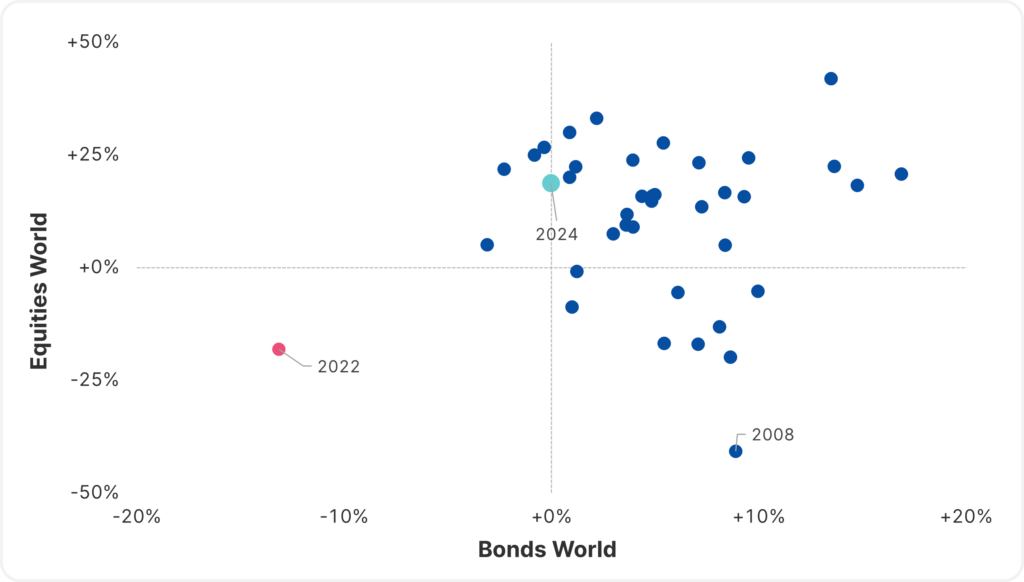

Looking back, 2024 feels complicated for us asset managers – especially for equity investments, there were repeatedly good reasons to be cautious: In the months of July-September, the economic data for the US clouded over significantly and fundamentally reliable indicators seemed to point to a recession. However, looking at the annual result alone, it is another year of normality, as the following chart shows. 2024 lies inconspicuously within the “point cloud” of historical annual returns for equities and bonds, from which only the years 2022 and 2008 actually fall out.

Note: Past performance is not a reliable indicator of future performance.

Annual performance of equities and bonds (1986-2024)

Source: ErsteAM, LSEG Datastream, data as at 31.12.2024 / World equities = MSCI World, World bonds = ICE BofA Global Government Index

The past 5 years have seen unprecedented events for the equity market – the 2020 pandemic and the difficult year 2022 for both equities and bonds, caused by the exceptionally rapid and sharp rise in inflation.

None of this was able to derail the medium-term performance of equities, as the following chart clearly shows. Ultimately, the stock market has come back stronger each time, mainly on the basis of the economic innovation power of the USA (e.g. the famous “Magnificient 7”), whose share in a global stock index such as the MSCI World is now approaching 3/4.

Note: Past performance is not a reliable indicator of future performance.

Performance of world equities (5 years)

Source: ErsteAM, LSEG Datastream, data as at 31.12.2024 / World equities = MSCI World; Representation of an index, no direct investment possible.

