore make sense in the current environment. High-yield bonds in particular offer an interesting risk/reward ratio due to the increased risk premiums (spreads). Investors can invest in this segment with our newly launched ERSTE LAUFZEITFONDS HOCHZINS 2029 IV bond fund, for example.

The fund can be subscribed to from 2 September at Erste Bank and savings banks as well as online. It invests primarily in high-yield bonds and offers the advantage of a fixed term. It should be noted that investing in securities entails risks as well as opportunities. 👉 For more information on ERSTE LAUFZEITFONDS HOCHZINS 2029 IV, please visit our website.

Risk Notices

The fund pursues an active investment policy and does not follow a benchmark. The assets are selected at our discretion, without any constraints to the latitude of judgement on the investment company’s part.

Warning notices according to the Austrian Investment Fund Act of 2011

ERSTE LAUFZEITFONDS HOCHZINS 2029 IV may invest a significant portion of its assets under management in demand deposits or callable deposits with a maturity of a maximum of twelve months as defined by sec 72 of the Austrian Investment Fund Act of 2011.

In accordance with the fund terms and conditions approved by the Austrian Financial Market Authority, ERSTE LAUFZEITFONDS HOCHZINS 2029 IV intends to invest more than 35% of assets under management in securities and/or money market instruments from public issuers. For a detailed statement on these issuers, please refer to the prospectus, section II, sub-section 12.