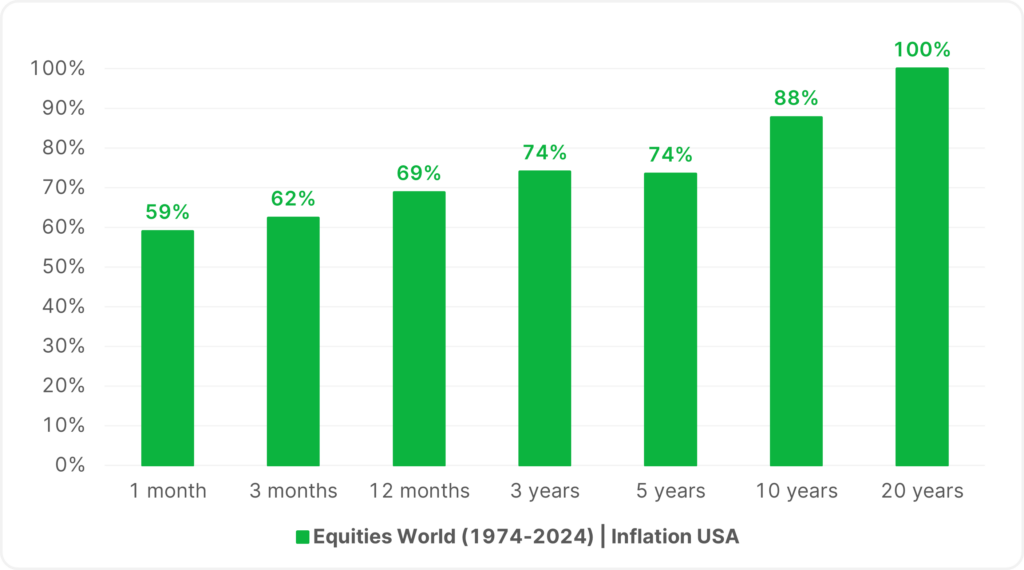

What remains is the “superpower” of equities to combat inflation. The next chart compares the return of a global equity basket with inflation in different time frames, between one month and 20 years. A very short equity investment outperformed inflation in around 59% of cases – whereas a customer with a 20-year investment horizon was able to compensate for inflation in 100% of cases. The period 1974-2024 was taken a basis. It should be noted that investing in shares always involves risks.

Comparison of shares with inflation

Source: ErsteAM, LSEG Datastream, data as at 31.12.2024 / World equities = MSCI World

Only time will tell whether gold has come to stay after a brilliant year with a significant price increase of around 27 percent. The Trump II era is likely to be characterized by the erection of new tariff barriers, deregulation and a possibly less stringent fight against inflation by the US Federal Reserve. During Donald Trump’s first presidency (with similar themes), gold has certainly performed well.

Note: Past performance is not a reliable indicator of future performance.

Development of gold (5 years)

Source: ErsteAM, LSEG Datastream, data as at 31.12.2024; Representation of an index, no direct investment possible.

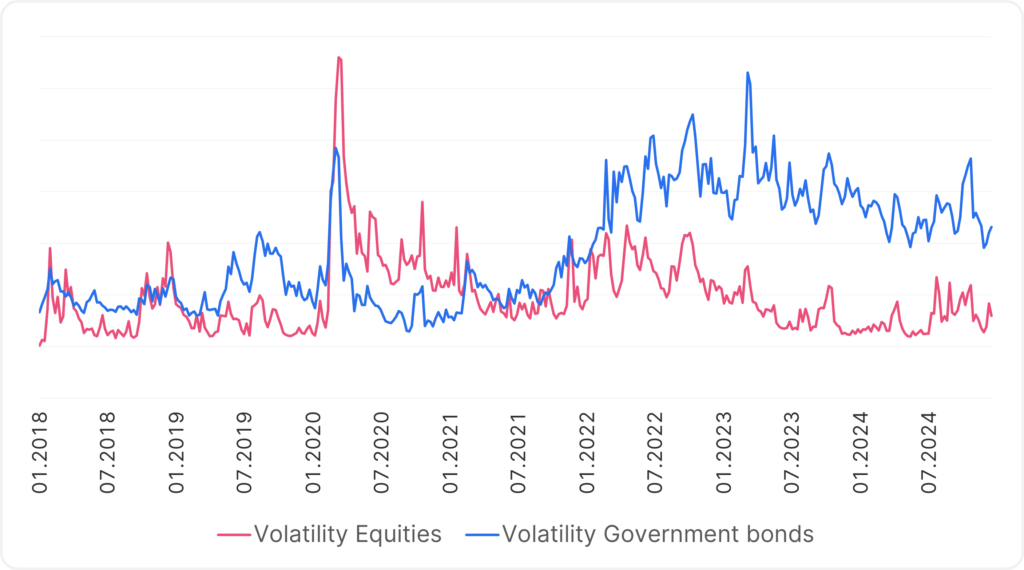

The volatility of equities and government bonds, i.e. the short-term fluctuation range that tends to worry investors, appears to be softening. As the following chart shows, the volatility of equities only flared up briefly in 2024, and to a manageable extent. Bond volatility, on the other hand, is likely to be permanently past its peak in 2023, when inflation shook up the bond markets. Nevertheless, volatility should never be completely discounted, as it is ultimately the expression of sudden and unexpected events.

Note: Past performance is not a reliable indicator of future performance.

Volatility of US equities and US government bonds

Source: ErsteAM, LSEG Datastream, data as at 31.12.2024

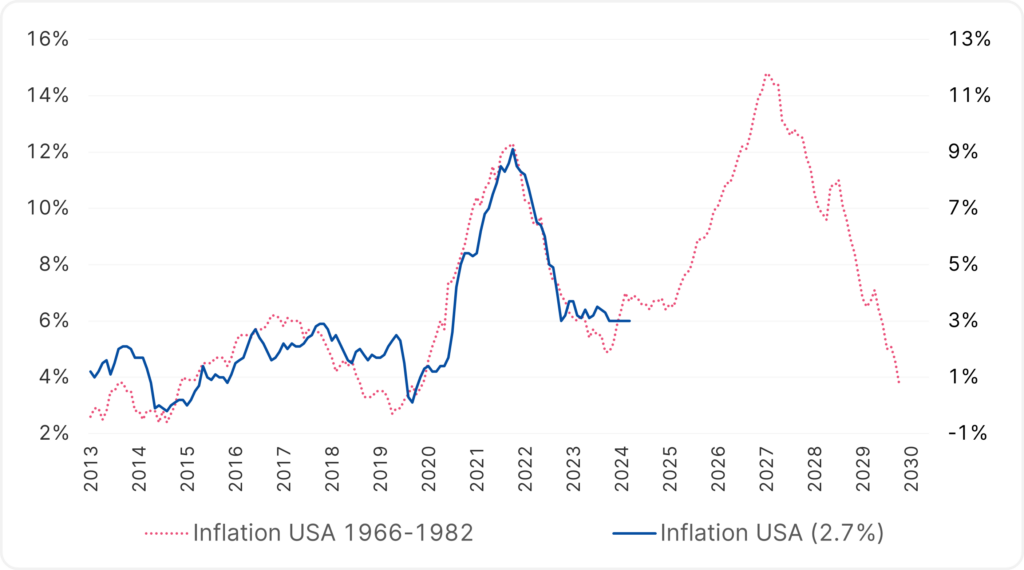

Has the spectre of inflation been banished for good? There is much to suggest that it has, but only time will tell. A comparison can be made with the 1970s – the next chart shows inflation then and now. Back then, the oil price shock inflation came under control for the time being, only to be followed later by a second wave. Strictly speaking, there are no valid reasons today that indicate a comeback of inflation – potential causes could be exploding commodity prices due to geopolitical conflicts, as the attack on Ukraine has already shown.

Comparison of inflation with the 1970s

Source: ErsteAM, LSEG Datastream, data as at 31.12.2024

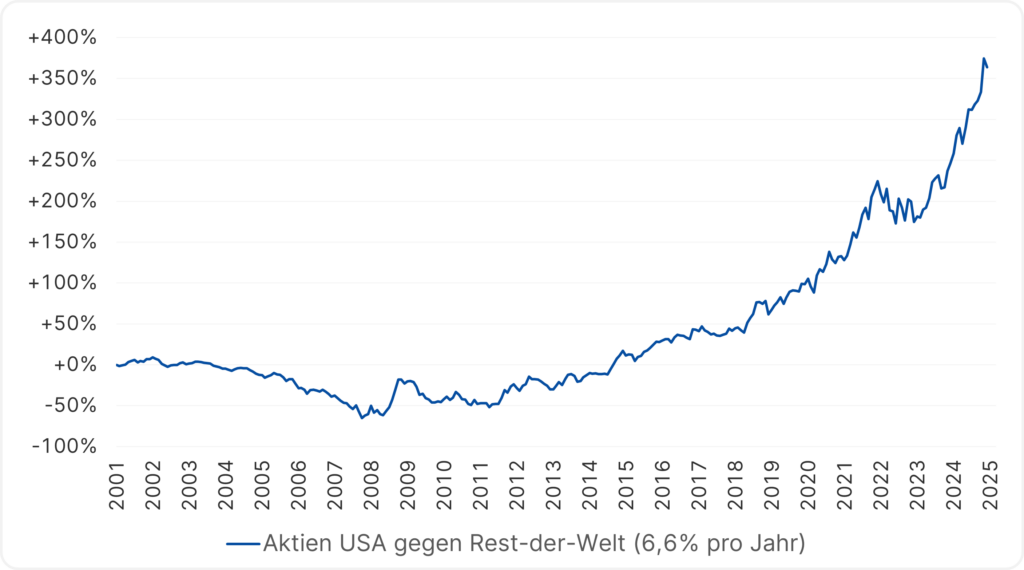

The outperformance of US equities against the “rest of the world” – i.e. in comparison with Europe and Asia (Japan, China) – has reached almost epic proportions. This seemed to stabilize in 2022/23 – only to return all the more massively in 2024! To take one example: While Volkswagen is struggling in Germany and cannot really gain a foothold in the global e-mobility market, Tesla is more valuable on the stock market than ever before. Although this is also due to the proximity of the Tesla boss to President Trump, it shows us that the USA is clearly tackling many issues more successfully than Europe.

Note: The companies listed here have been selected as examples and do not constitute an investment recommendation. Past performance is not a reliable indicator of future performance.

Outperformance of US equities versus the rest of the world

Source: ErsteAM, LSEG Datastream, data as at 31.12.2024 / World equities = MSCI World, Rest of the world equities = MSCI World excl. US Index

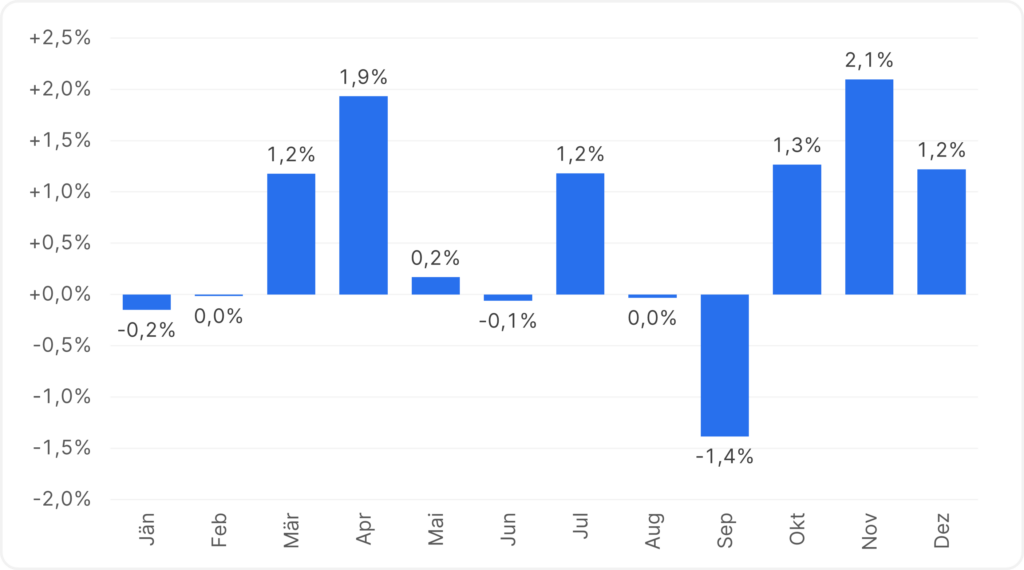

Obviously, the “calendar effect” for equity investors continues to exist. Naturally, this is an average view and this effect does not occur every year, but it does show that the 4th quarter tends to be more lucrative (observation from 1999 onwards). This was also the case in 2024.

“Calendar effect” for global equities

Source: ErsteAM, LSEG Datastream, data as at 31.12.2024 / World equities = MSCI World

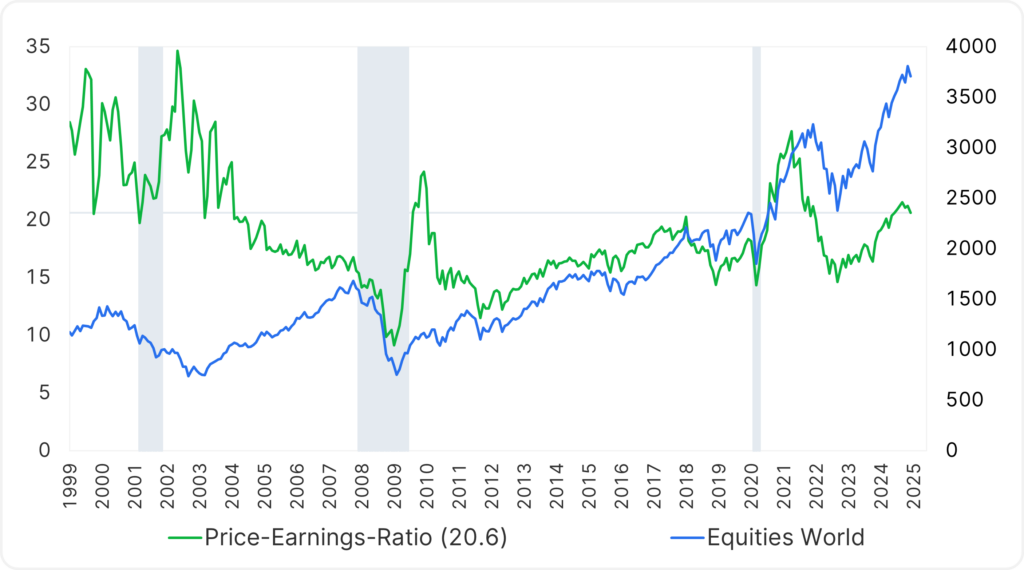

Are shares now already expensive and should therefore tend to perform weaker? This chart shows that despite the sporty price performance, the price/earnings ratio is not unusual, i.e. the rising prices are being driven by rising profits (especially in the USA).

Note: Past performance is not a reliable indicator of future performance.

Price/earnings ratio for the global equity market

Source: ErsteAM, LSEG Datastream, data as at 31.12.2024 / World equities = MSCI World

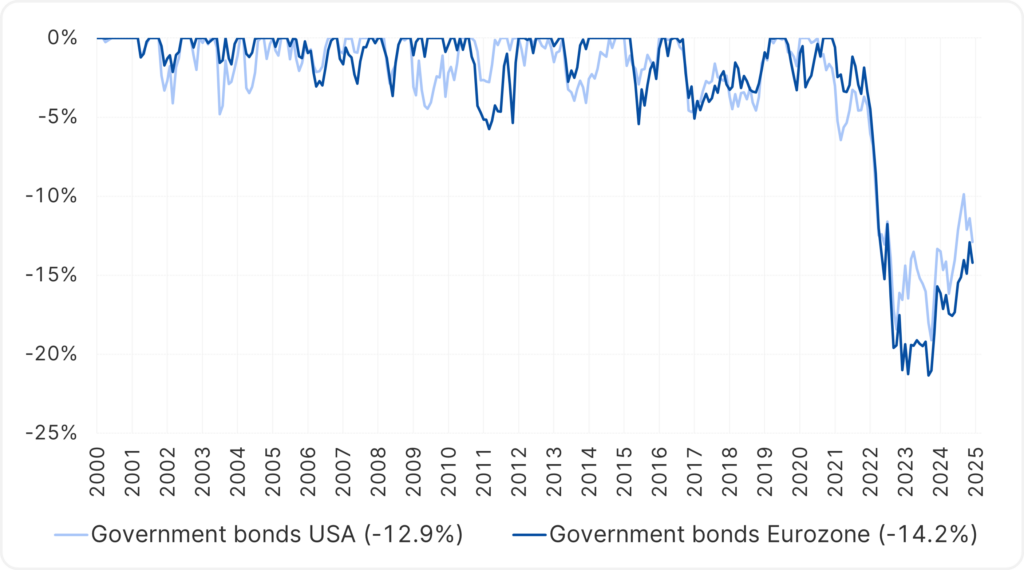

Government bond investments are also a good investment for 2025 – as our final chart indicates. The losses that occurred in 2022 have not yet been made up. Furthermore, central banks have the opportunity to “lend a helping hand” to bond investors by lowering key interest rates.

Note: Past performance is not a reliable indicator of future performance.

Loss phases for government bonds

Source: ErsteAM, LSEG Datastream, data as at 31.12.2024

Conclusion

A lot happened behind the scenes on the capital markets in 2024. If you add it all up to just one annual result, it was a really profitable year for investors. From today’s perspective, there is no need to remove any asset class (equities, bonds, gold, etc.) from the portfolio in 2025.